STAAR Surgical Co Defies Market Pressures While Reshaping Ophthalmic Implantable Lens Growth

Despite recent setbacks including a terminated merger and widening losses, STAAR Surgical leverages FDA approval expansion and leadership changes to bolster its implantable lens franchise.

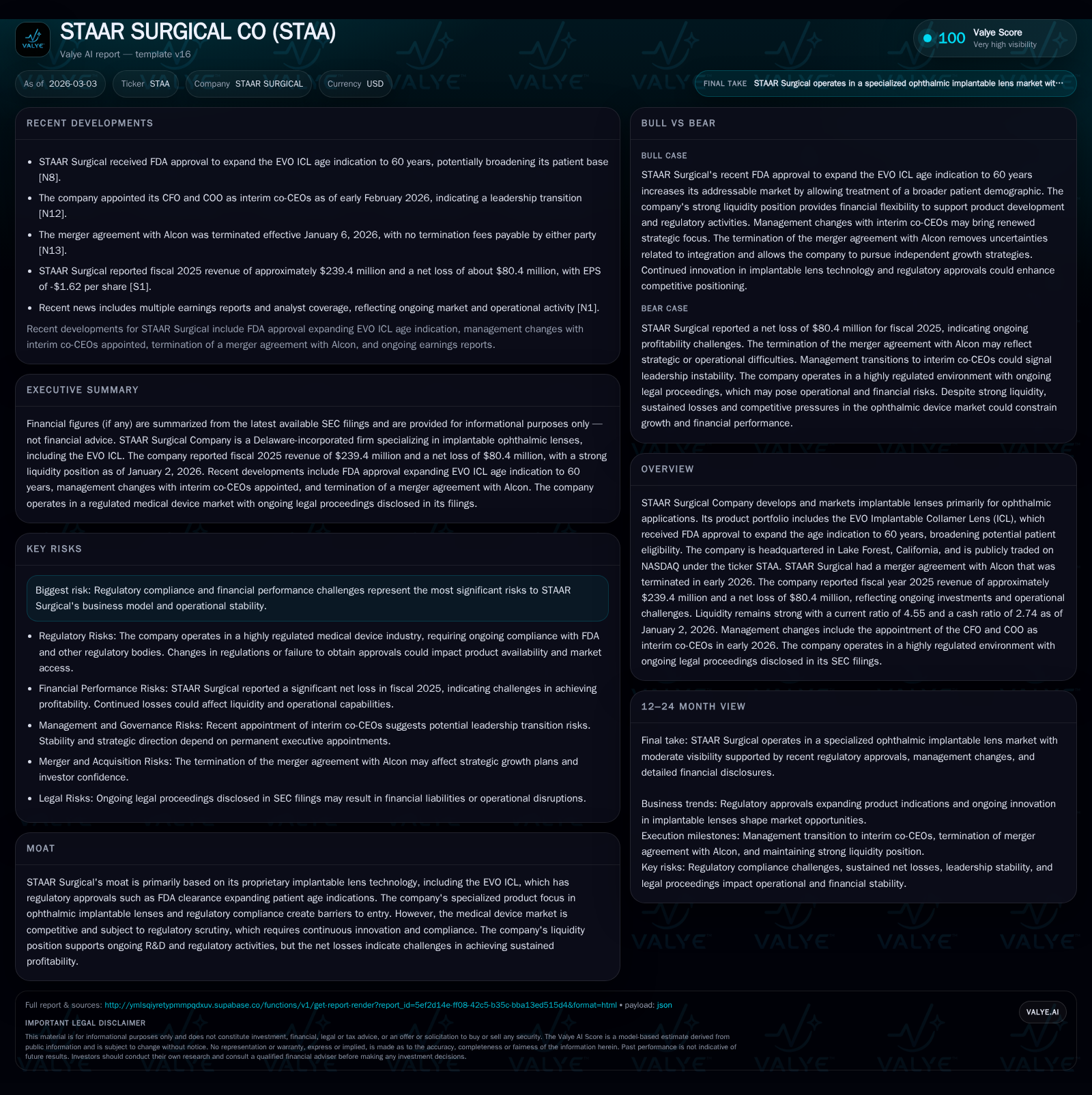

STAAR Surgical Company experienced a sharp revenue decline of nearly 24% in fiscal 2025 alongside significant operating losses, influenced in part by growing R&D expenses and disrupted operational momentum. The collapsed Alcon merger deal dealt a blow to anticipated synergies and strategic direction but did not impair the company’s regulatory progress evidenced by FDA approval expanding EVO ICL patient age eligibility to 60 years. Leadership transitions in early 2026 have installed interim co-CEOs from within senior management, aiming to stabilize execution. Strong liquidity with a 4.55 current ratio supports continued investment, though near-term profitability remains elusive. The coming quarters will require close monitoring of revenue recovery post-FDA expansion and cash flow dynamics amid persistent regulatory and competitive challenges.

Historic Sales Trajectory and Evolving Profitability Dynamics

STAAR Surgical’s revenue trajectory over the past four fiscal years exhibits volatility with a marked downturn in FY2025. Revenue declined 23.7% year-over-year to $239.4 million from $314 million in FY2024 [F1]. This reversal interrupted modest growth seen through FY2023 when top-line peaked at approximately $322 million. Operating income mirrored this trend emphatically: from $28.1 million operating profit in FY2023, STAAR swung to an operating loss of $91.7 million in FY2025, a staggering decline that underscored intensifying operational headwinds including increased R&D investments aimed at product pipeline advancement [F1]. Net income followed suit with a loss of $80.4 million representing roughly -23.4% annualized ROE relative to equity of about $344 million [F1].

The company reported negative operating cash flow for FY2025 at -$34.2 million compared to positive mid-teens millions in prior years [F1], signaling diminishing conversion of accounting earnings into liquidity amid possibly higher working capital outflows or delays in receivables collection typical in implantable device sales cycles where procedure volume can exhibit cyclical and regulatory timing effects (analysis). Capex declined drastically by 75%, suggesting management's focus on curtailing non-essential investitures to preserve cash amid earnings pressure [F1]. These metrics collectively paint a picture of mounting cost pressures coinciding with delayed revenue recognition tied to regulatory approvals and market adoption cycles common for implantable lenses requiring specialist surgeon uptake.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 239 | -80 | -34 | -92 | -23.7% | -298.1% |

| 2024 | 314 | -20 | 16 | -13 | -2.6% | -194.7% |

| 2023 | 322 | 21 | 15 | 28 | +13.4% | -44.9% |

| 2022 | 284 | 39 | 36 | 44 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -40 | -23.4 |

| 2024 | -8 | -5.1 |

| 2023 | -4 | 5.5 |

| 2022 | 18 | 11.7 |

Source: SEC companyfacts cache [F1].

Financials emphasize stark deterioration in underlying profitability and cash generation despite top-line scale at pre-downturn levels, stressing critical inflection point for STAAR's operational health [F1].

Implications of the Alcon Merger Termination on Strategic Outlook

The pivotal strategic event for STAAR Surgical was the termination of its merger agreement with Alcon Research LLC which was effective January 6, 2026 [S11]. This came after shareholders significantly voted against approving the merger proposal as shown by nearly double the opposing votes relative to supporting votes (27M vs ~15M shares) [S9]. The collapse of the deal eliminated prospects for anticipated synergies including broader commercialization capabilities, cost sharing in R&D, and scaling benefits from combining complementary ophthalmic portfolios.

Moreover, management acknowledged potential distraction impacts on business continuity during merger negotiations which may have contributed to operational disruptions reflected in financial performance [S12]. The loss of merger-driven capital restructuring possibilities preserves STAAR’s independent but financially constrained status requiring internal resource prioritization.

The company faces heightened pressure maintaining competitiveness against larger integrated ophthalmic firms given limited scale and must now pursue growth on its standalone merits—principally hinging on innovative product expansion such as EVO ICL enhancements along with all-important regulatory approvals discussed below.

EVO Implantable Collamer Lens Expansion: Unlocking Broader Patient Access

In February 2026, STAAR secured FDA approval extending the age indication for its flagship EVO Implantable Collamer Lens (ICL) from previous limits up to age approximately 45 out to age 60 [N12]. This regulatory success materially expands patient eligibility, increasing the pool of adults suitable candidates for vision correction through implantable lens technology that offers an alternative to laser refractive surgery.

This expanded labeling leverages STAAR’s proprietary biocompatible collagen-based lens technology that differentiates its product by virtue of flexibility, compatibility, and reversibility — qualities valued highly by cataract surgeons considering implantation scenarios beyond conventional young adult profiles (analysis). Regulatory hurdles remain substantial barriers within this domain thus maintaining STAAR’s technical moat but concurrently entail costly ongoing compliance burdens [S5].

The EVO ICL extension opens a pathway for renewed incremental revenue generation provided commercialization efforts successfully align ophthalmologist adoption with patient demand trends.

Leadership Transition Effects on Operational Strategy

January-February 2026 marked key leadership modifications with departure of CEO Stephen Farrell effective end-January along with board reshuffling efforts involving new appointments including three investment-oriented directors tied to Broadwood Capital concentration [S16][S26][S28]. Concurrently, the former CFO Deborah Andrews and COO Warren Foust were named interim co-CEOs as of February [N11], blending financial stewardship with operational expertise at the helm.

These dual leadership roles suggest a deliberate approach designed to stabilize ongoing operations while managing cost structures tightly during recovery phase post-merger defeat (analysis). Both executives possess deep company tenure enhancing continuity while also addressing investor concerns around governance evidenced by board composition changes around the same period [S27]. This tandem leadership model is expected to shepherd strategic initiatives surrounding product commercialization and capacity building for sustaining competitive positioning.

Liquidity Strength and Capital Allocation under Pressure

At fiscal year-end January 2, 2026, STAAR maintained substantial liquidity characterized by $153 million cash & equivalents underpinning a conservative current ratio exceeding four times current liabilities (current ratio = 4.55) [F1]. Such ratios are robust relative to sector peers often challenged by high working capital demands.

Nevertheless, operating cash flow was negative ($34 million) underscoring ongoing burn exceeding capital expenditures which were down markedly (-75% YoY) at approximately $5.8 million—reflective of capex austerity measures as the company conserves resources amid losses [F1][S7–S29].

There were no announced dividends or stock buybacks documented through multiple filings during these quarters, confirming reinvestment into sustaining R&D pipelines rather than shareholder returns [S7][S9][S13]. Capital allocation priorities clearly skew towards preserving runway rather than distributions while rebuilding profitable momentum.

Near-Term Financial Expectations and Monitoring Metrics

Wall Street awaits Q4 fiscal results cautiously optimistic for earnings growth following FDA expansion news as noted by consensus analysts cited prior to results release [N10]. Wedbush initiated coverage at neutral rating emphasizing uncertainty about translation of regulatory wins into stabilized revenue gains amid structurally impaired earnings profile [N13].

Key performance indicators going forward will include quarterly sequential improvements in implantable lens sales volumes especially within newly qualified adult cohorts post-EVO ICL label change; margin rebounds driven by fixed cost absorption gains; and reduction of operating losses aligned with tighter working capital management (analysis). Also critical will be cash burn rate moderation reflecting operational efficiencies achieved under interim co-CEO stewardship.

Regulatory Challenges and Competitive Pressures in Ophthalmic Devices

Regulatory environment remains stringent with ongoing FDA oversight emphasized prominently among risk factors due diligence disclosures [S5]. Given STAAR’s concentration on implantable collamer lenses tailored for niche ophthalmology segments, maintaining compliance involves continual costly clinical studies plus manufacturing quality controls that constrain rapid time-to-market agility.

Competitively, while proprietary lens chemistry creates entry barriers protecting technology moat, emerging competitors in refractive solutions carry risk profiles especially as laser-based alternatives persistently improve precision outcomes reducing reliance on implants (analysis).

Thus sustaining innovation cadence combined with cautious navigation through regulatory frameworks represents both necessary defense and opportunity leveraged carefully against STAAR’s limited commercial footprint.

This analysis is based solely on disclosed facts from SEC filings and authoritative news sources without speculative forecasts or investment recommendations provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments