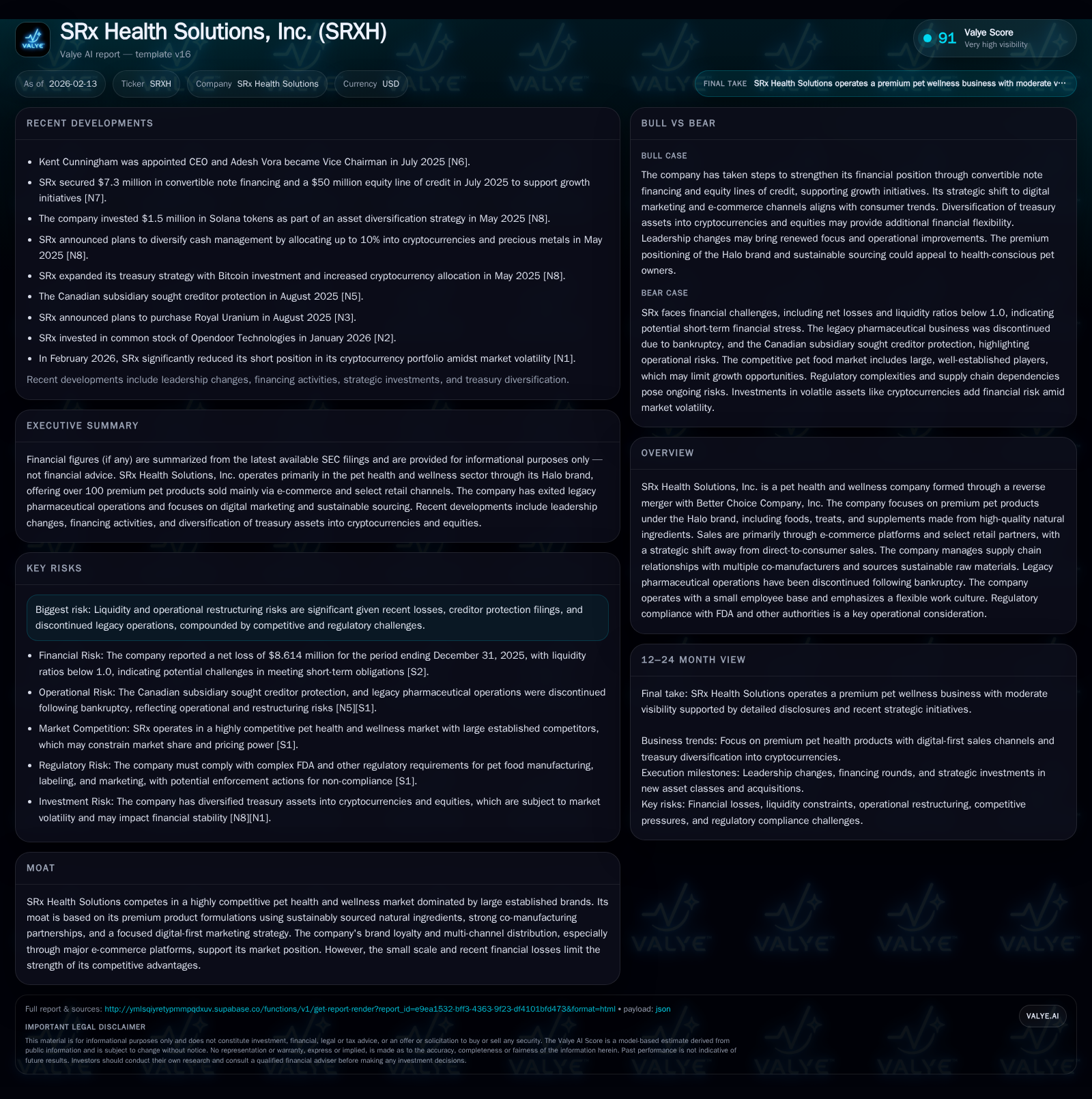

SRx Health Solutions: From Pharmaceutical Ruins to Premium Pet Wellness Amid Financial Strains

SRx Health Solutions has undergone a profound transformation pivoting from bankrupt pharmaceuticals to natural pet health products, navigating financial and operational challenges.

SRx Health Solutions (SRx) has reshaped its identity following the bankruptcy and exit of legacy specialty pharmaceutical operations. Leveraging the Halo brand acquired via reverse merger with Better Choice Company, SRx now concentrates on premium pet wellness products sold primarily through e-commerce and retail partners. Despite promising brand positioning in a competitive market, the company confronts ongoing liquidity pressures, tight balance sheet ratios, and operational risks tied to supply chains and regulatory compliance. Leadership continuity and strategic financing remain critical to its ability to capitalize on growth opportunities while mitigating persistent financial headwinds.

From Pharmaceuticals to Pets: Tracing SRx’s Dramatic Pivot

SRx Health Solutions’ evolution is as much a story of survival as reinvention. Historically rooted in specialty pharmaceuticals — with a string of acquisitions aimed at building scale — its legacy operations succumbed to financial distress culminating in bankruptcy. This collapse necessitated the winding down of its traditional business lines, reported now as discontinued operations post-2025 [S1]. The decisive turning point was the reverse merger with Better Choice Company, Inc., which brought under SRx’s reporting umbrella the Halo pet health and wellness brand.

This transition marked not just a change in product focus but an existential shift from complex healthcare services to consumer-facing premium pet nutrition. It also distanced SRx from pharmaceutical regulatory burdens but introduced new operational paradigms centered around product innovation for pets, supply chain management, and marketing in more fragmented retail environments. The pivot frames every aspect of SRx’s current strategy and challenges.

Inside Halo: Premium Pet Wellness in a Competitive Market

The Halo portfolio encompasses over 100 SKUs spanning kibble, canned food, freeze-dried raw options, chews, supplements, and dental care products formulated for dogs and cats [valye_report_excerpt][S1]. Characterized by high-quality natural ingredients sustainably sourced, this positioning aims at health-conscious pet owners demanding transparency and science-backed nutrition.

The company leverages longstanding partnerships with multiple co-manufacturers maintaining rigorous quality standards — a critical differentiator in an industry rife with recalls and trust issues among consumers. Yet the premium segment is fiercely contested by giants like Nestlé Purina and Blue Buffalo; while Halo’s formulations establish niche appeal, SRx’s relatively small scale limits pricing leverage and distribution breadth.

Brand loyalty appears palpable among dedicated customers invested in holistic wellness narratives; however, scaling these sentiments beyond loyalists remains an uphill task given mounting competition.

The E-commerce Gambit: How Channel Shifts Define SRx’s Distribution Strategy

Distribution is undergoing a significant recalibration. Until mid-2024, SRx maintained direct-to-consumer sales through halopets.com but strategically exited this channel, redirecting customers toward larger e-commerce partners such as Amazon, Chewy, Petflow, Thrive Market, and Vitacost alongside select brick-and-mortar retailers [S1]. This shift reflects pragmatic acknowledgment of rising customer acquisition costs in DTC models alongside broader retail trends favoring digital marketplaces.

E-commerce platforms offer scale reach but compress margins due to platform fees and promotional demands. Moreover, relying heavily on third parties elevates risks around pricing control and customer data ownership. Nonetheless, this multi-channel distribution approach supports incremental penetration into major online shopping ecosystems where consumers increasingly purchase pet supplies.

International distribution is nascent but potentially promising long-term revenue contributor as globalization intensifies demand for premium pet wellness.

Balance Sheet Under Pressure: Liquidity Challenges and Financial Realities

Despite positive strategic moves, SRx walks a financial tightrope. As of December 31, 2025, cash on hand stood at approximately $13 million against current liabilities surpassing $23 million — yielding a concerning current ratio near 0.8 [F1]. Such metrics underscore liquidity stress that could restrict operational flexibility.

Revenue generation remains modest given the recent scale-up phase; trailing revenues last reported at about $6.5 million for the year ended September 30, 2025 [S1]. Meanwhile, net losses ballooned to $8.6 million by year-end December 2025 [F1], reflecting elevated costs associated with restructuring efforts, marketing investments in the pet category, and legacy liabilities winding down.

Filings explicitly highlight risks regarding capital access constraints going forward along with potential dilution or restructuring measures necessary to sustain growth ambitions [S1][S2]. This financial backdrop frames an urgent imperative for efficient cash management coupled with securing additional financing sources.

Leadership and Talent: The Critical Role of Key Personnel Amid Change

SRx’s lean organizational footprint translates to heavy reliance on board members and a compact management cadre [S1]. The company warns that losing key personnel could jeopardize business plan execution during this fragile turnaround phase when agility and domain expertise are paramount.

Retaining talent amidst public company compliance requirements poses additional challenges as leadership balances growth-focus with regulatory rigor unaccustomed from earlier private-stage operations. Notably absent is key-man insurance protection that could mitigate disruption risks.

Effective knowledge transfer mechanisms remain vital to avoid operational hiccups as the company scales its new core business away from legacy pharma shadows.

Regulatory Landscape and Operational Risks Facing SRx

Though no longer pharmaceutical-centric, SRx remains vigilant regarding regulatory oversight impacting pet foods and supplements — categories scrutinized by FDA among others for ingredient safety and labeling claims [valye_report_excerpt][S1]. Stringent standards necessitate continuous monitoring of manufacturing partners’ compliance.

The company's dependence on co-manufacturers is both an asset—enabling flexible production scaling—and a vulnerability since lapses by external facilities could trigger recalls or disrupt supply chains. Maintaining robust quality assurance protocols thus forms a strategic cornerstone.

Global expansion ambitions add regulatory complexity given varying international standards requiring tailored approaches.

Strategic Investments Beyond Core: Cryptocurrency and Opendoor Stakes

In an intriguing move diverging from core competency focus, SRx recently reduced its short position in cryptocurrencies amid volatile markets [N1] while also acquiring minority shares in Opendoor Technologies—a real estate technology firm—earlier in 2026 [N2].

These initiatives may reflect attempts to diversify asset bases or generate ancillary income streams amid constrained operating cash flows. However, they introduce heightened exposure to unrelated market dynamics that could divert management attention or inflate risk profiles if market conditions worsen.

Close scrutiny will be warranted on how these non-core investments fit within broader capital allocation philosophies going forward.

Competitive Moats or Mere Ripples? Assessing SRx’s Market Position

SRx asserts competitive moats anchored in premium formulation quality, co-manufacturer alliances, brand loyalty within targeted niches, and digitally savvy multi-channel distribution strategies [valye_report_excerpt]. This constellation constitutes meaningful differentiation against generic mass-market brands.

However, when contextualized against titans wielding economies of scale far beyond SRx's footprint—the moat narrows considerably. Persistent losses diminish resources available for marketing muscle or innovation cycles essential for sustaining relevance.

Thus far, market momentum remains tethered to niche appeal rather than mainstream dominance—a distinction crucial for realistic expectation setting among stakeholders.

Future Pathways: Growth, Financing Needs, and the Road Ahead

Looking ahead, SRx navigates between aspirations of measured growth leveraging its specialized product portfolio against practical necessities of shoring up financial stability [S1][S2].

Achieving sustainable profitability likely hinges on securing incremental working capital or equity funding while continuing execution discipline around cost controls.

Possible scenarios include expanded geographic reach leveraging international channels or deeper penetration within existing e-commerce ecosystems balanced against prudent inventory management. Conversely, failure to raise sufficient capital or retain key talent could precipitate further reorganization or strategic pivoting.

Management must balance these opposing forces carefully — growth versus survival — crafting adaptable yet coherent plans aligned with evolving market landscapes.

This analysis draws upon publicly available SEC filings dated through February 13th, 2026 [S1][S2], verified company statements summarized in the Valye report excerpt dated February 13th 2026 [valye_report_excerpt], recent news releases [N1][N2], and reported financial data [F1]. It does not constitute investment advice but aims to provide nuanced understanding of SRx Health Solutions’ current status and prospects based on disclosed information. Readers should undertake their own comprehensive due diligence respecting inherent uncertainties inherent in transitional companies such as SRx.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments