FingerMotion’s Platform Diversification Struggles Amid Liquidity Constraints and Regulatory Risks

The company’s core telecom transaction services see sharp volume dips, while emerging platform segments remain nascent and capital-dependent.

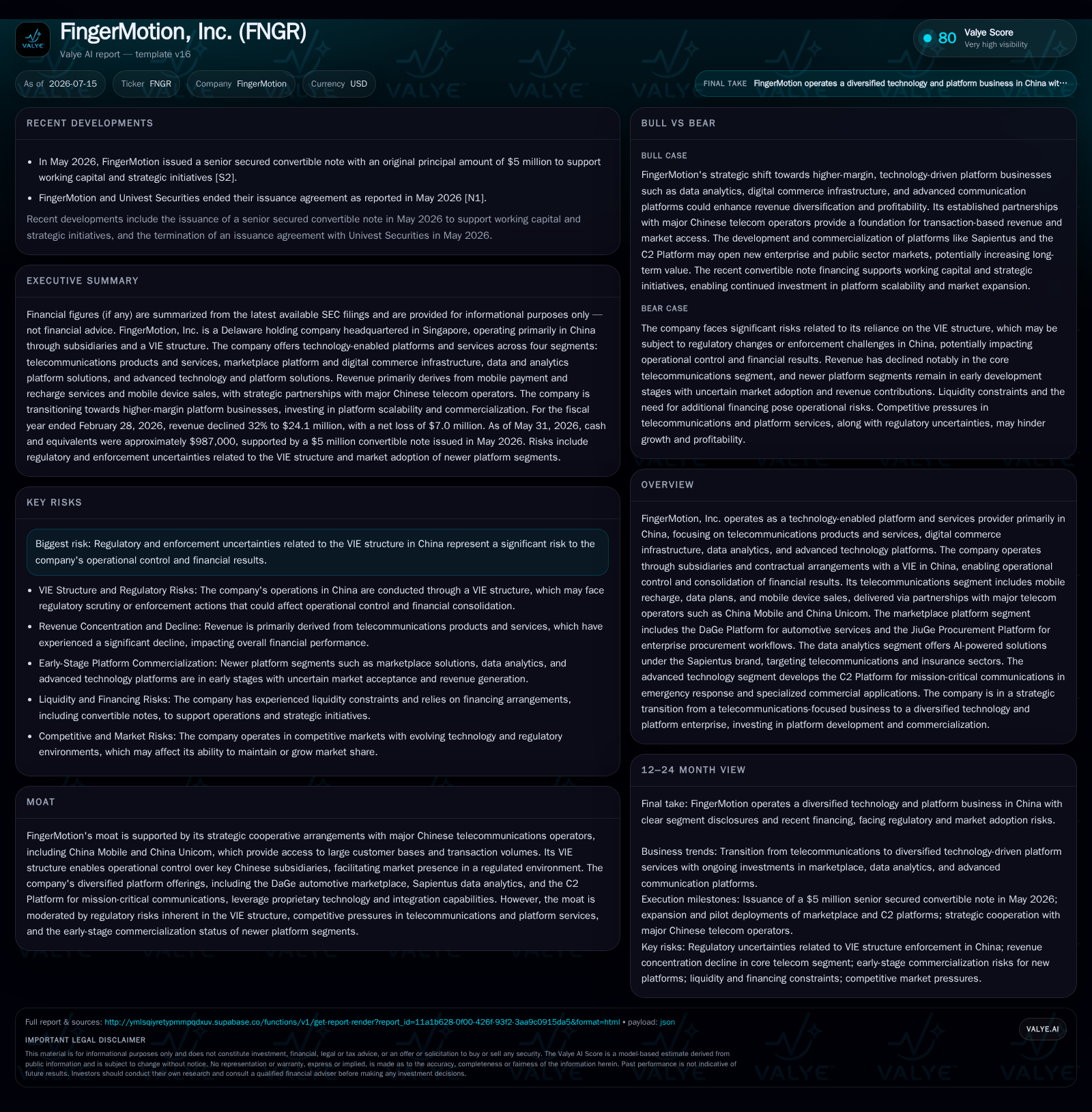

FingerMotion, Inc. reported a precipitous 92% revenue decline in Q3 2026 driven by lower transaction volumes in its telecommunications segment, reflecting ongoing liquidity constraints that have limited operational funding. While management pursues diversification through AI-powered data analytics, marketplace platforms, and advanced technology solutions, these newer areas are still early-stage with limited revenue contribution. The company's business model remains deeply intertwined with strategic partnerships with China Mobile and China Unicom via its VIE structure, a setup fraught with ongoing regulatory uncertainties. Recent financing activities provide temporary working capital relief but underline the dependency on external capital to sustain and grow operations.

Recent Operating Update: Sharp Revenue Decline Reflects Funding Challenges

Despite this downturn in volume-driven revenue, operating expenses remained essentially flat at approximately $2.14 million QoQ [S7], indicating stable cost management but also highlighting constrained flexibility for new growth initiatives or marketing spend enhancement. Consequently, FingerMotion's net loss remained broadly unchanged at around $2 million for the quarter ending May 31, 2026 compared with the same period last year [S7].

Liquidity saw an improvement following a strategic $5 million senior secured convertible note issuance earlier in May 2026 [S8], bolstering cash balances to nearly $987K as of quarter-end from just $68K at February’s end [F1][S7]. While this influx of capital offers short-term runway extension, the company’s business model continues to require effective working capital deployment for transaction processing volumes—a critical lever of revenue generation in mobile payment services.

Business Model: Transaction-Driven Telecom Services Paired With Emerging Platform Initiatives

As presented in the most recent annual report and quarterly disclosures, FingerMotion operates predominantly as a technology-enabled platform company providing digital telecommunications products and services primarily within mainland China through contractual control over its variable interest entity (VIE), JiuGe Technology [S1][S17]. This structure facilitates operational control despite Chinese restrictions on foreign ownership in telecom sectors.

The company monetizes mainly via transaction-based fees derived from mobile recharge/top-up services for consumers engaging on platforms integrated with major carriers such as China Mobile and China Unicom [S1][S2]. These transactions include prepaid voice/data top-ups, device sales, subscription management services, and value-added offerings like device protection programs launched via cooperation with China Unicom’s regional branches [S2]. This dependency on operator partnerships is both a moat—securing access to large customer bases—and a vulnerability given shifting regulatory landscapes around VIEs.

In parallel, FingerMotion is developing higher-margin technology platform businesses encompassing four main verticals: marketplace platforms (DaGe automotive services and JiuGe procurement workflow tools), data analytics under the Sapientus brand focusing on telecommunication and insurance enterprises powered by AI algorithms, advanced real-time communication platforms labeled C2, and broader enterprise digital infrastructure solutions [S1][S15][S17]. These newer segments aim to diversify away from pure telecom transactions toward subscription services, advertising monetization opportunities, and value-added enterprise intelligence applications.

However, these platform businesses are currently at early commercialization stages with limited revenue visibility. For instance, the DaGe marketplace shows minimal transactional activity yet relies on scaling user adoption; Sapientus is gaining traction but remains nascent; Advanced Technology & Platform solutions contributed just over $135K in Q3 versus roughly $109K prior year quarter—project-based rather than recurring revenue streams so far [S14]. Revenue concentration remains firmly skewed towards traditional telecom products where declines have overshadowed incremental platform gains.

Industry Structure and Competitive Position

FingerMotion occupies a niche as an integrator between end consumers/businesses and infrastructure providers (telecom operators), leveraging platform ecosystems that enable digital commerce transactions alongside enterprise-grade data analytics solutions typical of the technology-enabled platforms and services industry segment.

Its strategic arrangements with dominant state-backed Chinese telecommunication carriers are critical for scale: partnerships with China Mobile—the largest national operator—and China Unicom facilitate access to extensive subscriber networks necessary for mobile recharge volume-based revenue models [S2][S15]. By comparison peers in telecom services or digital commerce platforms like Alibaba or JD.com operate more diversified marketplaces with stronger consumer brand presence; data analytics competitors such as Palantir feature highly mature AI-driven products targeting broad industries beyond telecom-centric use cases.

While FingerMotion leverages proprietary technology stacks across multiple verticals—including SMS/MMS communication services via acquisitions like Beijing XunLian TianXia Technology Co.—its competitive differentiation is moderated by its dependence on secure VIE contractual arrangements subject to regulatory uncertainty [S2][S1]. Additionally, the early-stage nature of platform diversification limits bargaining power vis-à-vis larger ecosystem incumbents.

Growth Drivers: Platform Expansion Faces Early-Stage Hurdles Against Working Capital Constraints

Key growth vectors cited by management include increasing smartphone penetration driving mobile recharge transactions; expansion into O2O marketplaces exemplified by DaGe’s automotive service connection ambition; rising enterprise demand for AI-powered data analytics leveraged through Sapientus; and new real-time enterprise communications platforms under development like C2 aimed at mission-critical coordination scenarios across industries [S10][S15]. Regional ambitions extend beyond mainland China targeting selected Southeast Asian markets such as Indonesia and Thailand for these newer offerings [S10].

Yet scaling these platform initiatives intrinsically depends on successful user acquisition—active platform users—and recurring subscription renewals combined with expanding transaction volume processed metrics fundamental to improving ARPU (average revenue per user) over time [S8][S14]. Presently, liquidity limitations restrict operational capacity to fund transactions at meaningful scale in core telecom operations which cascades negatively onto marketing investments essential for accelerating adoption curves across newer platforms.

Strategic acquisition discussions signal intent to fill technology capability gaps or expand market reach; however execution risk remains elevated given resource constraints noted in financials.

Risks & Watchpoints: Regulatory Uncertainty and Capital Dependency Are Overarching Concerns

Foremost risk centers on the legality and stability of FingerMotion’s VIE framework amidst enhanced Chinese regulatory scrutiny protecting critical telecom infrastructures from foreign control risks inherent in VIE setups [S1][S2]. Any adverse enforcement actions could jeopardize contractual control over primary operating subsidiaries leading to significant operational disruption or loss of consolidation rights.

Financially, persistent net losses exceeding $7 million annually illustrate ongoing challenges achieving profitability while sustaining requisite working capital buffers critical for transaction-based business models dependent on frequent fund deposits with carrier partners [F1][S9]. The company faces Nasdaq delisting risk due to stock price below $1 compliance threshold received in mid-2026 prompting urgency around restoring investor confidence either via operational turnarounds or financial restructuring measures [S3].

Execution risks related to commercializing emergent platform segments through competing against entrenched digital commerce or data analytics incumbents remain acute given FingerMotion’s smaller scale and uncertain go-to-market traction. Monitoring KPIs including transaction volumes processed on core telecom platforms alongside early indicators of active user growth or subscription renewals for marketplace/Sapientus solutions will be critical demand markers.

What To Watch Next

Key milestones include updates on commercial traction for DaGe platform adoption rates, progress reports on Sapientus AI analytics client wins particularly among insurance customers, deployment success cases for C2 communication platform especially within emergency service agencies spotlighted previously via local government contracts [S14].

Financially, quarterly revenue rebounds tied to incremental recovery or expansion of telecom transaction volumes supported by improved working capital cycles would indicate easing constraint pressures. Management’s additional financing efforts post-May 2026 convertible note placement will also bear watching given dependence on external funding sources for sustaining operations beyond near-term horizons.

Also relevant are any developments regarding compliance status progression following Nasdaq deficiency notifications; resolution of VIE legal risk factors; announcements surrounding international regional expansion plans execution; and strategic acquisition activity enhancing technology or market footprint.

Financial Profile Discussion

As of 2026-05-31, companyfacts shows $987,391 in cash and equivalents, current assets of approximately $53 million, and current liabilities near $49 million implying a current ratio of about 1.09x [F1]. Capital allocation priorities emphasize balancing funding core telecom product/service operations against selective investments into growing platform initiatives plus measured regional expansion endeavors aiming for long-term value creation despite near-term margin pressures.

Disclaimer: This analysis is based solely on publicly available SEC filings dated up to July 15, 2026. It does not constitute investment advice but provides an independent assessment grounded strictly on disclosed company facts combined with sector-level understanding applicable within technology-enabled platform industries.

Financial position in context

As of 2026-05-31, companyfacts shows $987,391 in cash and equivalents [F1]. Current assets of $53mm and current liabilities of $49mm imply a current ratio near 1.09x for 2026-05-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments