Conagra Brands Faces Margin Pressure and Strategic Challenges Despite Brand Strength

The company’s latest quarterly results reveal operational headwinds amid commodity cost inflation and customer concentration risks.

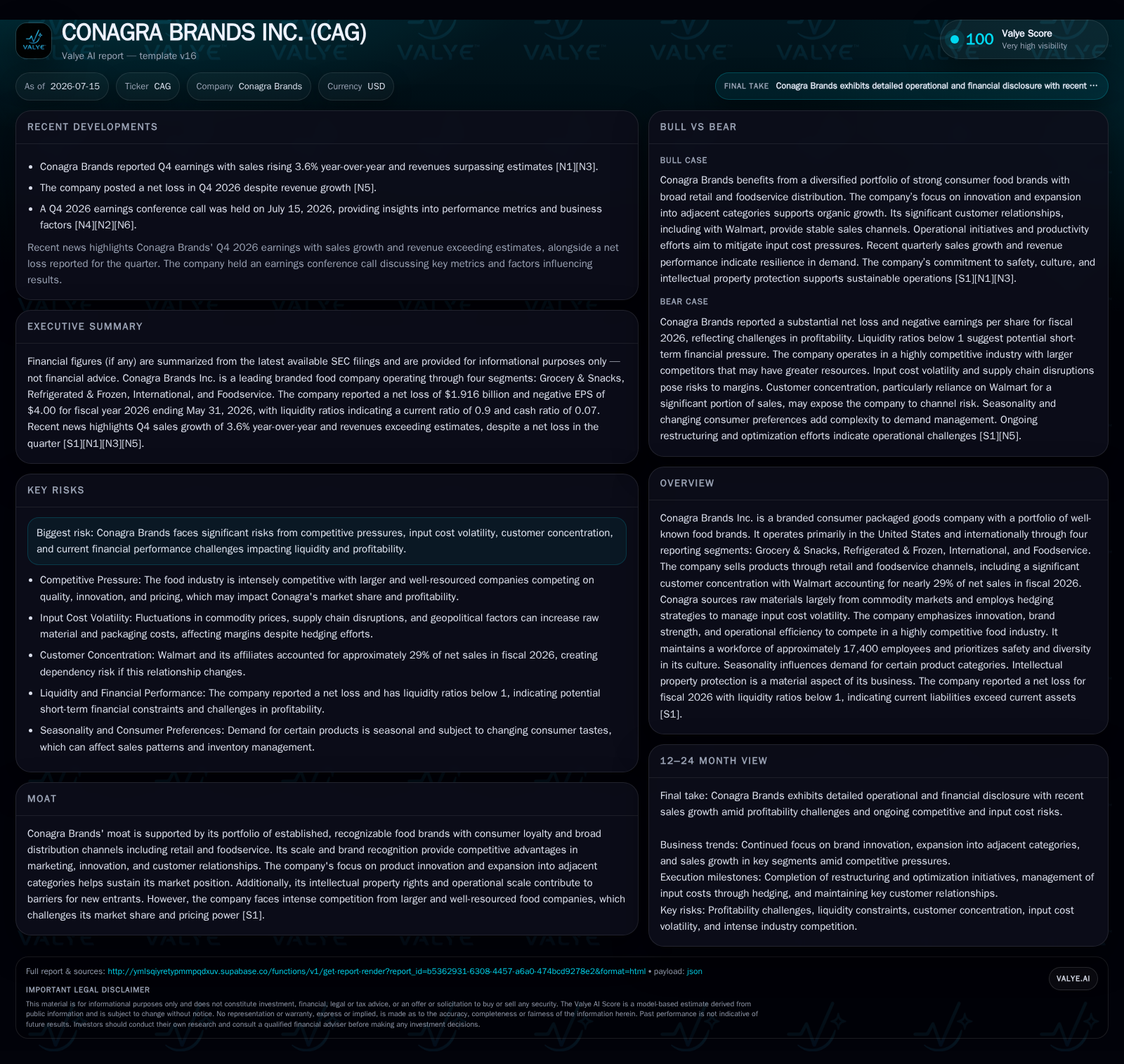

Conagra Brands Inc. reported fiscal 2026 results with revenue growth offset by significant operating losses, reflecting persistent margin pressures from commodity cost inflation and competitive market dynamics. The company’s branded packaged foods portfolio benefits from strong consumer recognition and retailer relationships, particularly with Walmart, but its heavy customer concentration and cost volatility pose ongoing challenges. Operational efficiency initiatives and product innovation remain crucial to sustaining competitiveness in a crowded sector where large peers also vie aggressively for market share. Financially, Conagra carries substantial net debt and a current ratio below 1, underscoring liquidity constraints that heighten execution risk.

Latest Operating Update

Conagra Brands Inc. reported fiscal 2026 results marked by revenue growth reaching approximately $15 billion, yet accompanied by a substantial operating loss of about $1.6 billion, reflecting ongoing margin pressures primarily driven by commodity raw material inflation and restructuring-related expenses [F1]. The company’s reliance on agricultural commodities such as grains and oils exposes it to significant cost volatility, despite employing hedging strategies aimed at mitigating some of this risk [S1]. These inflationary pressures have compressed gross margins, challenging profitability in a competitive branded consumer packaged goods environment.

Customer concentration remains a critical factor in Conagra’s operating dynamics, with Walmart accounting for nearly 29% of net sales [S1]. This concentration provides scale advantages in retail grocery channels but simultaneously introduces negotiation leverage risks, as Walmart’s pricing and assortment decisions can materially impact Conagra’s revenue visibility and margin profile. Maintaining strong brand equity and continuous product innovation is thus essential to securing shelf space and favorable terms within Walmart and other major retail partners.

Business Model Analysis

Conagra operates as a branded consumer packaged goods manufacturer with a diversified portfolio of value-added food products distributed primarily through retail grocery chains and foodservice operators across the U.S. and internationally. The company reports results across four segments: Grocery & Snacks; Refrigerated & Frozen; International; and Foodservice [S1]. Revenue generation is driven by wholesale sales volumes multiplied by negotiated prices with retailers and foodservice customers, where maintaining competitive pricing power is influenced by brand strength, category relevance, and retailer relationships.

The company’s broad brand portfolio spans multiple consumption occasions, from shelf-stable grocery items to perishable refrigerated offerings, enabling cross-category penetration. Distribution channels include traditional supermarkets, club stores such as Costco, mass merchandisers notably Walmart, smaller independent grocers, and institutional foodservice clients like restaurants and cafeterias. This multi-channel approach supports diversified revenue streams but also requires effective supply chain management and inventory turnover to balance seasonality and demand fluctuations [S1]

Margins are under structural pressure due to raw material cost inflation, with commodity prices for inputs such as grains, oils, and packaging materials being a significant cost driver. While Conagra employs hedging strategies to manage input price volatility, persistent macroeconomic inflationary trends have strained gross profits [S1]. Additionally, the company has incurred notable restructuring expenses related to workforce reductions, contract and lease terminations, and asset impairments as part of ongoing cost optimization efforts to align its cost base with evolving market conditions [S4].

Operational efficiency initiatives focus on streamlining manufacturing footprints and enhancing supply chain logistics to leverage scale economies. Product innovation remains a strategic priority, targeting consumer trends toward convenience and healthfulness, which are critical for sustaining category relevance and driving incremental sales in a crowded marketplace.

Industry Structure and Competitive Position

Conagra competes within a highly competitive consumer packaged food industry alongside large branded peers such as General Mills, Kraft Heinz, Kellogg Company, Nestlé, and Hormel Foods. These competitors vie on brand strength, marketing investment, product innovation cadence, pricing strategies, and shelf space access. While Conagra’s scale places it among the upper tier of U.S.-focused branded food manufacturers, it remains smaller than global giants like Nestlé, which benefit from broader geographic diversification and category breadth.

Distribution reach is a key battleground, with major retailer relationships dictating category shelf allocation and promotional support. The rise of private-label penetration by retailers intensifies competition, eroding branded players’ pricing power and compressing margins. Within this context, Conagra’s current negative operating margins highlight near-term execution challenges relative to peers who typically maintain positive operating margins through scale efficiency and pricing discipline.

Key operating metrics for benchmarking include gross margin percentages, operating margins, customer concentration ratios, and product innovation contribution to net sales [S1]. Conagra’s heavy reliance on Walmart (29% of net sales) is notable compared to peers, underscoring the importance of managing customer concentration risk

Growth Drivers

Conagra’s growth strategy centers on several vectors:

- Product Innovation: Developing and launching new SKUs aligned with consumer preferences for convenience, better-for-you ingredients, and premiumization supports incremental sales growth and helps maintain category relevance.

- Foodservice Expansion: Increasing penetration into institutional foodservice channels diversifies revenue streams and reduces dependence on retail grocery pressures.

- Geographic Expansion: Growth in the International segment aims to leverage U.S.-developed brands in adjacent markets with higher growth potential, addressing saturation in domestic categories.

- Brand Portfolio Diversification: Strategic acquisitions and targeted launches in adjacent food categories broaden market opportunities and reduce reliance on legacy products.

- Marketing Investment: Enhancing brand equity through focused advertising campaigns supports shelf prominence and consumer engagement amid intense competitor activity.

Tracking KPIs such as the percentage of sales from new product launches, renewal rates of key retail contracts, and distribution penetration in foodservice channels will be critical to assessing growth momentum.

Risks and Growth Constraints

Conagra faces several material risks that could constrain growth and profitability:

- Commodity Price Volatility: Raw material inflation can unpredictably erode gross margins despite hedging programs; sustained price spikes challenge the company’s ability to absorb or pass through costs without volume declines.

- Customer Concentration Exposure: Heavy reliance on Walmart means adverse renegotiations or assortment shifts could disproportionately impact revenues and margins.

- Competitive Market Pressures: Larger peers with greater marketing budgets and private-label competition limit pricing flexibility and market share gains.

- Execution Risk on Restructuring: Cost-reduction initiatives involve one-time charges that pressure earnings short-term; successful execution requires operational discipline without disrupting supply continuity.

- Regulatory Compliance Burden: Evolving food safety, labeling, and environmental regulations necessitate ongoing investment, particularly in international operations, adding complexity and cost.

- Seasonality Effects: Certain product categories experience seasonal demand fluctuations, requiring precise inventory and working capital management to avoid stockouts or excess inventory.

What To Watch Next

Key milestones to monitor include:

- Fiscal Q1 FY2027 results for indications of margin recovery following restructuring charges.

- Updates on new product launches reflecting pipeline vitality and alignment with health-conscious consumer trends.

- Outcomes of pricing negotiations with Walmart and other major retailers, which will reveal shifts in vendor leverage and pricing power.

- Commodity cost trends relative to hedging effectiveness impacting gross margin trajectory.

- Progress on operational efficiency metrics such as reductions in SG&A expenses and improvements in plant utilization.

- Changes in the International segment’s revenue mix as a gauge of geographic diversification success.

Financial Profile Discussion

Conagra’s fiscal 2026 financial profile reflects significant operating losses despite top-line growth, underscoring the impact of elevated commodity costs and restructuring expenses on profitability [F1]. The company’s net debt stands near $7 billion, with cash and equivalents of approximately $218 million, resulting in a current ratio of about 0.9x as of May 31, 2026, indicating tight liquidity conditions in a capital-intensive operating environment [F1]. This leverage profile heightens execution risk, emphasizing the importance of effective cost containment and stable revenue streams secured through diversified retail and foodservice contracts.

The company’s ability to improve operating margins through efficiency initiatives and product innovation will be critical to restoring financial health. Delays or setbacks in these areas could exacerbate liquidity pressures, especially given the competitive and inflationary challenges facing the branded packaged foods sector.

This analysis is based on publicly available SEC filings dated through July 15, 2026 [S1][S2][S3][F1] and incorporates relevant industry context common to branded consumer packaged goods companies. It does not constitute investment advice or research views.

Financial position in context

As of May 31, 2026, Conagra held $218 million in cash and equivalents against $7.23 billion in total debt, resulting in net debt of approximately $7.0 billion. Current assets totaled $2.88 billion versus current liabilities of $3.19 billion, yielding a current ratio near 0.9x, which reflects constrained short-term liquidity [F1]. This financial structure underscores the need for disciplined working capital management and operational improvements to support ongoing business investments and debt servicing.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments