Protara Therapeutics Drives Clinical Momentum with TARA-002 and Solid Liquidity Position

Protara's latest quarter highlights continued clinical progress on its lead cell therapy and a stable financial runway to fund ongoing development.

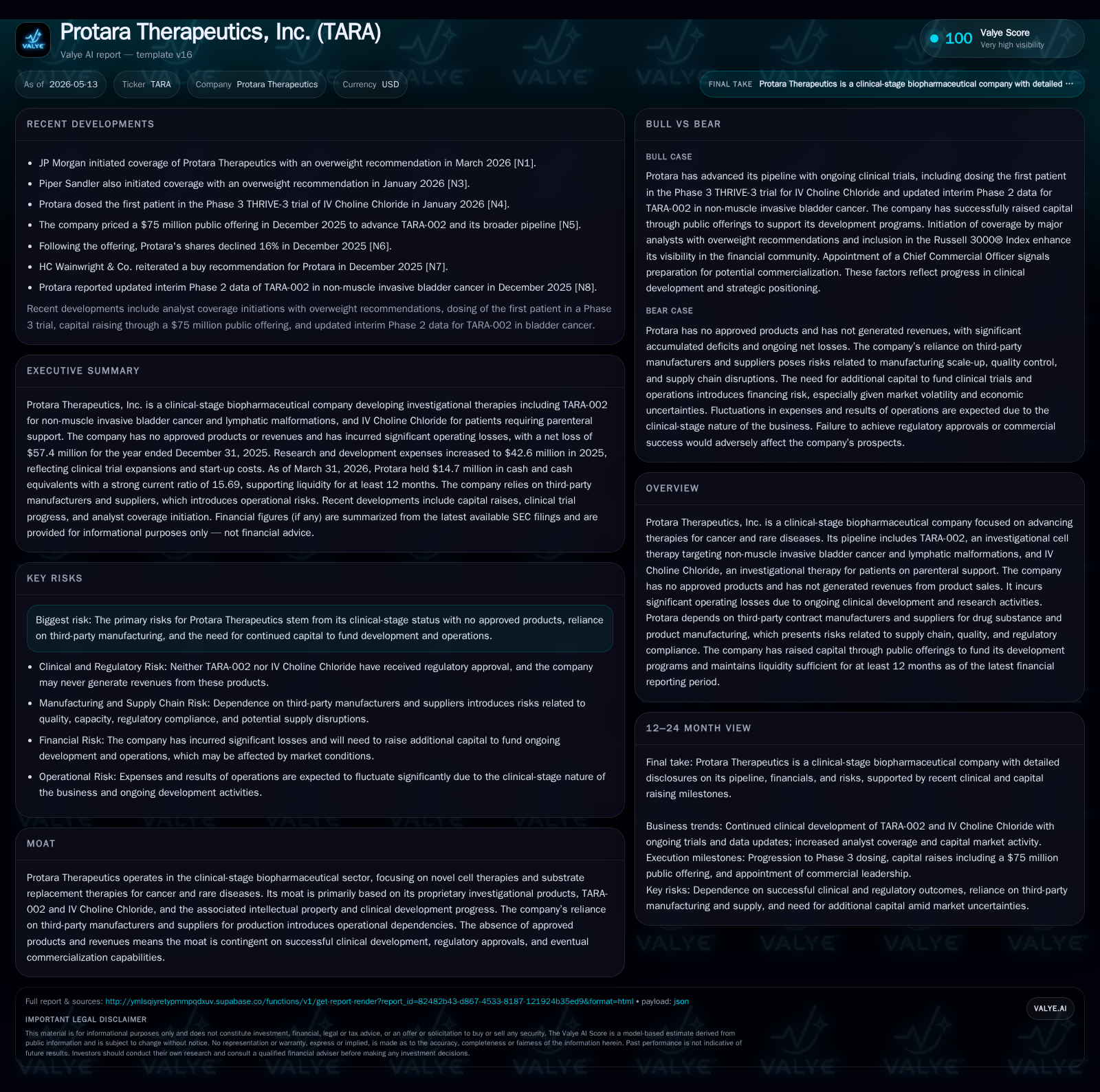

In its Q1 2026 filing, Protara Therapeutics reported steady advancement in its investigational cell therapy program TARA-002 targeting non-muscle invasive bladder cancer and lymphatic malformations, alongside maintenance of robust liquidity supporting at least twelve months of operations. The company remains early-stage, with no approved products or revenues, focusing on clinical development funded by capital raises. Growth hinges on successful trial outcomes and regulatory milestones, while risks include high development risk and dependence on third-party manufacturing. The cash position of approximately $14.7 million and strong current ratio underpin operational continuity but emphasize the need for additional financing to sustain the pipeline.

Latest Quarterly Operating Update: Clinical and Financial Highlights

Protara Therapeutics’ most recent quarterly report filed on May 13, 2026 ([S2]) alongside a contemporaneous 8-K announcement ([S3]) provided clear confirmation that its clinical-stage development is proceeding in line with strategic priorities. No material changes were reported in previously disclosed risk factors ([S2]), signaling consistent operational dynamics amid an active research phase. The company continues to incur operating losses as expected at this stage due to ongoing investment in clinical trials.

Financially, as of the quarter ended March 31, 2026, Protara maintains approximately $14.7 million in cash and equivalents ([F1]), supported by a strong current ratio of about 15.7 reflecting conservative liability management relative to assets ([F1]). Total debt remains minimal at roughly $370 thousand (measured as of late 2020) ([F1]), effectively rendering net debt negative. This liquidity profile underscores the company's ability to sustain operations without immediate refinancing needs but highlights the inherent necessity for future capital raises given burn rates typical in clinical biopharma.

Investor communications coupled with these filings emphasize the company’s focus on executing registrational clinical trials for TARA-002 in NMIBC and lymphatic malformations (LMs), as well as progressing IV Choline Chloride toward potential regulatory filings.

Business Model Overview: Pipeline Focus and Revenue Absence

Protara operates purely as an R&D-driven clinical-stage biotech entity without commercial products or revenues ([S1], [S4]). Its business model centers on the advancement of proprietary investigational therapeutics through preclinical studies and multi-phase clinical trials toward market approval. Revenue generation is contingent on successfully bringing these candidates through regulatory hurdles—a process inherently lengthy and capital-intensive.

Its lead compound TARA-002 is a novel cell therapy designed for NMIBC patients who often face limited options outside invasive procedures; additionally, TARA-002 is being evaluated for lymphatic malformations—rare abnormalities of the lymphatic system where treatment options are scant ([S1]). Complementing this is IV Choline Chloride, an investigational phospholipid replacement therapy targeting metabolic needs in patients dependent on parenteral nutrition support ([S1]).

The company outsources significant portions of drug substance manufacturing to contract manufacturing organizations (CMOs) and relies heavily on third-party suppliers for quality compliance and timely delivery (). While this strategy reduces fixed costs associated with owning manufacturing infrastructure, it creates operational dependencies that require rigorous supplier oversight to mitigate supply disruptions—a known challenge in cell therapy production characterized by complex chemistry, manufacturing, and controls (CMC).

R&D expenditure is the dominant operating cost driver—comprising personnel costs including research staff salaries and stock-based compensation; payments to CROs/CDMOs for clinical trial material manufacture; regulatory affairs; and site-related expenses ([S1]). In contrast, general administrative expenses support corporate governance, investor relations, regulatory compliance (e.g., Nasdaq listings), legal services, and other overhead typical of a public biotech firm.

Industry Context: Competitive Cell Therapy and Rare Disease Landscape

Protara competes within a specialized segment of biotechnology focusing on transformative cell therapy approaches for oncology indications such as NMIBC as well as rare diseases like lymphatic malformations—areas marked by high unmet medical needs but also significant regulatory scrutiny ([S1]). The underlying competitive landscape includes established biopharma firms advancing CAR-Ts or other adoptive cell therapies alongside emerging innovators exploring alternative modalities.

Entry barriers into this sector are steep given the intricate logistics of patient-specific cell product manufacturing, stringent FDA requirements for CMC consistency, safety profiling challenges inherent to living medicines, plus intellectual property defenses necessary to preserve exclusivity. Differentiation comes from proprietary engineering approaches embedded in TARA-002’s design aimed at enhancing efficacy or reducing side effects compared to existing local treatments like BCG instillation for NMIBC.

The industry’s lengthy timelines from trial initiation through approval mean structural demand drivers are measured over years rather than quarters. Furthermore, switching costs are elevated due to physician familiarity requirements with novel treatment administration protocols as well as insurance reimbursement complexities tied to innovative therapeutic classes.

Growth Opportunities: Advancing Clinical Trials and Regulatory Pathways

Protara’s near-to-medium term growth trajectory depends heavily on successful progression through registrational trials—particularly pivotal data readouts relating to efficacy endpoints in NMIBC patients receiving TARA-002. Positive outcomes could catalyze interactions with the FDA pushing toward marketing approval submission pathways. Likewise, further advancement of the LM indication could broaden addressable markets by targeting underserved patient populations with few effective therapies currently available.

For IV Choline Chloride, establishing safety and metabolic benefit profiles for patients reliant on parenteral nutrition may leverage orphan drug designation pathways facilitating accelerated regulatory pathways ([S5], [S6]).

Potential pipeline expansions or licensing deals could also augment value creation if Protara demonstrates durable clinical benefits or expands indications into related oncologic or rare disease categories.

Risk Factors: Clinical, Operational Dependencies, and Capital Needs

Consistent with all early-stage biopharma enterprises focused exclusively on investigational products without approved commercial offerings ([S1], [S2]), Protara faces substantial inherent risks:

- High attrition risk typical of drug development projects where regulatory rejection or negative trial results can materially impair asset value.

- Dependence on external CMOs/CDMOs increases vulnerability to supply chain disruptions or compliance issues impacting trial timelines.

- Continuous capital requirements impose pressure to raise funds amid potentially volatile equity markets which may dilute shareholders if done frequently.

- No current revenues mean all operations hinge on external financing cycles; delays or down rounds could constrain development pace.

- Competitive threats from other cell therapy developers advancing faster or garnering stronger efficacy/safety profiles may limit market opportunities post-approval. These factors underscore why operational execution transparency paired with prudent financial management is critical during this phase ([S2]).

Upcoming Catalysts: Clinical Milestones and Capital Management

Critical upcoming events revolve around scheduled Phase II/III trial completions or interim data disclosures for TARA-002 across both target indications; such announcements would provide essential de-risking signals at potential valuation inflection points ([S5], [S6]). Parallel progress towards Investigational New Drug (IND) application approvals or Orphan Drug designations can accelerate timelines.

Investor focus should also monitor communications regarding capital raising activities necessary to fuel milestone-driven expense outlays—such announcements will be key indicators of runway adequacy beyond twelve months currently supported by cash reserves ([F1]). Strategic partnerships or licensing agreements formed during this period could also influence prospects.

Financial Snapshot: Liquidity and Expense Profile

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $15mm | |

| 2026-03-31 | ||

| Current assets | $140mm | |

| 2026-03-31 | ||

| Current liabilities | $9mm | |

| 2026-03-31 | ||

| Current ratio | 15.69x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $14.7 million | |

| 2026-03-31 | ||

| Total Debt | ~$370 thousand | |

| 2020-09-30 | ||

| Current Ratio | 15.69 | |

| 2026-03-31 | ||

| Net Income (Annual) | -$57.4 million | |

| 2025-12-31 |

Protara carries sufficient liquidity today at about $14.7 million cash reserves with nominal debt outstanding as per latest disclosures ([F1]). The current ratio signifies ample short-term asset coverage against liabilities supporting fiscal stability while burn trends reflect intensive R&D spending consuming near-$60 million annually consistent with staged clinical program execution ([F1], [S3]). Maintaining adequate funding ahead remains imperative given absence of product-generated inflows.

Disclaimer: This analysis is based solely on publicly available SEC filings as of May 13, 2026. It does not constitute investment advice or recommendations. All forward-looking statements referenced reflect management’s expectations subject to known industry risks detailed within Protara’s disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments