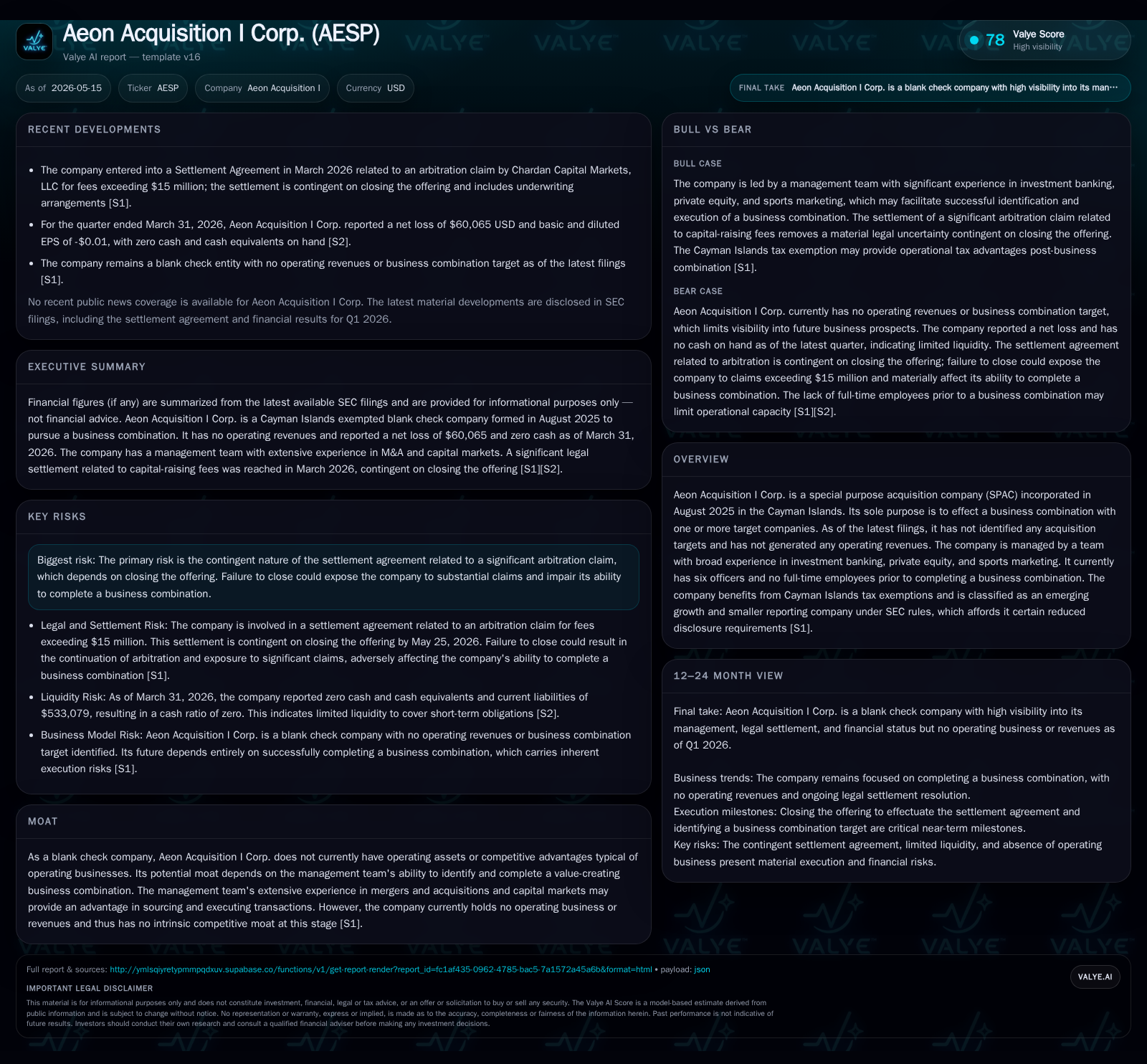

Aeon Acquisition I Corp.: Arbitration Settlement and Strategic Setup for Business Combination

Aeon Acquisition I Corp.’s recent quarterly filing reveals a critical arbitration settlement contingent on closing its SPAC offering by May 25, 2026, a legal development that directly shapes its path toward completing a business combination.

The company’s May 2026 10-Q filing highlights a binding arbitration settlement with Chardan Capital Markets that depends on completing the SPAC offering shortly, making this deadline pivotal for avoiding multi-million dollar litigation risks. Aeon Acquisition remains a blank check company with no operating revenues or target identified but benefits from a management team with deep expertise in mergers and acquisitions and capital markets. The structure as a Cayman Islands exempted emerging growth company offers tax and reporting flexibility but also embeds regulatory and market risks typical of SPAC vehicles today. Looking ahead, successful closing of the offering is the essential next step to unlock value creation via acquiring an operating business.

Latest Quarterly Update Highlights

Aeon Acquisition I Corp.'s most recent quarterly filing dated May 14, 2026 (10-Q) crystallizes the near-term operational narrative around a key legal and financial milestone: a binding Settlement Agreement tied to an outstanding arbitration claim filed by Chardan Capital Markets. This Settlement Agreement, reached in March 2026 after contentious proceedings, requires the company to close its SPAC offering by May 25, 2026. Failure to meet this deadline results in automatic termination of the agreement, reopening potential claims exceeding $15 million against the firm and its affiliates.

This conditionality places immense pressure on Aeon Acquisition’s capital raising timeline. The Settlement Agreement provides that upon closing of the offering—deemed the “Effective Time”—the arbitration matters will be fully resolved with dismissal and mutual releases among involved parties. Importantly, this deadline is not merely procedural but carries significant strategic gravity: without timely closure, Aeon's ability to complete any initial business combination—the very purpose of its existence—faces substantial impairment.

Thus, the latest SEC disclosure foregrounds litigation risk mitigation as directly tied to fundraising success. The company must navigate regulatory approvals, market dynamics, and underwriting coordination within this compressed timeframe to avoid a costly reset of legal exposure.

Aeon Acquisition’s SPAC Business Model and Management Team

Aeon Acquisition I Corp. operates as a classic special purpose acquisition company (SPAC), incorporated August 1, 2025 in the Cayman Islands as an exempted entity. It has no operating revenues or ongoing business operations and exists solely to identify one or more private companies for merger or acquisition (a “Business Combination”). This blank-check structure inherently means it generates revenue primarily through investor funds raised during its initial public offering (IPO) phase held in trust pending deal execution.

Critically, Aeon's management team brings a depth of experience often considered essential for navigating competitive M&A landscapes under SPAC models. Led by CEO Demetrios Mallios—founder of The Aeon Group Inc. with over three decades spanning fund management and investment banking—and CFO Alan Lewis, who has co-founded multiple ventures alongside extensive investment banking expertise focused on digital innovation sectors, the team's collective background encompasses private equity, capital markets structuring, strategic planning, and sports marketing.

This skill set positions Aeon well in theory to source attractive deals in sectors aligned with evolving technology trends or digital transformation themes; however, it remains without disclosed acquisition targets as of current filings. The absence of full-time employees before an initial Business Combination further illustrates typical operational minimalism specific to SPACs at this developmental stage.

Industry Context for Blank Check Companies

Aeon's incorporation offshore as a Cayman Islands exempted company offers notable tax advantages: exemption from local income taxes on profits or gains for twenty years post-undertaking grants financial flexibility uncommon among typical U.S.-domiciled entities. Coupled with status as an "emerging growth company" under SEC definitions (under JOBS Act provisions), Aeon benefits from reduced disclosure requirements such as simplified auditing rules and deferred adoption of new accounting standards. Additionally classified as a smaller reporting company enables further scaled-back compliance obligations.

These regulatory designations provide capital raising efficiencies but come with trade-offs: investors may demand higher equity risk premiums given limited transparency relative to mature public companies. The current climate for SPACs is marked by increased regulatory scrutiny following concerns about disclosure adequacy post-Business Combination along with market saturation impacting sponsor incentives and valuation expectations.

Underwriting agreements embedded in Aeon's settlement tie lead underwriting roles expressly to parties involved in litigation resolution efforts (Chardan as lead book-runner), implicating alignment between capital formation strategies and existing legal negotiations—a complexity familiar among recent blank check issuance structures competing amidst PIPE financing demands.

Arbitration Settlement Impact and Regulatory Risks

The $15 million arbitration claim from Chardan Capital Markets revolves around fees tied to historical capital-raising activities predating Aeon's formation but encompassing potential SPAC-related transactions negotiated through engagement letters issued in 2023–24. The March 26 Settlement Agreement effectively pauses these disputes contingent on successful capital raise closure.

Management indemnities from CEO Mallios and affiliate entities underpin protections shielding shareholders from direct exposure should claims arise. However, if the offering does not consummate by May 25 without extension consent from Chardan and D. Boral Capital LLC (co-lead underwriter), the settlement ceases effect automatically. Consequently, arbitration resumes with material adverse consequences anticipated including costly litigation expenses plus reputational damage that could deter future investors or partners.

This interdependence between legal resolution and fundraising underscores how intertwined corporate governance considerations are within SPAC structures where sponsor incentives intersect tightly with underwriting arrangements.

Growth and Strategic Path Forward

Aeon Acquisition's growth trajectory remains contingent principally on consummating its initial Business Combination successfully post-offering closure. Management's experience cultivating private equity funds coupled with broad M&A backgrounds should aid identification and negotiation of potential targets ideally aligned with digital innovation trends or sectors where their sports marketing expertise might create synergies.

Absent announced targets or pipeline disclosures so far, execution risk dominates growth prospects; competition among numerous blank check companies necessitates swift progress once capital is secured. Moreover, linking successful litigation resolution via arbitration settlement to underwriting agreements exemplifies strategic maneuvering aimed at smoothing pathway for deal closure while balancing complex sponsor-underwriter interests.

If executed effectively within regulatory constraints inherent to emerging growth companies and offshore tax regimes leveraged here, Aeon could unlock value creation reminiscent of successful SPAC combinations targeting tech-enabled firms.

Risks and Governance Watchpoints

Foremost among risks is failure to close the scheduled offering by May 25 which would dissolve the arbitration settlement agreement leaving disruptive multi-million-dollar claims active—an existential threat at this nascent stage given AEON’s purely shell nature without intrinsic operating cash flow.

Additional governance watchpoints derive from its status allowing reduced disclosure obligations; while cost-efficient operationally, these raise investor considerations around transparency standards especially given small core team size (six officers) that limits operational bandwidth prior to Business Combination completion.

Market volatility affecting blank check vehicles newly listed amid increased SEC oversight also factors into structural risks concerning timing windows available before regulatory mandates like Sarbanes-Oxley internal control evaluations kick in post-merger stage.

Lastly, intertwining underwriting compensation allocations within legal settlements represents both an alignment mechanism and potential source of conflicts requiring careful navigation through forthcoming filings.

Key Upcoming Milestones to Monitor

Several specific near-term milestones deserve attention:

- May 25, 2026: Critical deadline for closing the SPAC offering which activates arbitration settlement terms; missing this date could unravel litigation truce reflecting negatively on execution credibility [S2][S7].

- Post-Offering Period: Announcement of prospective acquisition targets or tentative deal frameworks vital for restoring investor confidence absent historic operating activity [S1].

- Future Quarterly/SEC Filings: Updates regarding progress against share issuance plans, PIPE financing arrangements coordinated via designated underwriters Chardan and D. Boral provide tangible markers of momentum [S2][S1].

- Governance Developments: Disclosure enhancements related to internal controls anticipated toward end-of-fiscal-year may signal readiness for scaling compliance post-Business Combination [S3].

Monitoring these developments will be essential to assess whether Aeon can transition from shell entity status into an active public operating franchise capable of generating sustainable shareholder value.

This analysis is intended solely for informational purposes presenting factual content based on publicly available SEC filings without any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments