Stryker Corporation: A Comprehensive Analysis of Its Medical Technology Leadership and Growth Dynamics

An in-depth review of Stryker’s diversified portfolio, competitive positioning, financial health, and risks in the evolving medtech landscape.

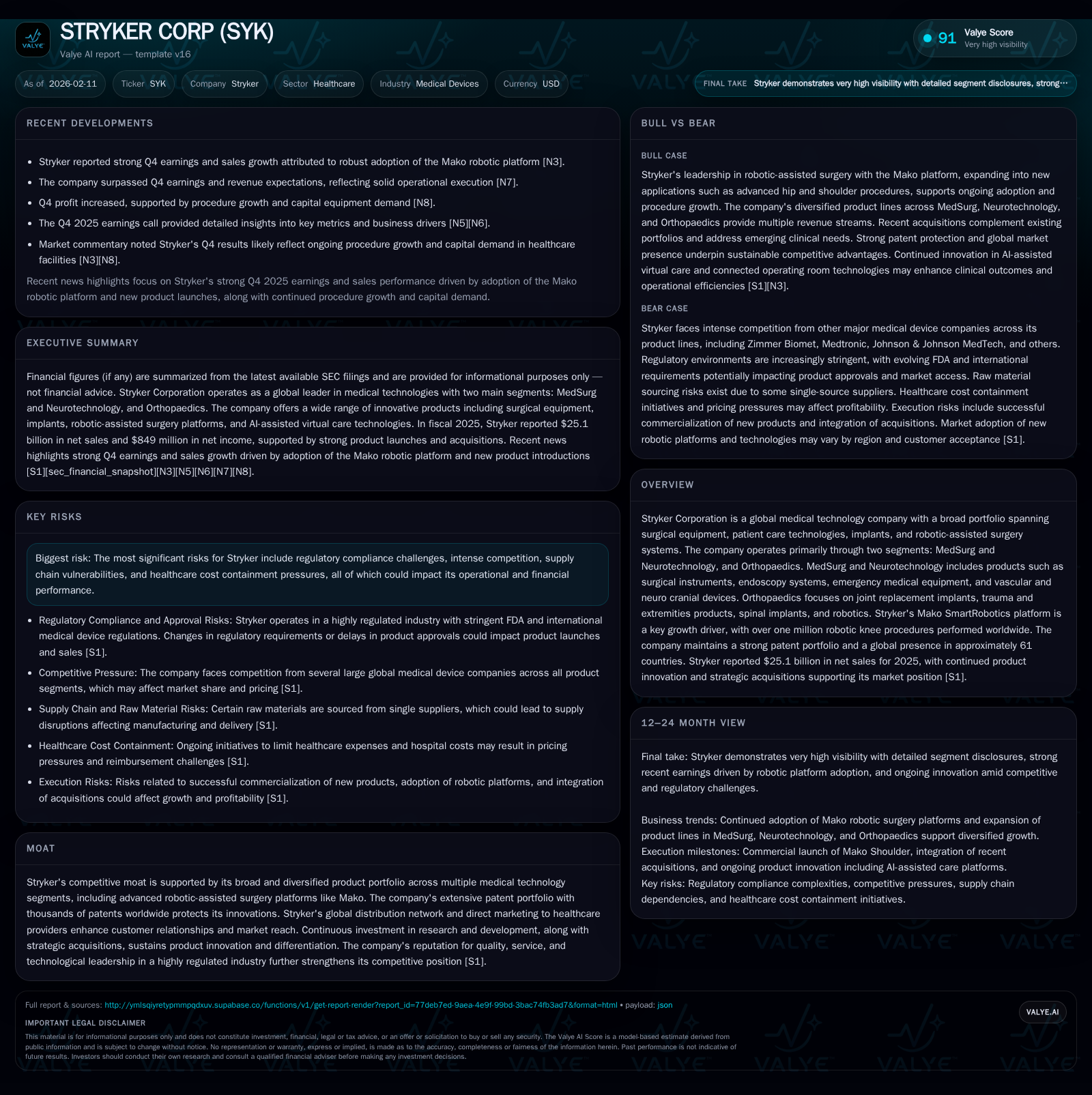

Stryker Corporation stands as a global powerhouse in medical technology, operating principally through two segments — MedSurg and Neurotechnology, and Orthopaedics. Its diverse product portfolio includes robotic-assisted surgery systems like the Mako platform, surgical instruments, and implants that collectively drive robust revenue growth and market presence. As of 2025, Stryker reported $25.1 billion in net sales supported by consistent innovation and strategic acquisitions. Nonetheless, the company faces industry-standard risks related to regulatory compliance, competitive pressures, supply chain challenges, and healthcare cost containment efforts.

Company Overview

Founded in 1946 as the successor to Dr. Homer H. Stryker's pioneering medical inventions dating back to 1941, Stryker Corporation has evolved into a global leader in medical technologies. Headquartered in Michigan, it services over 150 million patients annually across roughly 61 countries.

The company's operations are segmented into two reportable divisions:

- MedSurg and Neurotechnology (62% of total net sales in 2025), encompassing surgical equipment (instruments), endoscopy products, emergency medical equipment, patient handling technologies, vascular intervention devices for stroke treatment, neuro cranial products, and advanced clinical communication including AI-assisted virtual care.

- Orthopaedics (38% of total net sales), focused on joint replacement implants (hips, knees), trauma care devices, spinal implants, extremities products, and robotic-assisted surgery via its flagship Mako SmartRobotics platform.

This diversified segmentation allows Stryker to maintain resilience against market volatility specific to any single therapy area or technology.

Product Innovation and Competitive Moat

Central to Stryker's growth thesis is the Mako SmartRobotics system—an orthopaedic robotic-arm platform that has achieved over one million knee procedures globally [S1]. The platform exemplifies synergy between clinically proven outcomes and operational efficiency gains sought by hospitals. Beyond robotics, Stryker holds thousands of patents protecting innovations spanning minimally invasive vascular devices to AI-powered clinical communications.

Its competitive moat is reinforced by:

- A broad product portfolio avoiding overreliance on any single device or procedure.

- Direct relationships with healthcare professionals through a combination of company-owned subsidiaries and carefully selected third-party distributors.

- Continuous investment in research & development (R&D expense was $1.62 billion in 2025), fueling pipeline robustness.

- Strategic acquisitions enhancing core competencies while expanding addressable markets.

- Reputation for product quality and regulatory compliance enhancing trust among clinicians.

Competitors include Zimmer Biomet in instruments and implants; Medtronic globally; Johnson & Johnson MedTech; Olympus in endoscopy; Smith & Nephew; ConMed Linvatec; Arthrex; and STERIS among others [S1].

Financial Performance Highlights

In fiscal year 2025:

- Net sales reached $25.116 billion representing a continued upward trajectory from $22.595 billion in 2024.

- Gross profit totaled $16.065 billion with operating income at $4.889 billion indicating strong operational leverage amid rising expenditures.

- Net earnings were $3.246 billion or approximately $8.40 per diluted share.

- Operating cash flow generation remained robust at $5.044 billion providing ample liquidity for innovation investments ($761 million capex) and acquisitions (net $4.96 billion) [F1].

Balance sheet strength is evidenced by current assets of $14.755 billion versus current liabilities of $7.794 billion yielding a solid current ratio near 1.89 [F1]. Total debt stood at nearly $15.9 billion but is offset by shareholder equity of $22.42 billion underpinning capital structure resilience.

Dividend distributions grew modestly to $3.40 per share in 2025 reflecting confidence in free cash flow sustainability [S1]. Though authorized share repurchases have an available capacity exceeding $1 billion at year-end 2025, no repurchases occurred recently [S1].

Operational Footprint

Stryker employs approximately 27 company-owned locations alongside more than 300 leased sites including manufacturing facilities (55 total). These strategic manufacturing hubs ensure stable supply chains essential for high-quality medical device production globally [S1].

The geographic blend involves direct sales subsidiaries facilitating regional customization without sacrificing global economies of scale.

Industry Context & Strategic Positioning

The broader medical device industry faces several converging trends impacting players such as Stryker:

- Increased adoption of robotic-assisted surgeries requiring capital spending but promising improved patient outcomes.

- Growing demand for minimally invasive therapies aligned with aging populations worldwide driving orthopedic implant volumes.

- Heightened regulatory scrutiny across markets imposing compliance costs but creating barriers to entry for new competitors.

- Healthcare payers increasingly emphasizing cost-effectiveness influencing pricing strategies.

Against this backdrop, Stryker's dual focus on innovation-led growth combined with expanding its digital health solutions positions it favorably relative to peers reliant on commodity-like products or facing slower adoption curves [analysis].

Risks & Considerations

Key risk factors facing Stryker include:

- Regulatory Compliance: As a global manufacturer of Class II/III medical devices involving surgical robotics and implants, regulatory approvals remain challenging with potential delays or recalls impacting reputation.

- Competition: The landscape features entrenched global companies aggressively innovating; losing market share or pricing pressure could impact margins.

- Supply Chain Vulnerabilities: Geopolitical disruptions or raw material shortages may affect production timelines causing revenue volatility.

- Healthcare Cost Containment: Efforts by governments and insurers to reduce procedural costs could limit pricing power despite product advantages.

Management disclosure also notes ongoing legal proceedings typical of large medtech firms covering product liability suits and intellectual property disputes without immediate material impact noted [S1].

Recent Developments & Market Reaction

Recent fourth-quarter results beat consensus estimates driven by strong Mako procedure adoption contributing to higher capital equipment demand [N1–N4]. This underlines the strategic emphasis on robotics as a differentiation lever going forward.

The company continues pursuing acquisition opportunities while strategically investing in next-generation technologies spanning AI-enabled clinical platforms adding value beyond hardware-centric offerings [N2]. These initiatives address both short-term growth avenues and longer-term shifts towards integrated digital care pathways.

Conclusion

In summary, Stryker Corporation exemplifies a well-diversified medtech leader leveraging technology innovation such as robotic surgery alongside comprehensive implant portfolios to sustain revenue growth exceeding $25 billion annually. Its patent-rich environment combined with extensive distribution capabilities creates high entry barriers while consistent R&D investment fuels future readiness.

Nevertheless inherent risks linked to regulatory pressures, competitive intensity, supply operations, and payer dynamics warrant continuous vigilance from management to preserve margins and market position amid evolving industry conditions.

This analysis is intended solely for informational purposes based on publicly available data as of early 2026 without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments