Smurfit Westrock’s Post-Combination Growth and Integration Challenges Shaping 2025 Performance

The 2024 merger of Smurfit Kappa and WestRock formed a global paper-based packaging giant navigating integration, capital allocation, and regional diversification.

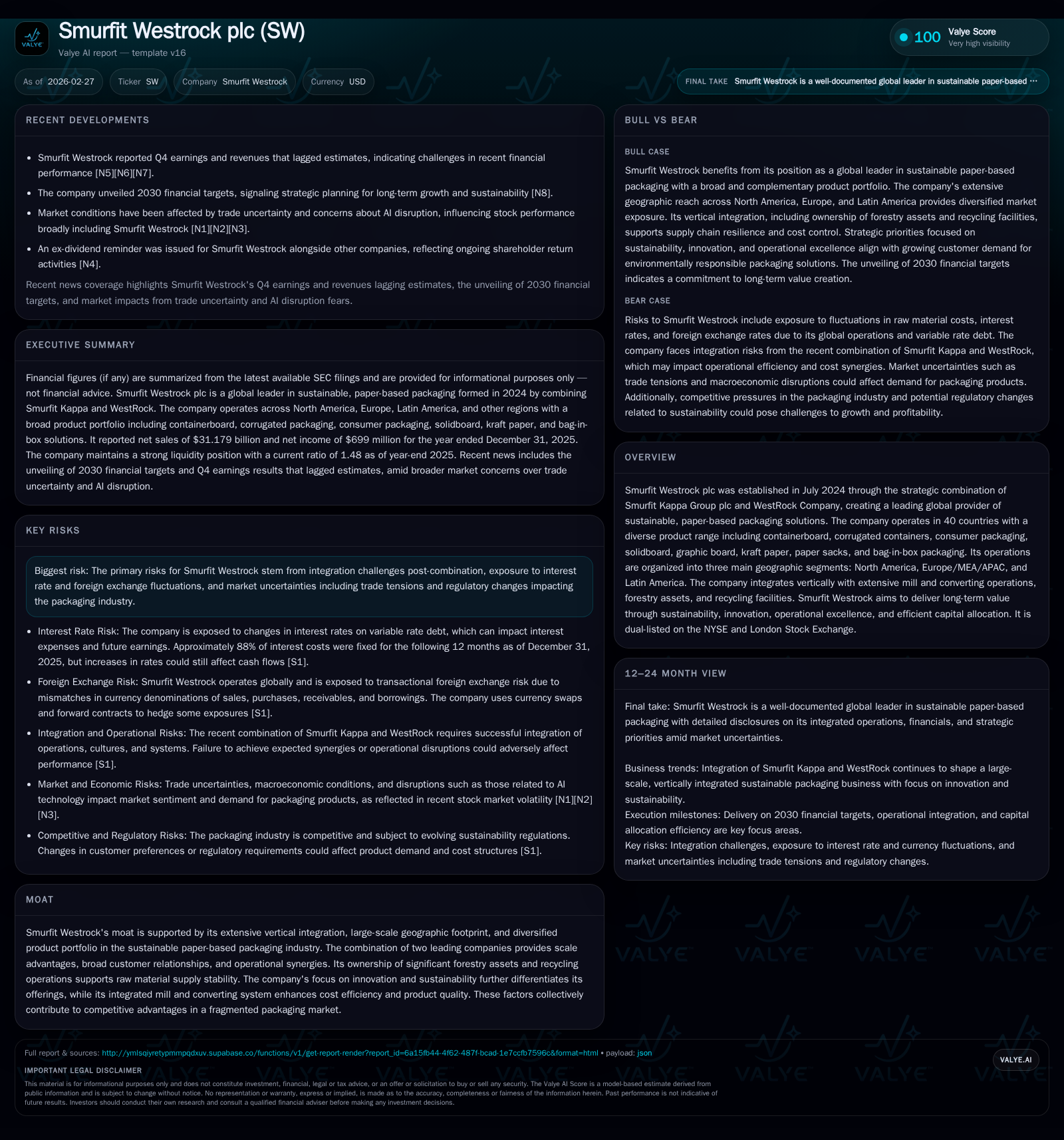

Formed in mid-2024, Smurfit Westrock plc quickly emerged as a leading global player in sustainable packaging across 40 countries via its vertically integrated mills and converting plants. The company's 2025 financials reflect robust top-line growth fueled by the merger's scale, particularly a near doubling of net sales and significant EBITDA expansion. Despite strong operating cash flow growth and disciplined capital investments, Smurfit Westrock faces notable integration headwinds, currency volatility, and regulatory risks that could temper near-term margin gains. Watch for progress on merger synergies, foreign exchange management, and balance sheet optimization to gauge future value creation.

Company Formation and Historical Performance

Smurfit Westrock plc was formed in July 2024 through the strategic combination of Smurfit Kappa Group plc, a European leader with significant Latin American operations, and WestRock Company, a major North American packaging provider [S1]. This merger created one of the largest global paper-based packaging companies with operations spanning over 40 countries.

The company employs a vertically integrated business model encompassing forestry assets and recovered fiber operations feeding into paper mills producing multiple grades of containerboard and paperboard. These raw materials are converted into corrugated containers and consumer packaging products across extensive converting plants [S8][S11][S12].

Financially, the merger drove substantial scale expansion. Net sales increased sharply from $21.1 billion in partial-year 2024 results to $31.2 billion in full-year 2025 [F1], reflecting full consolidation of both legacy businesses.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($mm) | Capex ($bn) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 699 | 3.4 | 1719 | 2.2 | +119.1% |

| 2024 | 319 | 1.5 | 1007 | 1.5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 900 | 0 | 1200 |

| 2024 | 650 | 27 | 17 |

Source: SEC companyfacts cache [F1].

Table: Summary Financial Metrics for Smurfit Westrock [F1]

Operating income rose approximately 70.7% year-over-year to $1.72 billion in FY2025 alongside a net income increase exceeding 119%, driven by operational leverage and synergy realization post-merger [F1]. Operating cash flow more than doubled to $3.39 billion while capital expenditures increased nearly 50% as investments focused on capacity modernization and integration efforts [F1].

Geographic Segment Overview

Smurfit Westrock organizes its operations into three segments aligned with geographic markets: North America; Europe/Middle East/Africa/Asia-Pacific (MEA/APAC); and Latin America [S8][S11].

North America accounted for approximately 58.5% of external net sales in FY2025 [S13]. This mature market segment includes an integrated portfolio spanning containerboard production, specialty paper grades such as kraft paper, converting capabilities including display assembly, and extensive recovered fiber collection operations [S14].

Europe/MEA/APAC covers diverse markets with production encompassing containerboard alongside specialty papers like graphic board and solidboard plus bag-in-box liquid packaging managed across multiple countries including European hubs as well as Canada and Mexico under this segment’s umbrella [S12][S13].

Latin America features pan-regional forestry assets (~308,000 acres) supporting mill systems focused on containerboard and kraft papers along with converting plants producing corrugated boxes and folding cartons [S12][S13].

Integration Strategy & Operational Risks

Post-merger integration remains critical for capturing anticipated synergies such as procurement consolidation, logistics optimization leveraging overlapping footprints, technology harmonization across mills, corporate overhead reduction, and cross-selling opportunities within the expanded customer base [S13].

Execution risks persist given cultural integration challenges across continents and disparate IT platforms inherited from legacy firms [N1][N2]. Regulatory scrutiny adds complexity amid pending antitrust litigation against subsidiaries in the U.S., requiring careful operational continuity management [S19].

Interest rate risk is managed partly through hedging with fixed-rate instruments covering about 88% of borrowings for the next twelve months at both year-end periods evaluated (December 31, 2024 & December 31, 2025) [S1]. Foreign exchange risk arises from significant non-U.S.-dollar revenues (~54% sourced outside the U.S. in FY25 down from ~65% previously), involving currencies such as euro, Mexican peso, Canadian dollar among others; this exposure introduces earnings translation variability [S1].

Commodity price risk is principally related to recovered paper input costs sensitive to global supply-demand dynamics amid rising demand for recycled containerboard driven by sustainability initiatives among customers [S1].

Capital Structure & Liquidity Profile

At December 31, 2025, Smurfit Westrock's debt portfolio comprised unsecured senior notes totaling roughly $13.8 billion spanning maturities through the mid-2030s with interest rates varying between low to high single digits depending on series currency denomination (USD or euro) [S15][S16][S21][F1].

Liquidity is anchored by a $4.5 billion multi-currency revolving credit facility extended through June 2030 with no outstanding borrowings at fiscal year-end plus receivables securitization programs totaling up to €330 million euro facilities due late-2029 and a $700 million USD program maturing mid-2027 providing short-term funding flexibility [S4][S6][S17].

Despite robust free cash flow estimated near $1.2 billion (operating cash flow less capex), no share repurchases occurred during FY25 while dividends increased markedly to $900 million reflecting management's commitment to shareholder returns alongside balance sheet strengthening following merger-related expenditures [F1].

Regulatory & Legal Considerations

Key legal contingencies include:

- A U.S.-based class action antitrust lawsuit targeting key subsidiaries alleging price-fixing involving containerboard products remains at an early procedural stage; Smurfit Westrock intends vigorous defense with recent dismissals at holding company level though subsidiaries remain defendants awaiting court rulings anticipated in calendar year 2026 [S19][N1].

- Environmental liabilities totaled approximately $67 million at December 31, 2025 related mostly to remediation obligations on legacy sites; insurance coverage offsets significant portions with no material adverse effect expected but closely monitored within contingent liabilities framework [S7][S18].

- Arbitration awards exceeding $469 million arising from Venezuelan expropriations introduce timing uncertainty pending annulment ruling hearings scheduled soon; prior competition fines imposed on Italian subsidiaries have been partially reduced after appeals demonstrating ongoing regulatory engagement within expected ranges [S15][S18].

Outlook & Key Monitoring Points

Given limited explicit forward guidance post-merger completion investors should track:

- Progress on synergy realization including cost savings versus pre-merger baselines.

- Effectiveness of foreign exchange hedging amid projected currency volatility.

- Capital deployment decisions balancing capacity reinvestments versus shareholder returns.

- Developments in pending litigations that could impact financial results.

- Innovation efforts tied to sustainability positioning given shifting customer preferences toward environmentally friendly packaging.

Recent Q4 reports indicate meaningful progress establishing an operational platform conducive to scale benefits despite typical large-scale integration challenges reflected partly in missed short-term earnings targets reported recently [N3][N6]. Strong cash flow generation supports strategic flexibility though ongoing risks warrant vigilant management.

This report is prepared solely for informational purposes based on publicly available data including SEC filings and reputable news sources as of February 2026; it does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments