Plutonian Acquisition Corp. II Advances SPAC Milestones with Robust Trust Account Reserve

July 2026 quarter confirms Plutonian’s strong capital foundation and sponsor backing, key for its SPAC trajectory toward a business combination.

Plutonian Acquisition Corp. II reported in its July 15, 2026, 10-Q filing that it secured over $108 million from its IPO, over-allotment, and sponsor private placement, all held in a trust account as mandated by SPAC regulatory requirements. This liquidity position underpins the company's operational runway and ability to pursue a de-SPAC transaction within the prescribed timeframe. Sponsor economics via private placements align incentives but introduce typical dilution considerations. With no operating business disclosed, Plutonian’s value creation depends on successful deal execution amid competitive SPAC market dynamics.

Plutonian Acquisition Corp. II Advances SPAC Milestones with Robust Trust Account Reserve

Plutonian Acquisition Corp. II’s July 15, 2026, 10-Q filing confirms the successful capitalization of its trust account with net proceeds totaling approximately $108 million from its initial public offering (IPO), over-allotment option units, and sponsor private placements [S3]. This trust account, held by Continental Stock Transfer & Trust as trustee, is a regulatory-mandated escrow designed to safeguard investor capital exclusively for use in an initial business combination or for redemption purposes, underscoring Plutonian’s compliance with SPAC operational norms and its readiness to pursue a de-SPAC transaction within the prescribed timeframe.

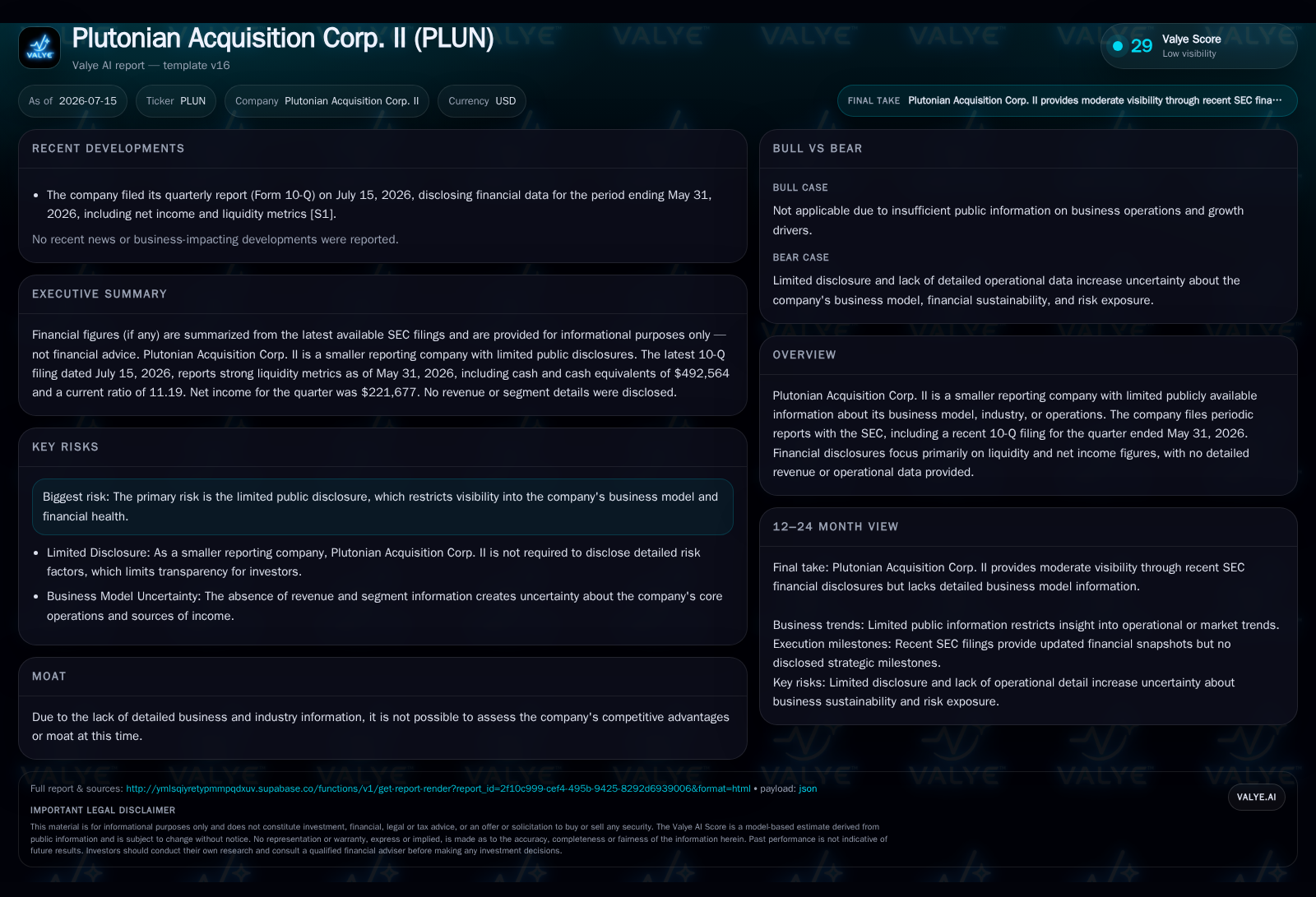

As of May 31, 2026, Plutonian reported cash and cash equivalents of approximately $492,564 outside the trust account, with no outstanding debt, reflecting a clean balance sheet typical of pre-combination SPACs [F1], [S2]. This cash primarily supports administrative and overhead expenses, including legal, underwriting, and compliance costs, ensuring operational continuity without encroaching on trust funds reserved for acquisition financing. The company’s current ratio of 11.19 further indicates strong short-term liquidity relative to minimal liabilities [F1].

SPAC Business Model and Capital Structure: Sponsor Promote, Units, and Redemption Rights

Plutonian’s capital structure follows the standard SPAC archetype, issuing units each composed of one Class A ordinary share and one right, with each right entitling holders to receive one-fourth of an additional Class A share upon consummation of a business combination [S3]. This structure enhances post-merger equity participation but introduces complexity in share count and potential dilution.

The sponsor’s role is pivotal in this model. Concurrent with the IPO closing on April 29, 2026, Plutonian completed a private placement of 7,800 units to its sponsor at $10 per unit, generating $78,000 in gross proceeds [S3]. These sponsor units represent the “promote,” a common incentive mechanism granting sponsors equity stakes at nominal cost to reward successful deal execution. While this aligns sponsor and public shareholder interests, it also introduces dilution risks post-merger, especially when combined with warrants and rights embedded in the units.

Redemption rights afford public shareholders the option to redeem their shares for cash from the trust account if dissatisfied with proposed acquisition terms [S3]. Redemption activity directly impacts the capital available for acquisition and can necessitate supplementary financing through PIPE (Private Investment in Public Equity) deals or additional sponsor contributions. This dynamic creates a delicate balance between sponsor incentives and shareholder protections, a challenge shared by peers such as Churchill Capital Corp series and Social Capital Hedosophia, which have navigated similar dilution and redemption trade-offs

Operational Status and Financial Metrics Reflect Typical Pre-Combination Activity

Plutonian currently operates as a capital vehicle without disclosed operating revenues or commercial activities [S2]. Its net income of approximately $221,677 as of May 31, 2026, primarily reflects nominal administrative income or expense recognition rather than substantive business operations [F1]. Operating expenses remain limited to costs associated with IPO processes, regulatory compliance, and corporate governance.

This financial profile aligns with the SPAC industry norm, where value creation hinges on identifying and executing a business combination rather than pre-combination revenue growth. Key operating KPIs for Plutonian will thus focus on deal pipeline development, time remaining to complete a business combination, and shareholder redemption rates rather than traditional revenue or margin metrics.

Competitive and Market Context: Navigating SPAC Lifecycle Pressures

Plutonian operates within a competitive SPAC environment characterized by numerous capital vehicles vying to identify attractive private companies seeking public market access. The company’s ability to consummate a business combination before statutory deadlines is critical, as failure to do so typically results in liquidation and return of trust funds to investors.

Sponsor economics, including promote structures and private placements, influence deal incentives but also heighten dilution risks. Redemption rights, while protecting shareholders, can reduce acquisition capital, necessitating PIPE financing or sponsor bridging to fill funding gaps. High-profile SPACs such as Pershing Square Tontine Holdings have illustrated these dynamics, where sponsor incentives and redemption activity materially impact post-merger equity valuation and shareholder returns.

Growth Drivers and Industry Tailwinds

Although Plutonian has not disclosed specific target sectors or acquisition candidates [S2], it stands to benefit from sustained demand among private companies for alternative public listing routes that offer faster timelines and potentially reduced regulatory burdens compared to traditional IPOs. Favorable capital market conditions and a regulatory environment supportive of SPAC transactions provide tailwinds for deal execution.

Growth prospects depend on Plutonian’s ability to identify acquisition targets aligned with investor appetite for emerging technologies or high-growth sectors often underserved by conventional IPO pipelines. The company’s sponsor expertise and capital base position it to compete effectively in sourcing and closing such transactions.

Regulatory Compliance and Governance

Plutonian maintains current SEC registrations and timely filings, with no material disclosures indicating regulatory or governance impediments to its de-SPAC timeline [S2]. The company’s adherence to SPAC-specific regulatory requirements, including trust account maintenance and disclosure obligations, supports operational cadence and investor confidence.

Financial Summary and Liquidity Position

As of May 31, 2026, Plutonian reported cash and cash equivalents of $492,564 outside the trust account, zero total debt, and current assets of $520,564 against current liabilities of $46,511, yielding a current ratio of approximately 11.19 [F1]. The net debt position is effectively negative $492,564, reflecting a strong liquidity buffer to cover administrative expenses.

The trust account balance, representing approximately $108 million in net proceeds from the IPO, over-allotment, and sponsor private placements, remains segregated and unavailable for general corporate use, preserving capital for the intended business combination or shareholder redemptions [S3]. This segregation is fundamental to SPAC investor protections and regulatory compliance.

Key Milestones and What to Watch

Critical upcoming milestones for Plutonian include identifying and announcing an acquisition target before the statutory deadline, securing shareholder approval for the business combination, and managing redemption levels to ensure sufficient acquisition capital. The company’s ability to attract PIPE investors or negotiate sponsor bridging financings will also be pivotal in mitigating dilution and funding risks.

Investors and market participants should monitor public disclosures for merger announcements, redemption statistics, and PIPE commitments to assess Plutonian’s progress and execution risk. Sponsor negotiations and deal structuring will significantly influence post-merger equity valuation and shareholder outcomes.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. All data is sourced from SEC filings [S2], [S3], and companyfacts [F1]. Readers should consult primary sources for verification.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments