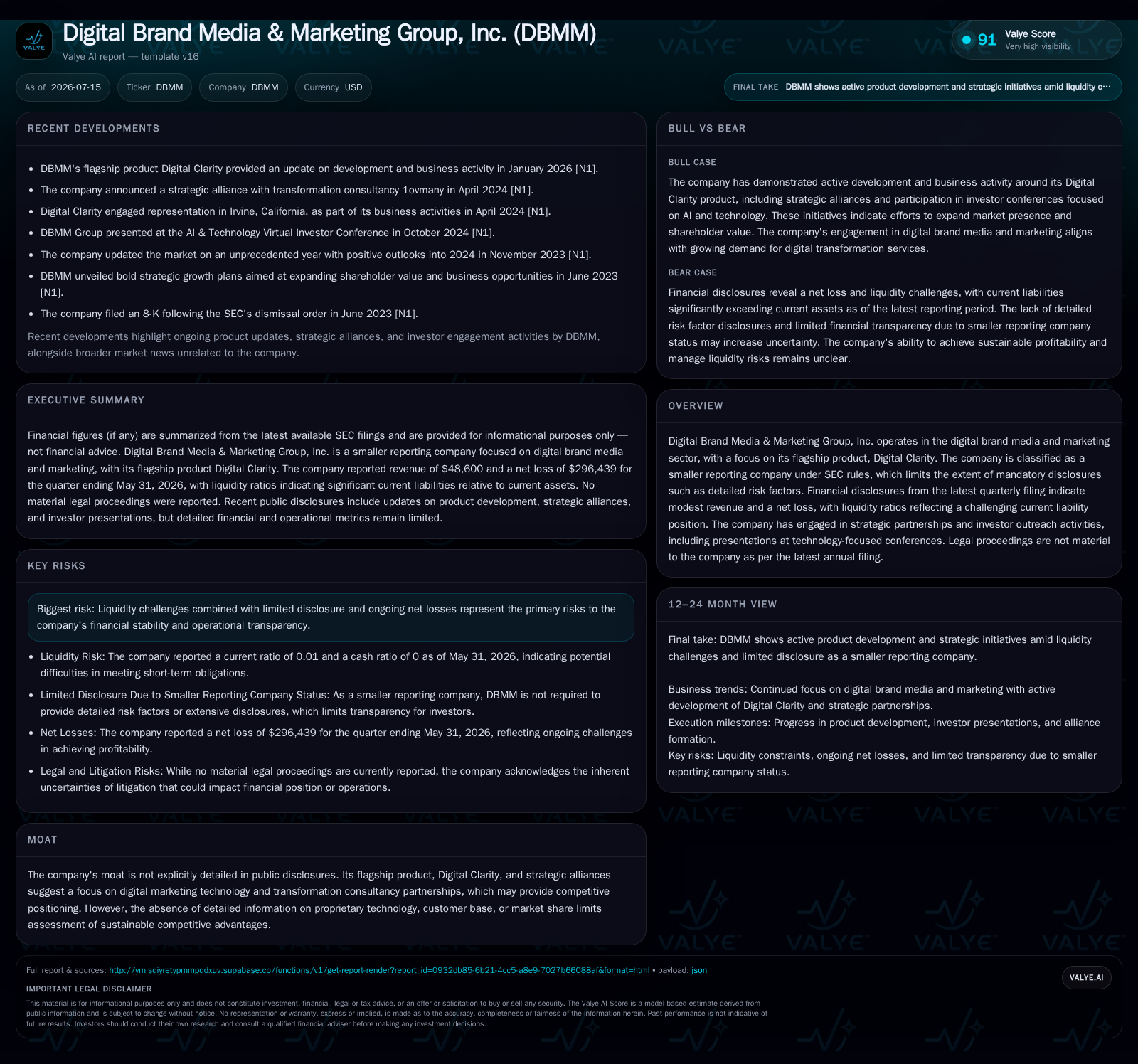

Digital Brand Media & Marketing Group Faces Critical Liquidity Challenge Despite Strategic Partnerships

DBMM’s precarious liquidity and ongoing losses overshadow strategic partnership efforts amid a competitive digital marketing landscape.

Digital Brand Media & Marketing Group, Inc. disclosed alarming liquidity constraints in its July 2026 quarterly filing, with a current ratio near 0.01 and substantial net debt burden. Despite these financial headwinds, the company continues to champion its Digital Clarity platform and maintain strategic partnerships aimed at broadening service offerings. However, persistent net losses and a weak balance sheet severely limit its capacity to capitalize on industry growth drivers, leaving operational viability in question without new capital or improved financial metrics.

Latest Quarterly Filing Highlights: Acute Liquidity Stress Amid Strategic Initiatives

Digital Brand Media & Marketing Group, Inc. (DBMM) reported critical liquidity constraints in its July 2026 quarterly filing, with current liabilities totaling approximately $9.3 million vastly exceeding current assets near $58,500, resulting in an alarmingly low current ratio of about 0.01 [F1]. This severe imbalance signals acute short-term solvency risk, threatening the company’s ability to meet operational and financial obligations without external capital infusion or asset divestitures. The company’s net debt position stands near $263,000, derived from total debt of roughly $293,000 less modest cash reserves, underscoring a constrained cash runway and limited financial flexibility [F1]. Despite these headwinds, DBMM continues to promote its Digital Clarity platform and maintain strategic partnerships aimed at expanding its digital marketing technology and consulting service offerings [S2]. However, persistent net losses exceeding $1 million and a fragile balance sheet severely restrict the company’s capacity to invest in growth drivers or scale operations effectively [F1].

Digital Clarity Platform and Consulting Services: Revenue Model and Customer Engagement

DBMM’s core revenue engine centers on its Digital Clarity platform, a marketing technology solution designed to support digital brand media campaigns through analytics, campaign management, and customer engagement tools, complemented by consulting services focused on digital transformation and marketing strategy execution [S1]. The company’s business model blends subscription-like recurring revenue from platform usage with project-based consulting fees, reflecting a hybrid monetization approach common in the digital marketing sector. Key operating metrics influencing revenue include client acquisition rates, customer retention, and monthly recurring revenue (MRR) growth, which collectively drive contract renewals and expansion [S1]. However, with reported revenues around $138,000 as of August 2025, DBMM’s scale remains limited, constraining gross margin expansion and operational leverage despite growing demand for integrated marketing technology and data-driven brand media solutions [F1]. In a competitive landscape characterized by rapid innovation and evolving client expectations, DBMM’s ability to maintain high customer retention and demonstrate measurable campaign ROI will be critical to stabilizing and growing its revenue base.

Competitive Landscape: Positioning Among Agencies and Marketing Technology Providers

Within the digital brand media and marketing industry, DBMM competes against a spectrum of players including boutique digital marketing agencies offering specialized technology tools, integrated agencies combining creative content and marketing platforms, and SaaS marketing technology providers focusing on analytics and performance marketing. Larger incumbents such as HubSpot and LiveRamp exemplify well-capitalized peers with extensive product development, sales, and customer support capabilities. Compared to these competitors, DBMM’s smaller scale and limited disclosure of proprietary technology place it at a disadvantage in pricing power and client negotiation leverage. The sector’s high competition intensifies client churn risks and compresses margins through discounting and commoditization of services. Consequently, DBMM must leverage operational efficiency and strategic partnerships to differentiate its offerings and sustain client engagement amid these pressures.

Strategic Partnerships: Growth Opportunities and Operational Constraints

DBMM actively pursues strategic partnerships to broaden its service capabilities beyond the Digital Clarity platform, aiming to capture new client segments and enhance value propositions through integrated marketing technology solutions and co-delivered consulting services [S2]. Such alliances are vital growth levers in the digital marketing sector, enabling expanded channel reach and enriched service portfolios without proportionate fixed cost increases. However, the realization of partnership benefits depends heavily on DBMM’s operational capacity to execute joint initiatives effectively. Given the company’s precarious liquidity position and net debt burden [F1], there is substantial risk that limited cash flow and resource constraints could impair project delivery timelines and partnership management, thereby diminishing the potential impact of these collaborations.

Industry Growth Drivers Versus Financial Limitations

The digital brand media and marketing industry is buoyed by secular tailwinds including rising global digital advertising expenditures, accelerated adoption of AI-driven marketing automation, expansion of social media and influencer marketing, and increasing demand for sophisticated marketing analytics platforms. These trends create a sizeable addressable market receptive to integrated platforms like Digital Clarity combined with consulting services focused on digital transformation strategies. Nonetheless, DBMM’s ability to capitalize on these growth drivers is severely hampered by its financial condition. The company’s near-zero current ratio (~0.01) highlights imminent liquidity challenges, restricting investments in product innovation, sales and marketing expansion, talent acquisition, and infrastructure enhancements [F1]. Additionally, tightening data privacy regulations and heightened client expectations for demonstrable ROI intensify competitive pressures and client retention challenges. In a saturated market, continuous innovation and effective campaign management are essential for differentiation, yet these require capital and operational bandwidth that DBMM currently lacks.

Key Operating Metrics and Near-Term Watchpoints

Critical performance indicators to monitor include client acquisition and retention rates, monthly recurring revenue growth, campaign conversion rates, and partnership renewal success. These metrics provide insight into DBMM’s ability to sustain and grow its revenue base amid competitive pressures [S2]. Furthermore, announcements regarding new strategic partnerships, expansions of service offerings, or cost optimization initiatives will be important signals of the company’s operational resilience. Given the ongoing cash burn and liquidity constraints, any disclosures related to capital raises, refinancing efforts, or restructuring plans will be pivotal in assessing DBMM’s near-term viability and capacity to execute its growth strategy.

Financial Profile Summary: Balance Sheet Fragility and Operating Losses

DBMM’s latest financial snapshot reveals a fragile balance sheet with cash and equivalents around $30,200 (as of early 2022) and total debt approximately $293,253 as of May 2026, resulting in net debt near $263,051 after accounting for cash reserves [F1]. Current liabilities exceeding $9 million dwarf current assets near $58,500, producing an extremely low current ratio of approximately 0.01, indicative of acute short-term liquidity risk [F1]. This financial strain compounds ongoing operating losses reported at over $1 million, reflecting persistent cash burn and limited profitability [F1]. The combination of these factors underscores an urgent need for capital restructuring or external financing to mitigate insolvency risks and support operational continuity. Without such measures, DBMM’s ability to invest in innovation, sales growth, and partnership execution remains severely constrained.

Financial position in context

As of May 31, 2026, DBMM’s total debt stood at approximately $293,253 with net debt near $263,051 after subtracting cash reserves, highlighting a leveraged balance sheet with limited liquidity [F1]. The current ratio of roughly 0.01 reflects a significant short-term solvency challenge [F1].

This analysis integrates recent SEC filings with broader industry context to frame Digital Brand Media & Marketing Group’s operational and financial challenges within the evolving digital marketing technology landscape. The tension between the company’s strategic ambitions for its Digital Clarity platform and the stark liquidity pressures defines a critical inflection point where execution capability and financial health must improve to sustain competitive relevance.

This assessment is based solely on publicly filed disclosures and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments