K&F Growth Acquisition II Nears Business Combination Deadline Amid High Stakes

The SPAC faces an impending November 2026 deadline to complete a Business Combination, intensifying competitive and regulatory pressures.

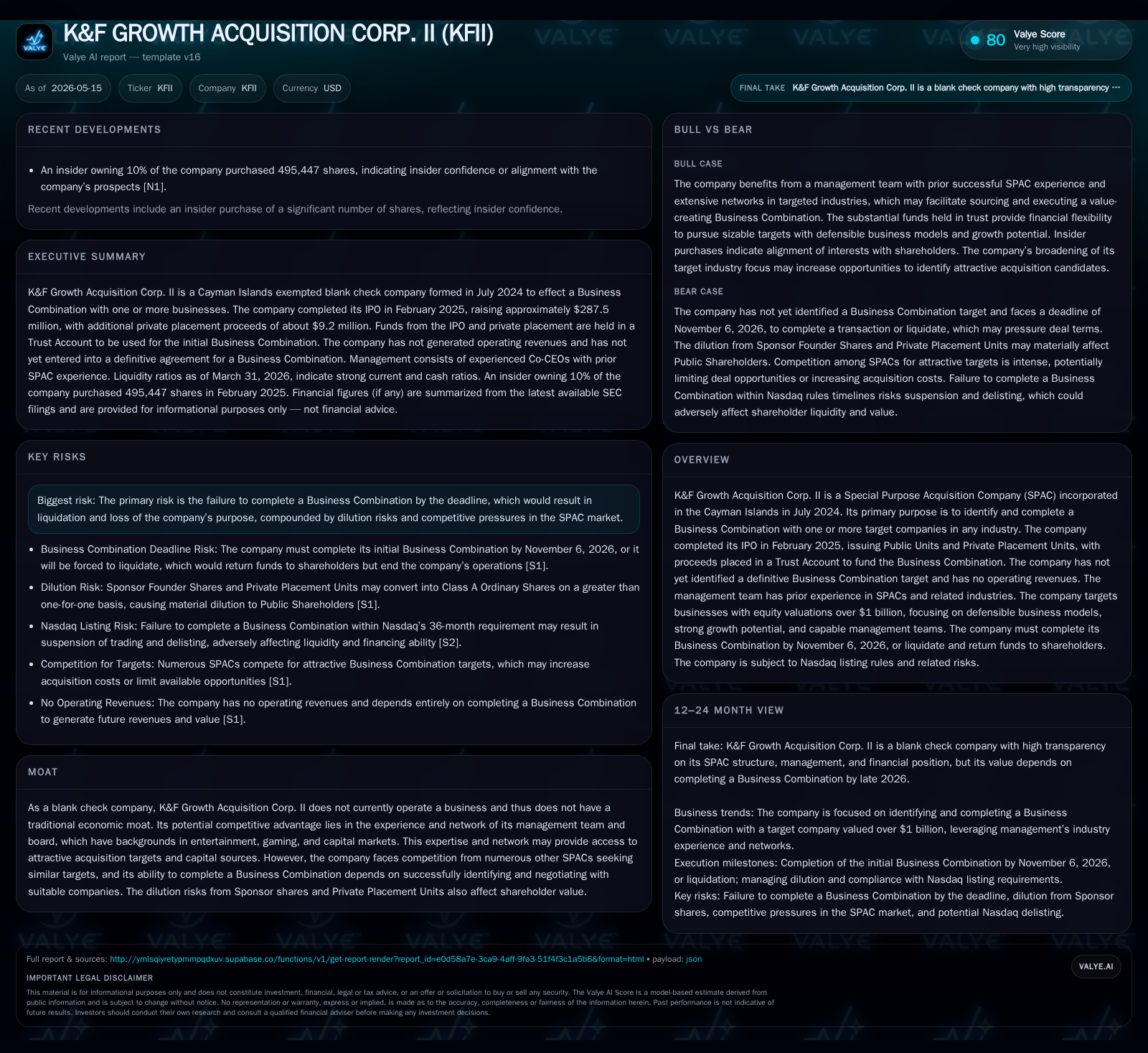

K&F Growth Acquisition Corp. II remains a blank check company with no operating revenues as it approaches its statutory deadline to consummate a Business Combination by November 6, 2026. The latest 10-Q confirms no material changes in risk factors but underscores the Nasdaq delisting risks if the combination is not completed timely. The company's strategy hinges on leveraging experienced management to identify a defensible, growth-oriented target exceeding $1 billion valuation. However, fierce competition among SPACs, shareholder dilution from sponsor shares and redemptions, and regulatory time constraints pose significant challenges. Monitoring progress toward a definitive agreement and possible extension proposals will be critical in the coming months.

Latest Operating Update Highlights and Implications

The quarterly 10-Q filing dated May 14, 2026 confirms that K&F Growth Acquisition Corp. II continues without a definitive Business Combination agreement as it nears the end of its initial combination period set for November 6, 2026 [S2]. The filing underscores that no material changes have arisen in risk factors since prior disclosures but stresses regulatory compliance urgency due to Nasdaq listing rules. Specifically, should the company fail to consummate a Business Combination by the deadline or any approved extension prior to February 4, 2028, its securities face immediate suspension from trading followed by delisting procedures under Nasdaq’s ‘‘36-Month Requirement.’’ This status would trigger adverse consequences including diminished attractiveness to targets and potential degradation of shareholder value.

These developments highlight a shrinking window to complete a strategic merger or acquisition, reinforcing operational inertia without affirmative deal announcements. The management must balance due diligence rigor with expediency given both market perception risk and contractual expiration looming less than six months away.

Business Model and SPAC Structural Overview

K&F Growth Acquisition Corp. II operates as a Special Purpose Acquisition Company (SPAC), a Cayman Islands exempted company focused solely on effecting a public merger with one or more target businesses [S1]. It completed its IPO in February 2025 by offering Public Units at $10 each along with simultaneous private sales of Private Placement Units to its Sponsor and BTIG totaling approximately $297 million in gross proceeds [S1][S10]. These funds were placed into a Trust Account governed by strict protective covenants designed to preserve capital until deployment.

Crucially, K&F II has no operating revenues—the business model depends entirely on identifying and negotiating a Business Combination that creates shareholder value post-transaction [S1][S10]. Revenue mechanics are therefore transactional; proceeds collected via units sold initially fund acquisition payments or serve in working capital once combined. The Sponsor’s investment via Private Placement Units provides aligned skin-in-the-game but introduces dilution risk for public investors due to preferential ownership terms [S13].

Management incentives focus on disciplined valuation assessment aligned through rigorous deal structuring and economic incentive harmonization aiming to unlock long-term returns from acquisitions valued typically over $1 billion [S3][S6]. This emphasis on large-scale deals aims at targeting established companies with enduring revenue streams or growth prospects sufficient to justify the public listing premium achieved via SPAC conversion.

Competitive and Market Position in the SPAC Ecosystem

K&F II operates within an intensely competitive SPAC ecosystem where many similar blank check companies vie for attractive acquisition candidates [S6]. Despite parity in structural form factors—IPO proceeds locked in trust accounts pending mergers—the company attempts differentiation through leveraging management’s deep experience across entertainment, gaming, live events, destination hospitality, and mobile gaming sectors [S1][S3][S12]. This domain expertise affords enhanced access to networks of founders, investors, and management teams potentially yielding proprietary deal flow opportunities unavailable to less connected sponsors.

However, competitive disadvantages persist given that rivals may possess larger financial resources or more flexible capital structures enabling them to outbid or outmaneuver K&F II in pursuit of premium targets. Additionally, Public Shareholder redemption rights combined with Sponsor dilution create complex capital allocation challenges which may dissuade some target companies wary of shareholder base instability or ownership concentration effects post-combination [S6][S13].

In this environment, execution discipline—balancing aggressive valuation negotiation with prudent risk mitigation—becomes central to successfully consummating transactions before mandated deadlines while preserving share price integrity.

Growth Path: Targeting Attractive Businesses Amid Market Pressures

K&F II’s target profile emphasizes companies with equity valuations exceeding $1 billion possessing highly defensible business models grounded in sustained consumer loyalty driven by differentiated experiences [S3]. Targets are ideally positioned within secular growth sectors such as regulated gaming industries where liberalizing regulations open avenues for rapid expansion coupled with robust cash flow profiles.

The strategic rationale involves unlocking shareholder value through enhanced market positioning linked with public market listing benefits—greater access to debt and equity capital markets, expanded branding opportunities, talent acquisition leverage through equity incentives, and potential for transformative acquisitions post-merger [S3][S9]. This comprehensive value creation model hinges on synergizing incumbent management teams’ operational capabilities with K&F II’s broad investor network and capital markets expertise.

Nevertheless, heightened competition among SPACs limits available quality targets while macroeconomic uncertainties could depress valuations or increase borrowing costs needed for transaction financing exacerbating deal execution complexity. Accordingly, success depends not only on target identification but also on securing attractive combination terms that support sustainable growth trajectories for the combined entity.

Risk Factors and Challenges Facing Completion

The principal existential risk facing K&F II is failure to consummate any Business Combination by November 6, 2026—or any shareholder-approved extension—forcing liquidation and return of Trust Account proceeds less administrative costs [S2][S23]. Such forced dissolution would terminate the company’s purpose causing complete loss of operational momentum.

Compounding this deadline constraint are Nasdaq listing rules mandating immediate suspension followed by delisting procedures should the ‘‘36-Month Requirement’’ lapse without transaction closure [S2]. This potential outcome carries deleterious effects including reduced liquidity, diminished public profile deterring target businesses’ interest, and reputational harm impairing future fundraising abilities.

Financially dilutive elements such as Sponsor Founder Shares acquired at nominal prices generating substantial overhang plus outstanding Private Placement Units further pressure Public Shareholders’ value continuity pre- and post-combination [S13]. Redemption rights exercisable upon combination approval can reduce transaction proceeds available for target purchase complicating financing plans requiring potential third-party capital raises which themselves risk additional dilution or restrictive covenants [S15][S27].

Finally, operational risks include limitations in assessing target management teams’ suitability post-acquisition along with integration challenges common in corporate carve-outs or private equity exits targeted by K&F II’s acquisition strategy [S24]. These multi-faceted risks necessitate prudent governance vigilance.

Upcoming Milestones and Key Events to Monitor

Investors should closely monitor several pivotal forthcoming events shaping K&F II’s trajectory:

- Disclosure of any proposed amendments extending the Business Combination deadline requiring shareholder approval with attendant redemption opportunities reducing Trust Account balances.

- Announcements regarding identification of definitive Business Combination candidates signaling transaction imminence.

- Scheduling of shareholder meetings or tender offers related to approval processes for proposed combinations.

- Potential secondary equity or debt financing arrangements intended to augment available transaction capital.

- Regulatory filings updating Nasdaq compliance status amid approaching timeline thresholds. Each milestone will represent critical inflection points potentially impacting deal feasibility perceptions as well as stock market trading dynamics.

Financial Position: Current Liquidity and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $413053 | |

| 2026-03-31 | ||

| Current liabilities | $2166 | |

| 2026-03-31 | ||

| Current ratio | 190.7x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026 (latest quarter end), K&F Growth Acquisition Corp. II held current assets totaling approximately $413K against negligible current liabilities near $2K yielding an exceptionally high current ratio around 190x—a testament to minimal short-term obligations relative to liquid resources [F1]. Cash & equivalents stood near $711K as reported September 30, 2025 confirming ample liquidity reserves maintained largely within Trust Account structures consistent with SPAC conventions [F1]. Debt levels remain modest at roughly $218K last available December 31, 2024 data evidencing very low leverage; net debt is effectively negative given cash dominance supporting financial flexibility absent recurring operating obligations pre-combination [F1].

This robust liquidity profile positions K&F II well financially for deploying acquisition capital when an appropriate target is identified; however incremental funding needs might arise depending on redemption activity levels or deal structuring requirements necessitating potential third-party financing commitments subject to market conditions [S15][S27].

Disclaimer: This analysis is based exclusively on information disclosed in publicly filed SEC documents through May 15, 2026 combined with industry-standard assessments. It does not constitute investment advice. Any forward-looking statements referenced herein are subject to inherent uncertainties outside current visibility. Readers should conduct independent due diligence before making decisions related to K&F Growth Acquisition Corp. II.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments