Simpson Manufacturing’s Growth Fueled by Market Penetration and Operational Investments

Solid historical growth underpinned by product diversification and engineering expertise positions Simpson Manufacturing for continued expansion amid housing market cyclicality.

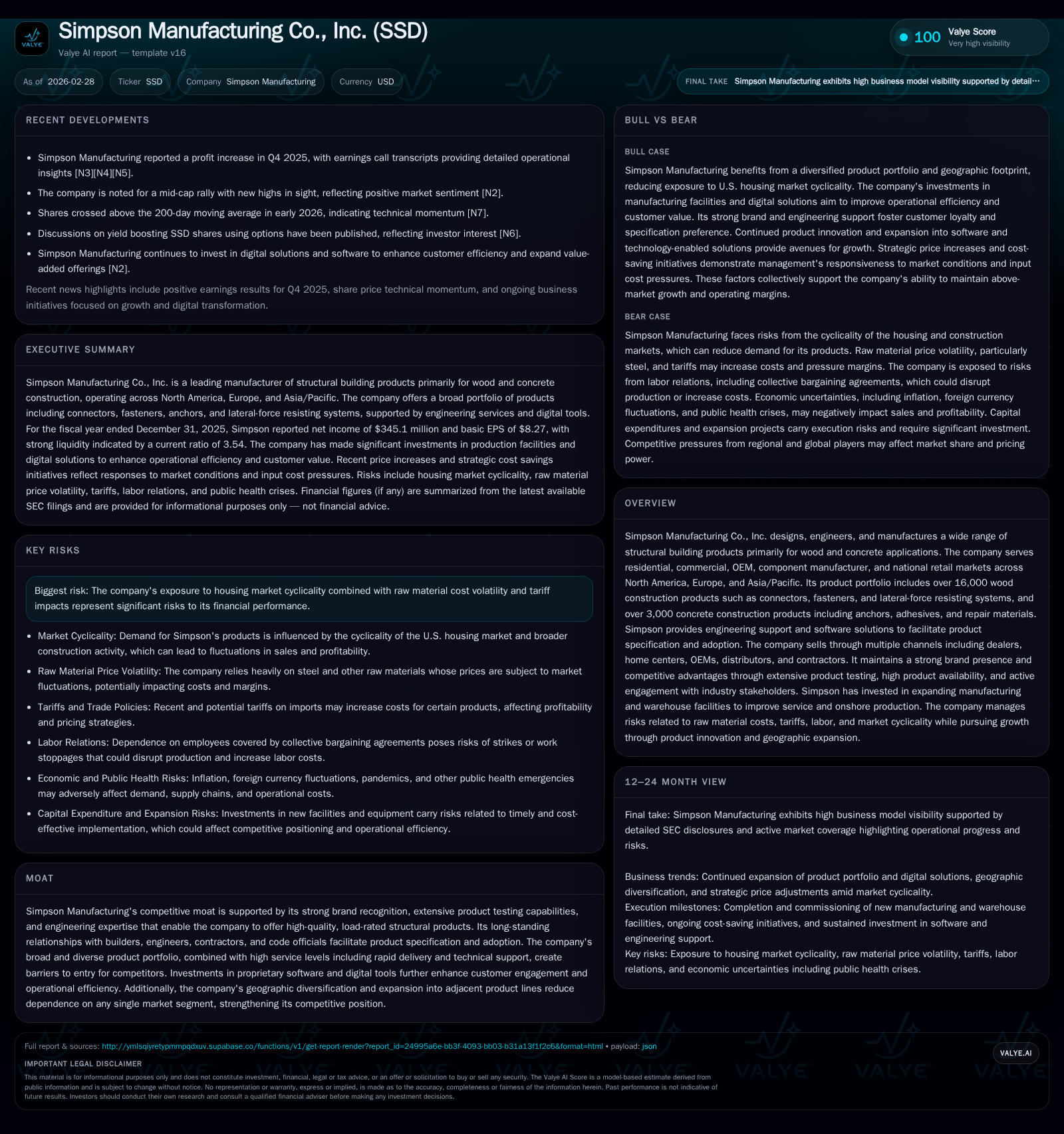

Simpson Manufacturing Co., Inc. has demonstrated consistent growth in operating income and net income over recent years, driven primarily by strong demand in North American wood and concrete building products. The company’s broad product portfolio, engineering services, and digital tools support customer adoption and market penetration. While housing market volatility and raw material cost pressures pose risks, Simpson’s active capital allocation—highlighted by substantial share repurchases and dividends—and investments in manufacturing infrastructure underpin its strategic ambitions. Future growth is expected to hinge on expanding customer segments, geographic diversification, and innovation within engineered products.

Business Overview

Simpson Manufacturing Co., Inc. designs, engineers, and manufactures an extensive range of structural building products focused primarily on wood and concrete applications. The company’s portfolio includes thousands of wood construction products such as connectors, fasteners, lateral-force resisting systems, as well as concrete construction products like anchors and adhesives serving residential and commercial construction markets along with OEMs and national retailers across North America, Europe, and Asia/Pacific [S1][S6].

The firm’s competitive advantage stems from its strong brand recognition, rigorous product testing capabilities, engineering expertise facilitating technical support, as well as proprietary software solutions supporting product specification. Its expansive portfolio paired with rapid delivery service helps maintain customer loyalty among builders, engineers, contractors, and code officials [S1][S6].

Historical Financial Performance

Simpson's financials demonstrate sustained momentum over recent years despite cyclical headwinds in construction markets. From 2017 through 2025,[F1] the company reported revenue growth of approximately 15.7%. Operating income increased 6.5% year-over-year to $458 million in 2025 versus $430 million in 2024; net income similarly rose 7.1% to $345 million (see Table below). Operating cash flow surged by more than a third to nearly $459 million in the latest fiscal year—providing substantial liquidity for ongoing investments and shareholder returns.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 345 | 459 | 458 | 161 | +7.1% |

| 2024 | 322 | 338 | 430 | 180 | -9.0% |

| 2023 | 354 | 427 | 475 | 89 | +6.0% |

| 2022 | 334 | 400 | 459 | 62 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 48 | 120 | 298 |

| 2024 | 47 | 100 | 158 |

| 2023 | 45 | 50 | 338 |

| 2022 | 44 | 79 | 337 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures available through FY2017; operating income from FY2022 onwards.[F1]

Growth since early this decade has been supported by strategic acquisitions adding revenue alongside integrated profit increases as highlighted by management commentary [S18][S19]. In addition to organic advancement in core markets, the business has benefited from realigning sales teams to better target end markets (residential/commercial/OEM/retail), improving distribution efficiency, enhancing field sales presence plus expanded engineering teams [S18][S19].

Segment Dynamics and Geographic Diversification

North America commands the lion’s share of sales (78%), supplemented by Europe (21%) where the company offers both wood- and concrete-based products tailored to local regulations and commercial/residential demand profiles [S6][S16]. Asia/Pacific is a smaller contributor but shows growth potential due to targeted market efforts.

Within North America:

- Residential remains the largest end-market influenced heavily by U.S housing start cycles.

- Commercial construction benefits from strength across specialty connectors and anchoring products but faces competitive dynamics.

- OEMs/Component Manufacturers represent incremental channels enhanced via proprietary software aiding design workflows.

Price escalations implemented mid-2025 aimed to offset inflationary impacts contributed materially to top-line increases despite modest volume declines aligned with weakening housing starts forecasts [S10][S12]. Concrete product lines saw accelerated growth (~6%) outpacing wood product shipments which grew just under ~5% year-to-date—highlighting diversification benefits within product mix.

Operational Investments & Innovation Pipeline

The company continues emphasizing capital projects focused on manufacturing efficiency gains including its new Gallatin (Tennessee) facility bringing heat treating/coating processes onshore complementing existing anchor production [S19]. Expansion projects near Columbus (Ohio) underpin increased capacity investment totaling approximately $150–160 million capex deployed through early/mid-2026 [S20].

Alongside physical asset investments there is strategic emphasis on digital transformation encompassing:

- Enhanced engineering software tools promoting ease of use for customers specifying complex structural connectors.

- Data-driven inventory management systems aimed at high availability minimizing backorders or delayed fulfillment—a critical factor given infrastructure project timeliness pressure.

- Development of new load-rated prefabricated lateral-force resisting systems targeting commercial construction codes compliance as well as modular building trends [S6].

Risks: Cyclicality & Supply Chain

Despite strengths Simpson faces cyclicality risks tied tightly to housing market fluctuations,[S1] consumer confidence swings,[S22] interest rate shifts affecting borrowing costs for builders/homeowners,[S25] raw material price volatility,[S10] plus logistics or energy cost spikes impacting gross margins [S22][S25].

Additional challenges include:

- Consolidation of distributor customers increasing bargaining power risk potentially compressing prices.[S22]

- Exposure to tariffs or import restrictions undermining profitability if not fully recoverable via price adjustments.[S22]

- Reliance on third-party transport firms exposing the firm to disruption or elevated freight expenses impacting supply chain reliability.[S21]

- Legal claims related to product failures or installation errors remain an inherent risk despite strict quality controls.[S25]

The company mitigates some risk via geographic diversity but remains predominantly concentrated (>75%) in North American residential/commercial sectors making it vulnerable during downturns.[S23]

Capital Allocation & Returns

Simpson demonstrates disciplined capital deployment balancing growth investments with shareholder returns [F1][S9][S20]:

- Robust free cash flow estimated near $298 million in fiscal year ended December 2025 (operating cash flow less capital expenditures).

- Since early-2022 more than $490 million returned via dividends (

$48 million annually) plus significant buybacks totaling over two million shares repurchased (5% of shares outstanding at period start).[F1][S9] - In October 2025,the Board authorized an additional $150 million buyback authorization effective through December 31 of that year supporting ongoing shareholder return objectives.[N1][N5]

Dividend increases have been consistent albeit modest reflecting confidence balanced against cyclical risks inherent in the underlying housing markets.[F1]

Future Outlook – What To Watch

While formal guidance beyond recent earnings commentary has not been provided,[N1] key watch points include:

- Progress against planned rollout of new product innovations especially prefabricated systems designed for modular building which can provide higher margin uplift.

- Ability to sustain premium pricing amid raw material cost inflation without losing volume share given competition dynamics.[N4]

- Execution against manufacturing footprint expansions enhancing supply responsiveness allied with improved delivery lead times.

- Growth trajectories across Europe/Asia-Pacific segments where penetration is less mature but represents incremental opportunity.

- Impact of broader macroeconomic variables such as mortgage interest rate trends influencing residential construction activity.

- Continued development of digital sales/support platforms potentially creating stickier client relationships through integrated design/specification tools.

To the extent the company can maintain volume growth exceeding U.S housing start rates (targeting outperformance historically around +250 basis points), while managing margin pressure from input costs through operational efficiencies,the earnings per share growth should continue outpacing revenue expansion per stated ambitions[S18][S19].

Conclusion

Simpson Manufacturing Co., Inc.’s track record embodies steady financial performance supported by deep domain expertise in engineered load-rated solutions across wood/concrete substrates used throughout residential/commercial construction globally albeit weighted heavily toward North America. Its strategic investments in physical assets along with digital capabilities form a foundation for sustained above-market growth even amid cyclical challenges common to construction-related suppliers. Prudent capital allocation including aggressive buybacks alongside growing dividends signals financial discipline while reinforcing appeal for long-term stakeholders focused on resilient industrial franchises addressing essential infrastructure needs. However, prevailing macroeconomic uncertainties including raw material cost variability plus evolving trade policy environments require close monitoring. Overall, Simpson leverages strong brand moats with diversified yet complementary offerings positioning it well for mid-term sustainable expansion within an otherwise volatile industry backdrop.

Disclaimer: This report is prepared strictly for informational purposes reflecting data available through February 27, 2026 sourced from regulatory filings ([F1],[S#]) and reported news ([N#]) without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments