E.W. Scripps Co Confronts Profitability Challenges With Strategic Asset Sales and Transformation

The company balances growth in multi-platform reach and local broadcast strengths against recent operating losses and a major enterprise overhaul.

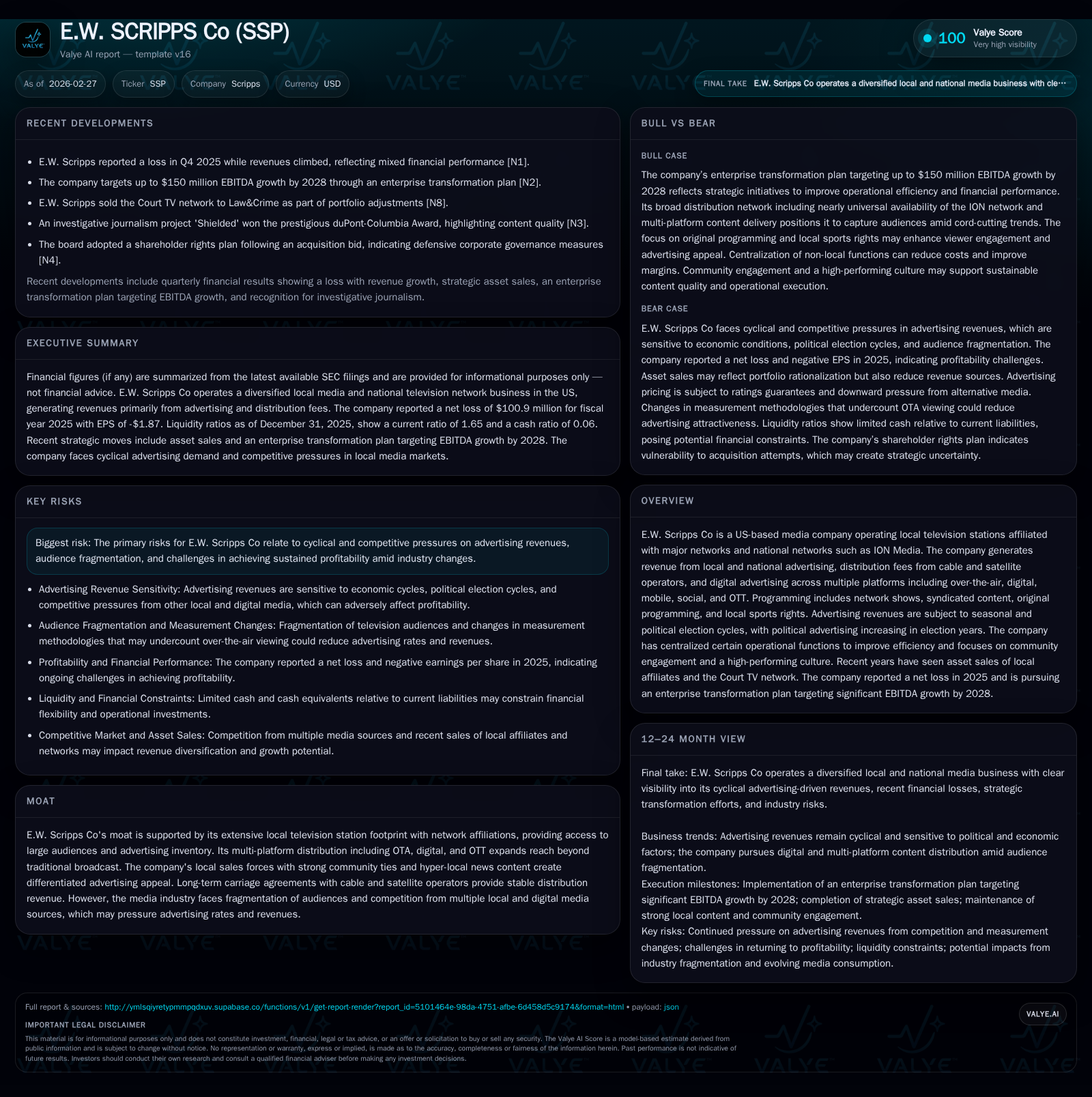

E.W. Scripps Co has experienced fluctuating financial performance marked by a net loss in 2025 despite a positive operating income, reflecting cyclical political advertising impacts, rising programming costs, and restructuring charges. Management is executing strategic asset sales including the Court TV network and select local affiliates while pursuing an enterprise transformation plan targeting $125–150 million in annualized EBITDA growth by 2028 through cost efficiencies and technology adoption. The company maintains a strong local station footprint with stable carriage agreements amid audience fragmentation challenges.

Historic Performance Shifts: Revenue Growth Contrasted With Earnings Volatility

E.W. Scripps Co’s financial history illustrates tension between revenue trends and profitability. Revenues expanded from $245.7 million in 2014 to nearly $257.0 million in 2017 [F1]. More recently, operating income swung dramatically from a $428.3 million gain in 2022 to a substantial loss of $-753.2 million in 2023 before recovering to $184.0 million in 2025 [F1]. Net income has reflected this volatility, with a notable net loss of $-100.9 million recorded in 2025 [F1].

Operating cash flow also contracted sharply from $365.7 million in 2024 to $53.1 million in 2025, while capital expenditures decreased from $65.3 million to $46.6 million over the same period [F1]. This resulted in a modest positive free cash flow of approximately $6.5 million in 2025.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | 53 | 184 | 47 |

| 2024 | 366 | 412 | 65 |

| 2023 | 112 | -753 | 60 |

| 2022 | 311 | 428 | 46 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 7 |

| 2024 | 300 |

| 2023 | 52 |

| 2022 | 266 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures latest available are through FY2017; other metrics are as per latest filings [F1]

Margin pressures stem from increased programming costs including affiliation fees paid to major networks, as well as operational expenses related to staffing and production [S7][S15]. While the company’s station footprint has expanded via acquisitions like ION Media, profitability remains challenged by cyclical advertising demand and restructuring charges.

Advertising Revenues: Seasonality and Political Cycles

Advertising constitutes the majority of revenues within the Local Media segment, comprising local business sales, national ads, digital advertising, and political spending which causes pronounced seasonality [S7][S14][S15]. Political advertising accounted for roughly 1.5% of Local Media revenues during the non-election year of 2025 but increases substantially during even-year federal, state, and local elections—with presidential election years further amplifying this effect [S14][S15].

This leads to uneven quarterly earnings patterns driven by upfront commitments aligned with campaign cycles followed by scatter market adjustments closer to ad runs [S15]. The company’s local sales teams leverage community ties to provide targeted inventory attractive for advertisers seeking hyper-local engagement—a key differentiator amid broad audience fragmentation.

Programming arrangements include contractual obligations where networks provide content with associated affiliation fees paid by Scripps; networks retain substantial advertising time during broadcasts, influencing revenue sharing dynamics [S7]. Expansion into digital platforms including OTT apps extends audience reach beyond traditional broadcast but faces competition from streaming services.

Strategic Asset Rationalization: Divestitures Including Court TV

Management has pursued portfolio streamlining through selective divestitures aligned with core local broadcast focus [N3][S17]. The sale of Court TV was completed in February 2026, resulting in a non-cash charge of approximately $19.5 million reflecting asset value adjustments [N3][S17].

Additionally, agreements to sell WFTX (Fox affiliate; $40 million) in Fort Myers, Florida, and WRTV (ABC affiliate; $83 million) in Indianapolis are progressing toward closing pending regulatory approvals expected by early March 2026 [N3][S17]. These disposals reduce geographic breadth but improve capital allocation flexibility.

Such moves balance shedding steady but lower-growth assets against expense reduction supporting broader transformation goals amidst competitive pressures.

Enterprise Transformation Plan Targeting EBITDA Growth by 2028

In February 2026, the company announced an enterprise-wide transformation plan targeting annualized EBITDA growth of $125–150 million by fiscal year-end 2028 [N2][S1]. Key components include:

- Cost Savings via Operational Centralization: Consolidating functions such as master control, traffic management, graphics production, and research into fewer hubs reduces fixed costs while enabling stations to focus on content creation and sales efforts [S7].

- Revenue Growth through Technology: Leveraging AI-driven automation enhances pricing optimization on existing inventory; expanding multi-platform offerings including OTT products aims to broaden monetizable audiences beyond traditional over-the-air transmissions [N2].

This initiative aligns with industry trends emphasizing digital monetization to offset cord-cutting impacts.

Capital Structure Amid Operating Losses

E.W. Scripps Co carries a complex debt profile comprising senior secured notes maturing between January 2029 and August 2030, unsecured notes due July 2027 through January 2031, plus term loans expiring between May 2026 and November 2029 [S4][S5][S6][S29]. The issuance of $750 million senior secured second lien notes at a coupon near 9.875% reflects prevailing risk pricing post-portfolio adjustments.

Refinancing activities executed in April 2025 included repayments totaling hundreds of millions toward term loans alongside redemption of older high-coupon notes [S17]. Despite reported losses, liquidity remains adequate with approximately $27.9 million cash on hand at year-end and a current ratio near 1.65 indicating no immediate solvency concerns [F1][S4].

Maturities concentrated over the next few years necessitate monitoring for refinancing needs or capital allocation decisions.

Capital Allocation: Cash Flow Trends and Shareholder Returns

Operating cash flow declined significantly from $365.7 million in FY24 to around $53 million in FY25 amid higher operating costs and restructuring charges [F1]. Capital expenditures reduced from about $65 million to $46.6 million supporting necessary infrastructure investment.

Free cash flow remains positive but limited at roughly $6.5 million after capex constraints discretionary spending for dividends or buybacks [F1]. Historically meaningful dividends paid until FY20 have ceased thereafter consistent with prudent capital preservation amid profitability challenges; no significant share repurchase activity is disclosed currently [F1][S26][S28].

This conservative approach reflects reinvestment priorities into digital capabilities amid legacy media headwinds.

Industry Context: Audience Fragmentation Challenges Local Media Economics

The company operates amid accelerating audience fragmentation driven by OTT platform proliferation diluting traditional linear viewership bases—pressuring advertising rates and retransmission fee revenues underpinning distributor payments [S10]. Although measurement improvements seek better capture of viewing data via set-top boxes, risks persist that over-the-air consumption may be undervalued potentially weakening broadcaster leverage.

Nonetheless, Scripps’ emphasis on hyper-local news content created by multi-skilled reporters across platforms supports community engagement that appeals to advertisers targeting precise local audiences beyond mass national campaigns [S21]. Balancing syndicated popular programming with original content further enhances retention despite cord-cutting pressures.

Key Upcoming Milestones for Investors

Investors should monitor upcoming distribution agreement renewals impacting nearly one-quarter of subscriber households — terms can materially affect recurring carriage revenue given multi-year contract durations [S7]. Additionally, progress on operational centralization milestones under the transformation plan will indicate execution capability toward targeted EBITDA gains [N2]. Further asset rationalizations remain possible as the company sharpens focus amid competitive consolidation.

This report synthesizes publicly available filings and news sources without offering investment advice or forecasts beyond cited management disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments