Solventum Corp's Earnings Surge Highlights Growth Bottlenecks and Cash Flow Pressures

Strong revenue expansion contrasted by sharp operating cash flow decline and margin contraction demands close attention.

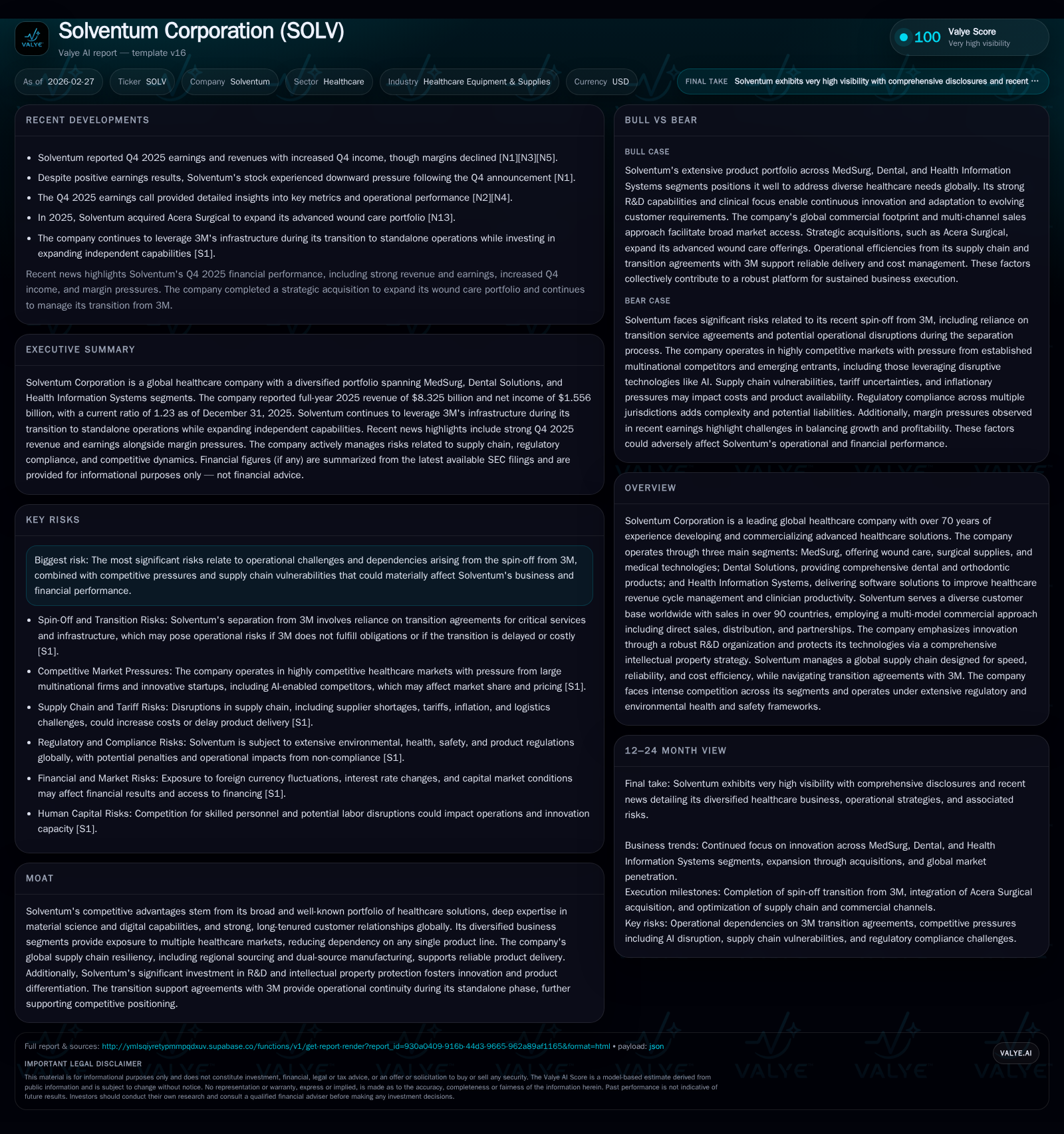

Solventum Corporation, a healthcare leader spun-off from 3M, delivered modest revenue growth of less than 1% in 2025 with operating income more than doubling year-over-year. However, this profit improvement belies challenges as the company’s operating cash flow plunged nearly 70%, leading to negative free cash flow despite steady capex levels. Solventum’s diversified portfolio in MedSurg, Dental Solutions, and Health Information Systems provides resilience but faces headwinds from transitional dependencies on 3M, pricing pressures, expanding regulatory complexity, and supply chain risks. Investors should watch for progress on standalone infrastructure development and operational efficiencies amid intensifying competition and evolving healthcare regulations.

Historical Performance and Growth Drivers

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.3 | 1556 | 369 | 2.2 | +0.9% | +224.8% |

| 2024 | 8.3 | 479 | 1185 | 1.0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -10 | 30.8 |

| 2024 | 805 | 16.2 |

Source: SEC companyfacts cache [F1].

Solventum Corp, having emerged as a standalone entity post-spin-off from 3M, posted total revenues of $8.33 billion in fiscal year 2025, marking a marginal uptick of just under 1% from $8.25 billion in 2024 [F1]. The revenue trajectory underscores a plateauing maturity given Solventum's established presence in global healthcare markets spanning over 90 countries. However, beneath the surface top-line stability was a pronounced shift in profitability metrics: operating income more than doubled to $2.18 billion from roughly $1.04 billion a year prior while net income soared over 220% to nearly $1.56 billion [F1].

Operating margins expanded largely due to operational restructuring initiatives aimed at cost containment, supply chain efficiency improvements, and phase-in of higher-margin innovations within segments like MedSurg—which contributed almost 58% of sales—anchored by advanced wound care solutions designed to accelerate healing and reduce total care costs [S10][F1]. The Dental Solutions division (16%+ revenues) provides orthodontic brackets and restorative products supporting broad dental lifecycles; meanwhile Health Information Systems (HIS) segment similarly contributes about 16%, offering AI-driven clinical documentation platforms aimed at streamlining hospital reimbursement processes amidst industry-wide digitization pressures [S10][S14].

Operational Cash Flow Deterioration

Paradoxically however, this bottom-line strength masked severe strain on liquidity metrics. Operating cash flow (CFO) dramatically declined by nearly 69%, plunging from approximately $1.18 billion in FY2024 down to $369 million in FY2025—a drop disproportionately large relative to net income swings [F1]. Capital expenditure (Capex) outlays were relatively flat around $379 million reflecting ongoing commitments toward manufacturing footprint expansion and R&D—but free cash flow turned negative by approximately $10 million after accounting for these investments [F1].

This divergence suggests widening gaps in working capital management or non-cash revenue recognition enhancements not fully translating into near-term cash generation post-spin-off; analysts should monitor quarterly liquidity trends closely alongside receivables/payables cycles as Solventum continues disentangling itself operationally from legacy parent company dependencies [S1][S24]. The company retains sizable current assets versus liabilities ($3.86B vs $3.14B), yielding a current ratio of about 1.23 indicative of manageable short-term liquidity but less cushion against ongoing costs volatility or supply chain turbulence [F1].

Transition Status and Corporate Separation Risks

Solventum remains reliant on transition service agreements with 3M for critical functions such as IT systems support, supply logistics, legal services, treasury operations, auditing controls, HR administration, and finance management during its early independent phase [S1][S10][S18]. This operational tether carries potential risk should any service interruptions or contractual limitations arise impacting business continuity or margin control.

Additionally, cost of capital may be higher now compared to when it was embedded within the larger diversified enterprise entity which benefits from broader scale economies—a vulnerability as Solventum navigates credit ratings scrutiny by major agencies that impact financing flexibility amid macroeconomic tightening trends [S17][S24]. The company’s independence also shifts exposure toward foreign currency exchange rate fluctuations more acutely given its international sales footprint exceeding ninety countries [S17].

Growth Outlook: Innovation Amid External Pressures

Solventum targets growth through advancing its proprietary materials science expertise paired with data science integration—particularly emphasizing digital health platforms within the HIS segment poised to better align reimbursement accuracy with clinicians’ workflows using automation technologies beyond traditional software applications [N3][S10][S14]. The MedSurg product pipeline aims at incremental improvements in negative pressure wound therapy devices alongside synthetic tissue matrices enhancing patient outcomes.

However, competitive dynamics intensify with new entrants leveraging AI capabilities that could disrupt existing HIS offerings; pricing pressures exacerbate margins especially when negotiating with consolidated healthcare providers wielding greater bargaining power over suppliers [S14][S20]. Regulatory landscapes remain complex globally: compliance burdens span product safety approvals to rigorous enforcement of anti-bribery laws such as FCPA (Foreign Corrupt Practices Act), privacy protections like HIPAA and GDPR frameworks affecting data handled by HIS solutions; failure risks include fines or exclusion from government contracting which accounts for considerable sales volume [S19][S21][S27].

Environmental compliance extends into emerging challenges related to PFAS substances within some products prompting ongoing material substitutions where feasible; regulatory scrutiny increasingly targets carbon emissions disclosures alongside mandated sustainability reporting adding both cost pressures and strategic imperatives for greener innovations that can sway buyer preferences [S16][S26][S29].

Financial Returns and Capital Deployment

Equity invested has nearly doubled year-over-year to about $5.05 billion paralleling the spin-off’s capital structure adjustments; utilizing net income figures yields a robust approximate return on equity (ROE) of roughly 30.8%, underscoring high profitability relative to shareholder equity base size post-separation [F1]. Yet the operating cash flow decline tempers enthusiasm regarding underlying free cash flows essential for funding growth initiatives internally without excessive external financing.

Dividend policies or share repurchases as part of capital allocation strategies were not explicitly stated in recent filings or press releases thus monitoring future quarterly disclosures remains key; maintaining investment capacity while managing debt levels will be pivotal given uncertain macroeconomic factors affecting cost of credit assiduously tracked by rating agencies influencing solvency premiums paid by Solventum versus prior integrated status within 3M ecosystem [F1][S17][N7][N2].

What to Watch: Key Catalysts and Risks Ahead

- Execution speed on replacing legacy services currently provided by 3M under transition contracts without degrading quality or raising costs too sharply.

- Development success of AI/automation-based health information solutions countering both existing competitors’ advances and emergent AI entrants addressing clinical burden reduction.

- Regulatory outcomes related to anti-corruption audits or claims management including adherence to global laws across government customer bases.

- Supply chain resilience amidst geopolitical tariff uncertainties (e.g., US-China trade tensions) impacting materials sourcing or manufacturing operations.

- Progress minimizing environmental liabilities associated with PFAS-containing products while aligning growth with sustainability standards required by clients increasingly focused on ESG factors.

- Capital market affordability pressures influencing access to low-cost funding instrumental for organic R&D investment or bolt-on acquisitions intended to supplement core competencies.

Solventum’s position as a diversified healthcare supplier with a strong innovation pipeline is compelling yet its transition challenges from corporate parenthood combined with volatile cash generation dynamics form a critical backdrop shaping strategic choices through calendar year 2026 onward.

Disclaimer: This analysis is intended solely for informational purposes based on available disclosures as of February 2026. It does not constitute investment advice or recommendations regarding the securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments