Caro Holdings’ AI Platform Development Hindered by Severe Liquidity and Mixed Asset Strategy

Recent filings reveal Caro Holdings grappling with financial strain while pivoting into mineral assets, complicating its core AI software growth trajectory.

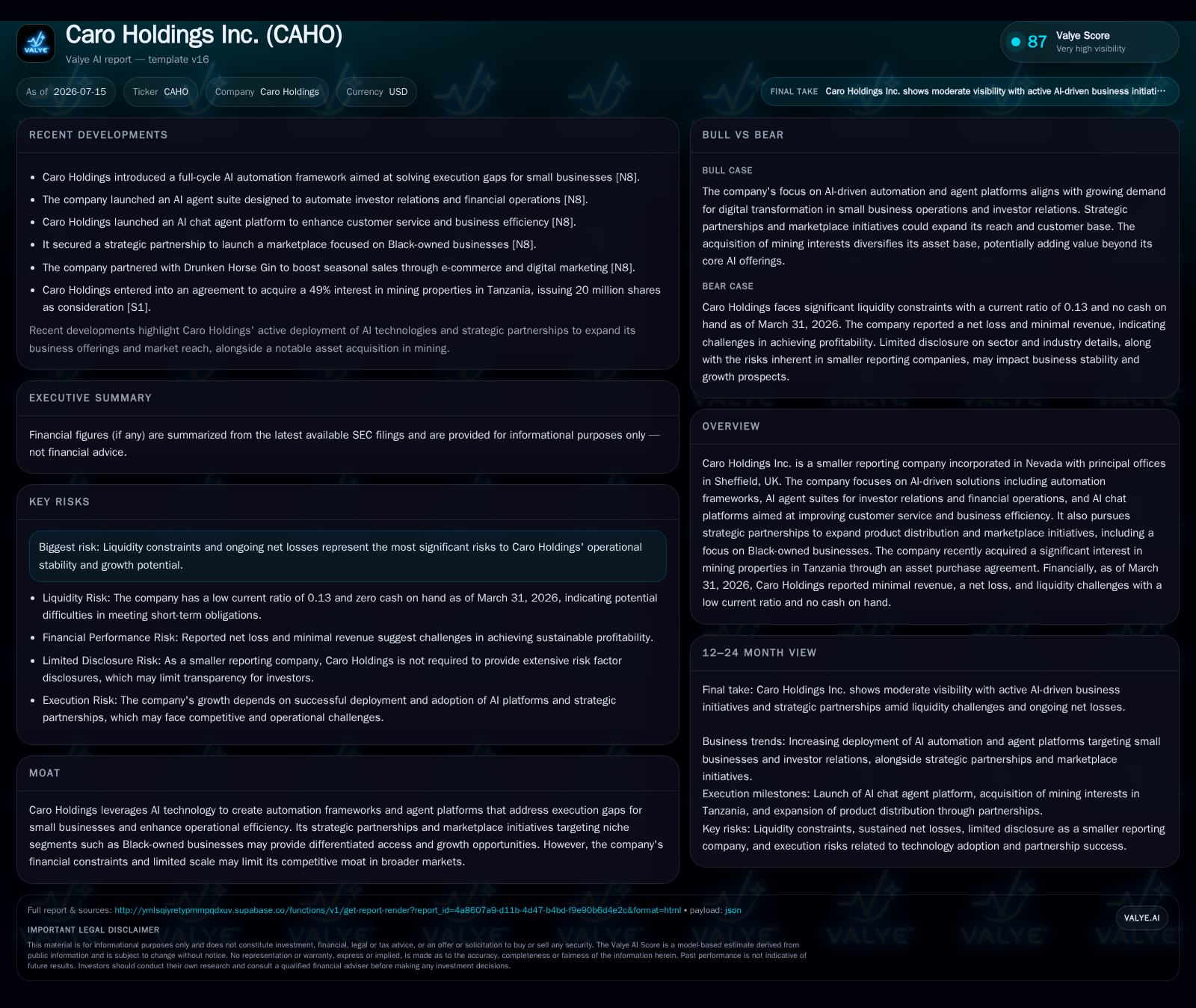

Caro Holdings Inc., primarily an AI-driven software developer focused on automation frameworks and investor relations technology, faces significant liquidity challenges as evidenced by a current ratio of 0.13 and net losses reported for fiscal 2026. A recent acquisition of a 49% stake in Tanzanian mining properties introduces a non-core asset dimension that distracts from its core software strategy. The company relies on strategic partnerships targeting niche markets such as Black-owned businesses to drive adoption and recurring revenue but remains in early stages with minimal revenue generation. These operational and financial headwinds raise concern about the sustainability of growth absent capital infusion or strategic refocusing.

Reported revenue is nominal at approximately $11,254 through year-end March ’26 while net losses deepen to about $407,797 for the same period [F1][S2]. The company's liquidity profile is particularly concerning: current assets stand around $262,757 versus current liabilities exceeding $1.9 million—yielding a critically low current ratio near 0.13 [F1]. Such imbalance signals severe short-term funding constraints that could impair day-to-day operational execution.

Compounding this liquidity pressure is Caro’s recent significant pivot into resource assets via an asset purchase agreement finalized in June 2026. The company agreed to acquire a 49% undivided interest in Tanzanian mining properties operated by Goldrange Resources Corp., paying via issuance of 20 million shares of common stock [S3]. While this move potentially opens alternative growth avenues outside core software offerings, it materially shifts the capital allocation focus amidst cash scarcity.

This juxtaposition—between growing financial strain in its primary AI business alongside aggressive entry into mining investments—establishes tension points likely influencing operational priorities and raising risks around resource distribution.

AI Automation Platforms and Strategic Partnerships: Cornerstones of Caro’s Software Business Model

Per the latest annual filing (10-K dated July 15, 2026), Caro Holdings positions itself as a creator of AI-driven automation frameworks and agent platforms designed primarily for investor relations and financial operations enhancement [S1]. Its product suite includes AI chat platforms facilitating improved customer engagement alongside modular automation tools intended to increase operational efficiency for small business users.

Revenue generation assumptions appear rooted in traditional technology sales archetypes: namely software licensing fees combined with subscription-based software as a service (SaaS) models. This setup predicates stable recurring revenue streams aligned with expanding monthly active user bases and maintaining strong product adoption rates.

To extend market reach beyond standard channels, Caro pursues strategic partnerships intending to penetrate underrepresented niches—explicitly involving Black-owned businesses—and develops marketplace initiatives positioning it as both technology enabler and community advocate [S1]. This strategy could differentiate Caro from peers by fostering customer loyalty amid niche segmentation.

Nonetheless, given the nascent stage noted by very limited reported revenues and ongoing operating losses, monetization remains weak with substantial reliance on accelerating customer acquisition costs (CAC) towards efficient scaling and reducing churn.

Industry Context: Competing as a Smaller AI SaaS Player Facing Capital and Scale Challenges

Within the broad Technology Software and Services sector focusing on AI automation solutions, Caro resides among smaller-scale SaaS providers specializing in business process automation for niche verticals. Such companies often grapple with high upfront R&D expenditure ratios relative to early-stage revenues leading to negative operating income profiles until achieving scale beyond initial product adoption plateaus.

Strategic partnerships are crucial growth levers here—not only for placing products within accessible sales channels but also for overcoming cost barriers intrinsic to selling complex AI platforms to small businesses with limited budgets. Peers resemble smaller fintech SaaS startups emphasizing investor relations or customer engagement tech but benefit from deeper pockets or more established brand recognition.[^peercontext]

Competition from mature incumbents capable of investing heavily in technology refresh cycles presents another hurdle as rapid innovation can quickly render early-stage offerings obsolete unless continuous reinvestment offsets product obsolescence risk.

For Caro, confirmation of progress would materialize through upward trends in monthly recurring revenue (MRR), higher active user counts reflecting successful partnerships, reduced CAC due to efficient marketing funnels, stable churn reductions signaling better retention, and gradual margin improvements tied to scaling effects.

Balancing Dual Focus: Implications of Mineral Asset Investments on Software Growth Execution

The decision to acquire a substantial interest in mineral asset properties introduces an uncommon duality into Caro’s corporate strategy. This pivot from pure software development into a resource extraction domain is atypical for companies primarily classified under technology services.

Such diversification imposes integration challenges including possible dilution of management focus from critical software R&D efforts toward operational complexities inherent in mining projects—territories requiring distinct expertise and capital commitments that compete against pressing technology development demands [S3][F1].

Moreover, given constrained liquidity—with zero reported cash balance against major liabilities—the opportunity cost of allocating scarce capital toward asset acquisition versus reinvestment into core platform advancement becomes conspicuous.

Industry precedents caution that without deliberate structuring or dedicated teams segregating these lines of business clearly at governance levels, cross-domain distractions can slow innovation pace or divert vital funds needed for scaling the SaaS model effectively.

Growth Catalysts: Partnership Expansion and Niche Market Penetration via Marketplace Initiatives

Caro’s primary visible growth engine rests on its ability to nurture and expand partnerships that widen distribution pathways especially within digitally underserved communities such as Black-owned enterprises [S1]. Marketplace initiatives targeting these niches not only build goodwill but can translate into meaningful new users adopting automation frameworks or AI agent platforms that improve investor relations efficiency.

Such channel strategies encompass partner onboarding efficacy reflected through partnership count growth metrics alongside twin KPIs like MRR uplift originating from new subscriptions tied to partner-driven referrals. Additionally, product adoption rate improvement—measured by increased usage intensity or higher ARPU—would validate marketplace traction.

Given the early commercial footprint evidenced by minimal revenue thus far, success hinges on converting these initiatives into tangible subscription commitments while balancing related CAC expenditures.

Risks from Liquidity Constraints, Customer Adoption Uncertainty, and Technology Competition

The risk spectrum centers predominantly on persistent liquidity insufficiency intensifying cash burn pressure absent meaningful revenue influxes or external financings [F1][S2]

Customer adoption barriers remain significant with risks related to slow ramping subscription volumes or elevated churn undermining ARR stability; product-market fit uncertainties exacerbate these concerns given incremental investment hurdles vs entrenched competitors.[^growthrisk]

Additionally, regulatory developments around AI usage—covering data privacy safeguards or ethical standards—can impose compliance costs or restrict deployment flexibility affecting operational continuity within certain jurisdictions.[^regrisk]

Integration risk from non-core mining acquisitions adds another layer requiring careful management lest it distract leadership or sap resources needed for platform innovation amidst already intense competition from larger SaaS vendors boasting scale advantages.[^diversificationrisk]

"Forward Indicators": What Metrics and Milestones Will Signal Progress or Setbacks for Caro?

Investors should closely monitor several measurable indicators that will act as barometers for Caro’s trajectory:

- Consistent acceleration in monthly recurring revenue (MRR) indicating healthy subscription scaling;

- Growth in partnership count especially agreements funneling customers from targeted niche segments;

- Stabilizing or declining churn rates evidencing improved retention;

- Improvements in customer acquisition cost (CAC) reflecting marketing efficiency gains;

- Any public disclosures of client wins quantifying active user counts or notable platform engagements;

- Actions toward strengthening liquidity such as successful capital raises or debt restructuring initiatives reducing near-term solvency risk;

- Signs that management dedicates sufficient bandwidth to advancing core AI platform roadmaps rather than diversionary pursuits.

These markers will clarify whether Caro can sustain its dual ambitions without losing ground amid financial pressures.

Financial Profile Discussion: Cash Flow Realities and Capital Structure in Context

From a balance sheet perspective drawn from the latest available SEC data ending March 31, 2026 [F1], Caro Holdings holds no cash equivalents while carrying total debts approximating $28,900 against current liabilities nearing $2 million—a configuration resulting in an extremely strained current ratio around 0.13. This mismatch highlights alarming short-term liquidity risk potentially constraining working capital flexibility.

Operating results further compound concerns with an operating loss recorded over $280K contributing to a net loss tally close to $408K during the same reporting period [F1]. Limited top-line at just over $11K indicates that operating expenses vastly outpace revenues underscoring negative cash flow dynamics typical of early-stage software firms yet amplified here by strained financing conditions.

Absent immediate relief through equity injections or restructuring maneuvering enabled by strategic investors or partnership monetization exits, sustaining platform development initiatives at required R&D levels will be difficult. This financial profile contextualizes the challenges facing execution speed necessary to capitalize on emerging demand for AI-driven automation solutions targeting small businesses through curated marketplace channels.

Cautionary statement: This analysis incorporates public filings up to July 15, 2026. It is intended solely for informational purposes without expressing any investment research view.

[^peercontext]: Examples of comparable smaller AI SaaS firms include LivePerson and Nuance Communications which have broader scale advantages than Caro but operate similarly within conversational AI platforms. [^growthrisk]: Slow adoption risks stem from niche market penetration delays potentially aggravated by limited marketing budgets relative to incumbents. [^regrisk]: Regulatory scrutiny regarding ethics of algorithmic decision-making may impose constraints requiring costly compliance upgrades by vendors like Caro. [^diversificationrisk]: Corporate strategy literature warns against unrelated diversification causing management distraction harms especially when capital resources are limited.

Financial position in context

As of 2026-03-31, companyfacts shows $28,900 of total debt and net debt for Caro Holdings [F1]. Current assets of $262,757 and current liabilities of $1,986,308 imply a current ratio near 0.13x for the same date [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments