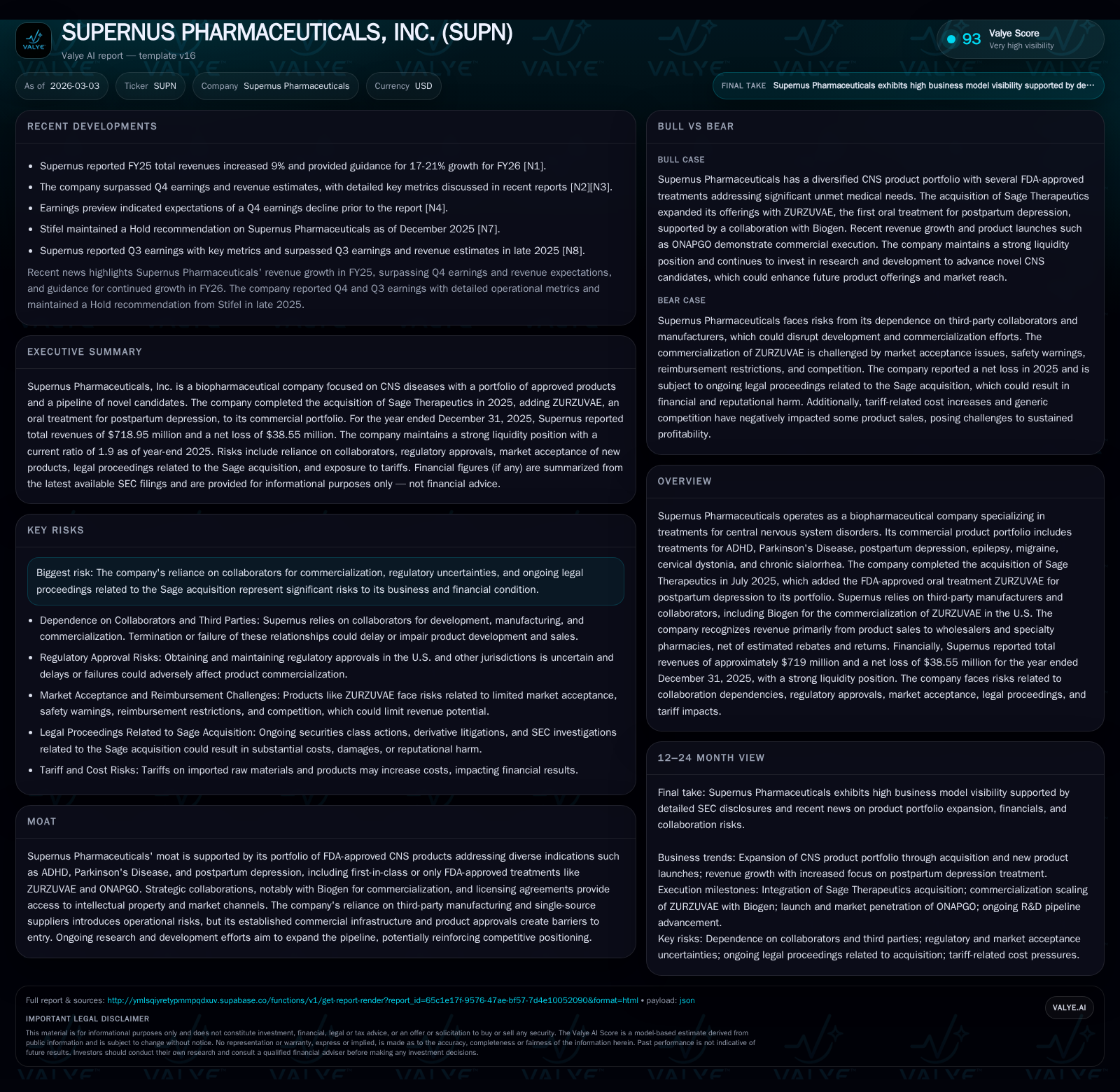

Supernus Pharmaceuticals’ Strategic Expansion and Financial Challenges in Central Nervous System Therapies

Supernus Pharmaceuticals expands its CNS therapeutic portfolio post-Sage acquisition while navigating profitability pressures and operational dependencies.

Supernus Pharmaceuticals has broadened its central nervous system (CNS) treatment offerings, notably by acquiring Sage Therapeutics and integrating ZURZUVAE for postpartum depression. Despite a 9% revenue increase in 2025, the company faced a substantial operating loss of $62.3 million and a net loss of $38.6 million, driven largely by acquisition-related and commercialization costs. Reliance on third-party manufacturers and collaborators like Biogen presents supply chain risks. Looking ahead, contingent milestone payments related to the Sage deal and pending regulatory approvals add financial uncertainty amid expected 17-21% top-line growth in 2026.

Growth Momentum Reflected by Diversified CNS Product Portfolio

Supernus Pharmaceuticals focuses on central nervous system disorders with commercial therapies covering ADHD, Parkinson's Disease dyskinesia and hypomobility syndromes, epilepsy, migraine, cervical dystonia, chronic sialorrhea, and postpartum depression via ZURZUVAE—acquired from Sage Therapeutics in mid-2025—and ONAPGO for PD hypomobility [S1][S2]. The company leverages strategic collaborators such as Biogen for U.S. commercialization of ZURZUVAE under a profit-sharing arrangement [S1][S17]. Manufacturing relies on third-party contract manufacturing organizations (CMOs), underscoring operational dependencies within its diversified portfolio [S1].

FY2025 Financial Performance: Revenue Growth Amid Profitability Challenges

Supernus reported fiscal year 2025 revenues increased approximately 9% year-over-year. While the exact figure for FY25 revenue is not directly available from [F1], the prior years showed fluctuations with $100.4 million in revenue in FY2019; recent news indicates solid growth [N6]. However, the company incurred an operating loss of $62.3 million in FY25 compared with an operating income of $81.7 million the prior year—a decline of approximately 176% [F1]. Net income was negative $38.6 million versus positive $73.9 million in FY24 [F1]. These losses reflect acquisition-related charges tied to the Sage transaction along with elevated selling, general & administrative expenses associated with scaling commercialization efforts.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -39 | 47 | -62 | 1338000 | -152.2% |

| 2024 | 74 | 172 | 82 | 725000 | |

| 2022 | 61 | 117 | 46 | +13.6% | |

| 2021 | 53 | 127 | 86 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 46 | -3.6 |

| 2024 | 171 | 7.1 |

| 2022 | 6.9 | |

| 2021 | 6.5 |

Source: SEC companyfacts cache [F1].

This divergence between revenue growth and profitability highlights investment in R&D and integration costs post-acquisition [F1][N6].

Operational Dependencies and Partnership Risks

Supernus depends on third-party collaborators for development, manufacturing supplies, intellectual property rights licensing, and commercialization platforms [S1]. The partnership with Biogen involves equal sharing of profits and losses from ZURZUVAE sales in the U.S., which exposes Supernus to potential operating losses if sales underperform [S17]. Additionally, supply agreements like the Britannia Supply Agreement for APOKYN/ONAPGO products create single-source supplier risks that could disrupt manufacturing or require costly technology transfers if terminated [S1]. These dependencies emphasize vulnerabilities inherent in Supernus's business model.

Sage Acquisition: Pipeline Expansion with Contingent Milestone Payments

The July 2025 acquisition of Sage Therapeutics expanded Supernus’s CNS portfolio by adding FDA-approved oral zuranolone (ZURZUVAE) for postpartum depression [S1][N6]. The deal includes contingent milestone payments totaling up to $234 million tied to achieving specific U.S. sales thresholds through calendar years ending in 2030 and a milestone related to first commercial sale in Japan upon regulatory approval before June 30, 2026 [S1]. These contingent payments represent future cash obligations dependent on successful market penetration amidst competitive pressures.

Liquidity Position and Capital Allocation

As of December 31, 2025, Supernus held approximately $128 million in cash and equivalents with current assets exceeding current liabilities by nearly double—a current ratio of about 1.9—indicating solid short-term liquidity [F1][S4]. Operating cash flow remained positive at roughly $47 million despite net losses, supporting ongoing operations [F1]. Capital expenditures were modest at about $1.3 million focused likely on maintenance rather than expansion [F1]. Free cash flow after capex was positive at approximately $46 million.

The company has not declared dividends or engaged in share repurchases recently, signaling a focus on reinvesting cash into pipeline development and integration activities resulting from recent acquisitions rather than returning capital to shareholders [F1][S4]. Credit facilities remain available but unused at year-end [S4][S6].

Forward Outlook: Guidance Highlights Growth with Profitability Risks

Management guidance for fiscal year 2026 projects total revenue growth between approximately +17% to +21%, driven primarily by continued uptake of ZURZUVAE alongside existing product lines expanding geographically or into new indications [N6][S3]. Key milestones include achieving sales targets triggering contingent payments linked to the Sage acquisition and securing Japanese regulatory approval for zuranolone to unlock additional milestone payments [S1].

However, uncertainties remain due to evolving U.S. healthcare reforms targeting drug prices that may pressure margins across product lines as well as ongoing legal proceedings related to the Sage acquisition that pose operational risks [S10][S14][S5].

Investment Returns: Negative ROE Reflecting Growth-Stage Investments

For fiscal year 2025, Supernus posted an approximate return on equity (ROE) of -3.6%, derived from net losses relative to equity totaling about $1.06 billion at year-end [F1]. This negative ROE reflects elevated operating costs outpacing earnings despite top-line gains—a common profile among biopharmaceutical companies investing heavily in pipeline advancement.

Capital allocation priorities currently favor reinvestment over shareholder distributions given ongoing integration efforts and heightened operating expenses associated with recent strategic transactions [F1].

Regulatory Environment and Legal Considerations

Supernus operates amid complex regulatory dynamics including U.S. healthcare reforms aimed at lowering pharmaceutical prices which may impact reimbursement levels across products [S10][S11]. Additionally, ongoing federal securities litigation originating before the Sage acquisition introduces legal uncertainties that could divert management attention or incur costs [S14][S5]. Patent litigation defending proprietary technologies also remains an active risk requiring vigilance [S20].

This analysis integrates publicly available data emphasizing historical financial performance alongside operational fundamentals shaping Supernus Pharmaceuticals’ trajectory following recent strategic acquisitions within the evolving CNS market landscape without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments