General Fusion Group: Post-Combination Trajectory from SPAC to Fusion Energy Pioneer

Spring Valley Acquisition Corp. III’s transformation into General Fusion Group marks a pivotal shift from a shell acquisition vehicle to an operating fusion energy company facing technical and commercial inflection points.

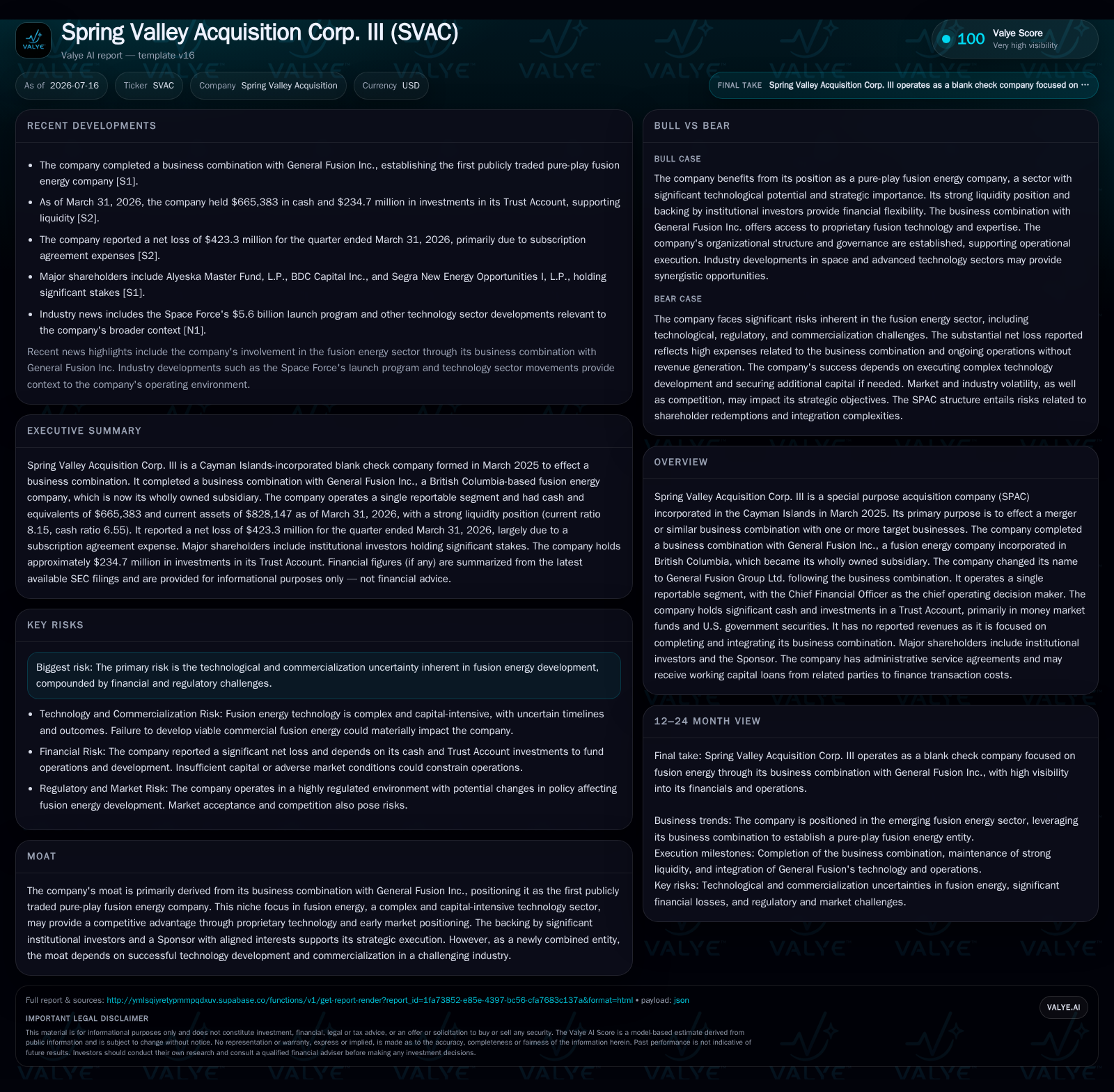

Spring Valley Acquisition Corp. III completed its business combination with General Fusion Inc., transitioning from a SPAC shell into General Fusion Group Ltd., the first publicly traded pure-play fusion energy company [S1][S2][S3]. The latest quarterly filing reveals a strong trust account cash position post-IPO yet signals potential liquidity needs as the company advances its capital-intensive fusion technology development [S2]. Sponsor involvement remains a critical enabler of capital and governance, while investor redemption rates and PIPE participation will influence funding stability [S2][S3]. Risks remain elevated due to fusion technology commercialization uncertainty and capital market volatility [S1]. Watchpoints include lock-up expirations, additional capital raises, and milestones linked to technology validation and initial revenue generation [S1][S2][S3].

Latest Quarterly Filing Signals Financial Positioning Ahead of Fusion Commercialization Milestones

Spring Valley Acquisition Corp. III’s May 15, 2026 10-Q filing reveals that following its September 2025 Initial Public Offering (IPO), approximately $230 million was secured in a dedicated Trust Account. These funds are conservatively invested in short-duration U.S. government treasury bills and money market funds, providing a secure capital base to support near-term fusion technology development activities [S2]. As of March 31, 2026, the company reported no outstanding working capital loans, reflecting a clean balance sheet post-repayment of prior related-party borrowings, including a $151,636 unsecured promissory note from its Sponsor that was fully repaid at IPO closing [S2].

However, the filing also highlights going concern considerations under ASC 205-40, indicating that additional capital—potentially through loans or equity investments from Sponsors, shareholders, or third parties—may be necessary to sustain ongoing research and development (R&D) efforts. This underscores the capital-intensive nature of fusion energy commercialization and the importance of prudent liquidity management [S2]

Fair value measurements for certain assets are classified as Level 3 inputs, reflecting the inherent valuation challenges of early-stage fusion technology where observable market comparables are scarce or nonexistent [S2]. Additionally, the presence of warrants convertible at the lender’s discretion (up to $1.5 million) introduces potential dilution typical of SPAC sponsor financing structures

Transition from SPAC Shell to Pure-Play Fusion Energy Company

The de-SPAC transaction with General Fusion Inc. culminated in a legal continuation from the Cayman Islands to British Columbia, Canada, with the entity rebranded as General Fusion Group Ltd. This jurisdictional and structural shift marks a critical transformation from a non-operating blank check vehicle into an operational public company focused exclusively on fusion energy technology development [S1][S3].

Post-merger, General Fusion Group consolidated its reporting into a single operating segment comprising General Fusion Inc., its wholly owned subsidiary dedicated to magnetized target fusion (MTF) research and prototype development. The company currently generates no revenues, reflecting its early-stage R&D lifecycle and emphasizing milestone-driven value creation rather than traditional revenue or EBITDA metrics [S1][S3]

This pure-play positioning differentiates General Fusion Group from typical SPACs with diversified or undefined targets, placing it at the forefront of public market exposure to fusion energy innovation. The company’s progress will be measured by technical validation milestones, patent development, and regulatory approvals rather than conventional commercial KPIs.

Sponsor Role and Capital Structure Dynamics

Sponsor involvement remains a cornerstone of General Fusion Group’s capital strategy. Prior to IPO completion, the Sponsor provided an unsecured, non-interest-bearing promissory note facility of up to $250,000, fully repaid at IPO close, demonstrating aligned financial support during critical transaction phases [S2].

Post-business combination, the Sponsor holds founder shares and private placement warrants, aligning incentives for long-term value creation but also introducing dilution risks common in SPAC structures. The Sponsor’s equity stake and warrant holdings influence governance and capital allocation decisions, balancing the need for ongoing funding with shareholder dilution considerations.

PIPE (Private Investment in Public Equity) financing concurrent with the IPO further supplemented capital resources, signaling institutional investor confidence despite the speculative nature of fusion technology development [S1][S3]. The interplay between Sponsor equity, PIPE participation, and public shareholder redemption rates will critically determine the net capital available for advancing fusion R&D.

Trust Account Liquidity and Redemption Rights Impact on Funding Stability

The Trust Account, holding IPO proceeds and PIPE funds, acts as a financial safeguard ensuring merger consideration availability but also imposes liquidity constraints until redemption rights and business combination conditions are settled [S2][S3]

Public shareholders’ redemption rights exercised post-merger materially affect the net funds retained, directly influencing General Fusion Group’s operational runway. Elevated redemption rates can reduce available capital, potentially necessitating additional PIPE rounds or Sponsor-led capital raises to bridge funding gaps. Conversely, low redemption activity reflects investor confidence and enhances financial stability.

PIPE financing participation rates serve as a proxy for institutional appetite toward the company’s fusion technology risk profile, with committed capital extending the runway for multi-year R&D cycles essential to achieving commercial viability.

Commercialization Challenges in a High-Tech Fusion Sector

General Fusion operates within a uniquely challenging technological domain. The magnetized target fusion approach requires sustained R&D investment to overcome scientific, engineering, and regulatory hurdles. These include validating plasma confinement and compression techniques, scaling prototype reactors, and navigating environmental and safety regulations in both Canadian and U.S. jurisdictions [S1].

The company’s risk disclosures emphasize uncertainties around timely achievement of technical milestones and budget adherence, reflecting the inherent volatility of pioneering fusion energy development. Unlike typical SPAC targets with established revenue streams or near-term profitability, General Fusion’s valuation depends heavily on successful demonstration of fusion technology feasibility and scalability.

This long development horizon and capital intensity differentiate General Fusion from other SPAC-acquired entities, positioning it as a high-risk, high-reward investment within the clean energy innovation ecosystem.

Investor Sentiment and PIPE Participation as Confidence Indicators

Institutional investor participation in PIPE financing concurrent with the IPO suggests a measured optimism regarding General Fusion’s proprietary MTF technology. This contrasts with traditional private equity clean-tech investments, which often involve longer incubation periods before public market entry [S1][S3].

The PIPE size relative to trust funds and Sponsor equity injections provides a tangible measure of investor conviction, enabling the company to extend its operational runway through critical validation stages. This capital structure supports the multi-year timeline necessary for prototype development, regulatory engagement, and eventual commercial deployment.

Growth Drivers Centered on Technological Validation Milestones

With no current revenue generation, General Fusion’s growth prospects hinge on achieving key R&D milestones that validate its fusion technology platform. These include successful prototype testing, patent filings, and regulatory approvals for experimental reactor deployment.

Such milestones serve as critical inflection points for value realization, substituting for traditional SaaS or industrial KPIs like ARR or EBITDA margins. Progress in these areas will influence investor sentiment, warrant exercise rates, and potential future capital raises.

Key Watchpoints: Lock-Up Expirations, Dilution, and Capital Raises

Upcoming lock-up period expirations for Sponsor founder shares and private placement warrants will be pivotal events, potentially increasing share liquidity and trading volumes [S2][S3]. These expirations may also introduce dilution pressures if warrants are exercised, impacting share count and market capitalization

Management’s assessment of going concern risks highlights the possibility of additional capital raises through equity or debt instruments. Announcements regarding such funding rounds, especially those involving Sponsor or strategic partners, will be critical indicators of the company’s financial sustainability.

Operational milestones, such as completion of major prototype phases or securing initial revenue-generating contracts—likely from government or research institutions—will serve as tangible validation points for the company’s fusion technology investment thesis.

Disclaimer: This article is for informational purposes only. It does not constitute investment advice or an offer to buy/sell securities. Readers should conduct their own due diligence when evaluating any financial instrument or investment opportunity discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments