AsiaStrategy Reinforces Watch Market Position as Web3 Ventures Gain Traction

April 2026 filings reveal governance enhancements and progress in digital asset integration complementing AsiaStrategy’s core luxury watch trading.

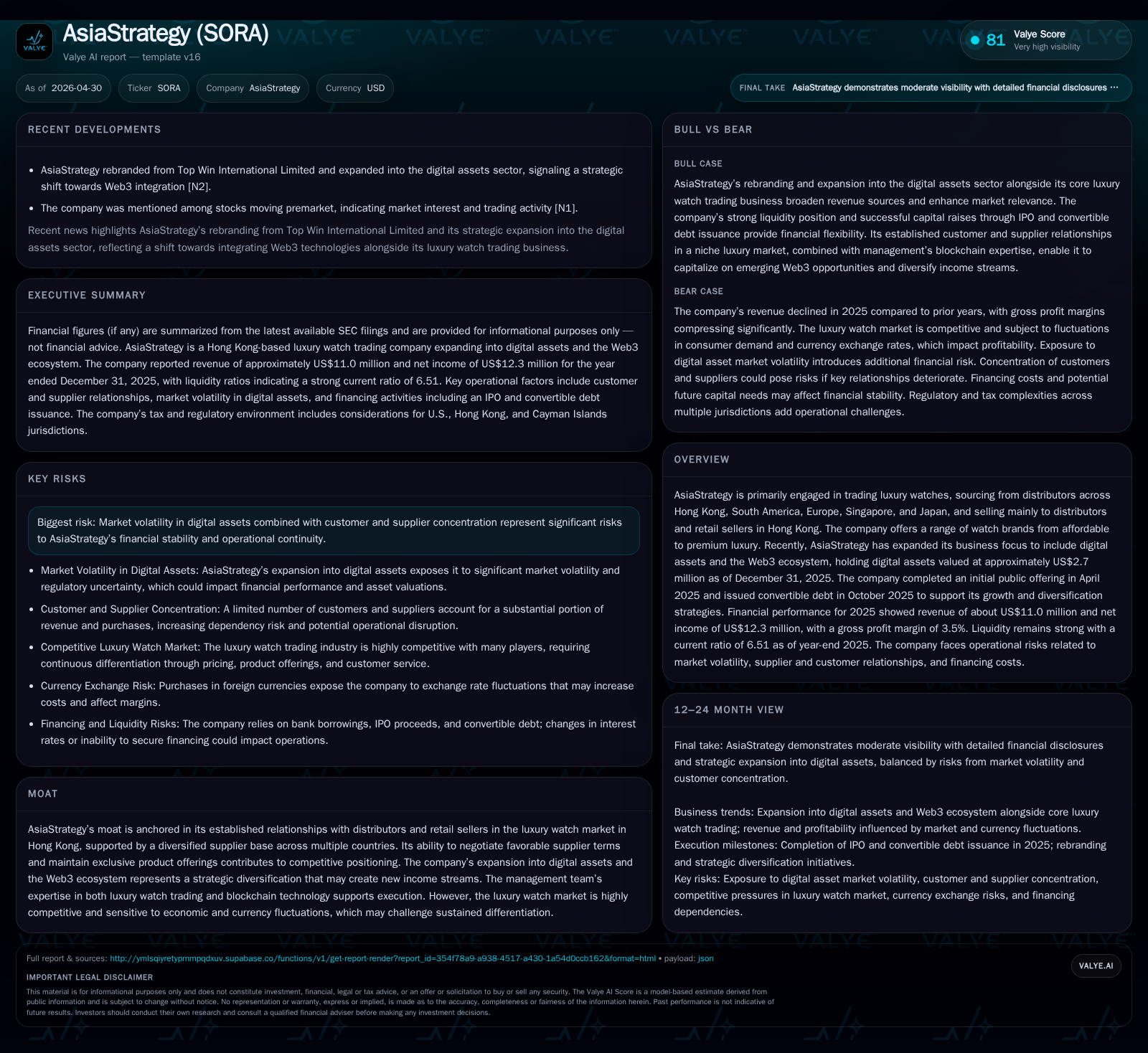

AsiaStrategy’s latest quarterly filing highlights appointment of an independent director with cross-border transaction expertise, underscoring governance strengthening. The company continues to balance its traditional luxury watch distribution in Hong Kong with strategic expansion into digital assets and Web3 ecosystems, holding approximately $2.7 million in digital assets as of end-2025. While revenue grew modestly to about $11 million in 2025 and net income reached $12.3 million, gross margin compression driven by product mix shift and currency headwinds presents margin pressures. The issuance of convertible debt and IPO proceeds are fueling diversification efforts, but risks including customer concentration and crypto volatility remain relevant.

Latest Quarterly Developments: Governance and Operating Highlights

AsiaStrategy’s April 21, 2026 quarterly filing signals notable governance updates that reinforce organizational oversight amid evolving business dynamics. The appointment of Mr. Yunming Tao as an independent director replaces Mr. Xiaojun Wang and brings specialized expertise in corporate law spanning governance frameworks, finance structuring, M&A, international transactions, intellectual property litigation, and cross-border investments between China and Japan environments [S3]. His chairmanship of the nominating committee alongside membership on audit and compensation committees indicates a strengthened board oversight crucial for AsiaStrategy’s dual exposure—traditional luxury watch trading and emerging digital asset ventures.

Operationally, the company continues its focus on core trading activities while progressing its diversification into Web3-driven income streams via digital asset holdings acquired since its April 2025 IPO. This melding of legacy commerce with innovative technology platforms positions the company at an inflection point where governance rigor must match strategy breadth.

Business Model Overview: Traditions of Luxury Watch Trading

AsiaStrategy operates predominantly as an intermediary wholesaler specializing in luxury watches sourced from distributors located across Hong Kong, South America, Europe, Singapore, and Japan. Its primary customer base comprises distributors and retail sellers within Hong Kong’s vibrant watch market—a hub known for luxury brand appetite but also intense competition [S1]. The company offers a spectrum ranging from affordable sports watch models to premium international luxury pieces.

Revenue generation leans heavily on negotiating favorable import terms with suppliers against the backdrop of fluctuating currency exchange rates (notably the Swiss Franc) affecting procurement costs. The company’s ability to maintain exclusive product offerings through strong supplier partnerships confers moderate bargaining power while also buffering supply chain risk. However, this model places pressure on unit economics given gross profit margins that have historically been tight.

Competitive Landscape and Supplier Dynamics in Luxury Watches

The luxury watch distribution industry is characterized by numerous competing entities catering to discerning consumer groups sensitive to macroeconomic trends such as GDP growth rates and discretionary spending patterns. Currency movements notably impact cost bases since procurement deals settle largely in Swiss Francs; the approx 12% CHF appreciation during 2025 directly inflated AsiaStrategy’s purchase costs without a commensurate ability to raise selling prices locally due to weak market conditions [S9].

Supplier relationships represent a critical lever—successful negotiations around pricing, payment terms, or inventory exclusivity underpin differentiated access that can sustain competitive advantage amidst commoditization risks affecting lower-tier models. Customer retention ties closely to service quality and product availability given switching costs are moderate; however, the company’s concentrated revenue exposure to a handful of large distributors—accounting for roughly one-third of total sales—heightens vulnerability if client demands shift abruptly or if there is supplier disruption [S18].

Strategic Shift: Digital Assets and Web3 Opportunities

In an evident strategic pivot beyond traditional watch trading confines, AsiaStrategy has directed a portion of its IPO proceeds (~$3.5 million) into acquiring digital assets valued at approximately $2.7 million by end-2025 [S1], [S5]. This reflects a conscious diversification toward the burgeoning Web3 ecosystem where blockchain-enabled assets hold potential for novel revenue streams.

While this move may unlock new income avenues less correlated with physical goods sales cycles or geographical constraints, it concurrently introduces susceptibility to highly volatile crypto markets—as evidenced by associated unrealized valuation losses—and regulatory uncertainties surrounding such assets globally [S1]. Execution proficiency rests on management’s dual competence bridging luxury goods expertise with blockchain technology knowledge.

Convertible debt financing ($10 million raised at favorable interest terms) further underpins investment capacity for these emerging ventures without immediate dilution pressure on equity holders [S4], [S6].

Growth Catalysts: Market Expansion and New Revenue Streams

AsiaStrategy’s articulated growth strategy hinges on expanding market penetration beyond densely served Hong Kong geographic segments by onboarding additional distributors and retail outlets potentially outside traditional hubs [S1]. Broadening product portfolios toward diverse luxury brands along affordability spectra could capture complementary demand segments.

Simultaneously, successful monetization along the Web3 dimension hinges on converting digital asset holdings into profitable cash flow through trading gains or ancillary services within crypto ecosystems that accompany tokenization trends.[S1]

Growth visibility might be tracked through KPIs such as increased distributor count figures or sequential expansion in digital portfolio valuations balanced against realized earnings impacts.

Key Risks: Customer Concentration, Market Volatility, and Regulatory Environment

AsiaStrategy’s operational continuity faces risks stemming from concentrated dependence on few customers whose aggregate revenues approximate over one-third of total sales; disruption or reduced orders from these clients could materially impact financial outcomes [S18].

Moreover, digital asset holdings expose profitability to abrupt market swings inherent in cryptocurrency valuations with unrealized losses recorded—a nascent line of business carrying regulatory scrutiny risks that could hamper business model adaptiveness or capital deployment flexibility.[S1]

Currency risk from exchange rate fluctuations remains salient given procurement settlements predominantly in Swiss Francs juxtaposed against HK dollar local market pricing limitations.

Finally, identified internal control weaknesses relating to financial reporting processes underscore challenges related to accounting complexity compliance under U.S. GAAP standards for combined physical-digital assets enterprises [S1].

Milestones Ahead: Governance Stability, Digital Asset Performance, and Market Penetration

Key forthcoming junctures include assessing Q2/Q3 operational filings for evidence of execution against expansion initiatives both geographically and within the Web3 segment sphere. Monitoring board committee effectiveness under Mr. Tao’s chairmanship will provide insights into corporate governance robustness aligned with complex multi-industry exposure.

Tracking shifts in digital asset valuations will also be pivotal given their direct linkages to reported profitability metrics reported up through Q1/Q2 of fiscal 2026.

Then monitoring changes—or stabilization—in customer concentration levels alongside supplier terms will reflect market position resilience during ongoing economic cycles.[S2], [S3]

Financial Snapshot: Liquidity, Profitability, and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1464381 | |

| 2025-12-31 | ||

| Total debt | $5mm | |

| 2025-12-31 | ||

| Net debt | $4mm | |

| 2025-12-31 | ||

| Current assets | $32mm | |

| 2025-12-31 | ||

| Current liabilities | $5mm | |

| 2025-12-31 | ||

| Current ratio | 6.51x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Strong liquidity reflected by a current ratio above six stems from sizeable current assets primarily inventories designed to support anticipated post-period sales expansions versus relatively limited current liabilities at year-end reporting date.[F1]

Debt includes $10 million convertible notes issued October 2025 facilitating capital availability for diversification efforts offset by net debt after cash approximating $3.8 million indicating modest leverage consistent with medium-term growth ambitions.[S4], [F1]

Overall financial positioning offers a foundation capable of supporting strategic shifts while requiring vigilant cost management amidst margin pressures stemming from structural product pivots.

Disclaimer: This analysis is prepared solely for informational purposes based on disclosed SEC filings and public data as of specified dates without any investment recommendation or offer to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments