BBB Foods Expands Rapidly in Mexican Discount Grocery but Faces Liquidity and Profitability Challenges

Tiendas 3B’s aggressive store growth drives revenue gains while operational costs pressure near-term earnings and liquidity.

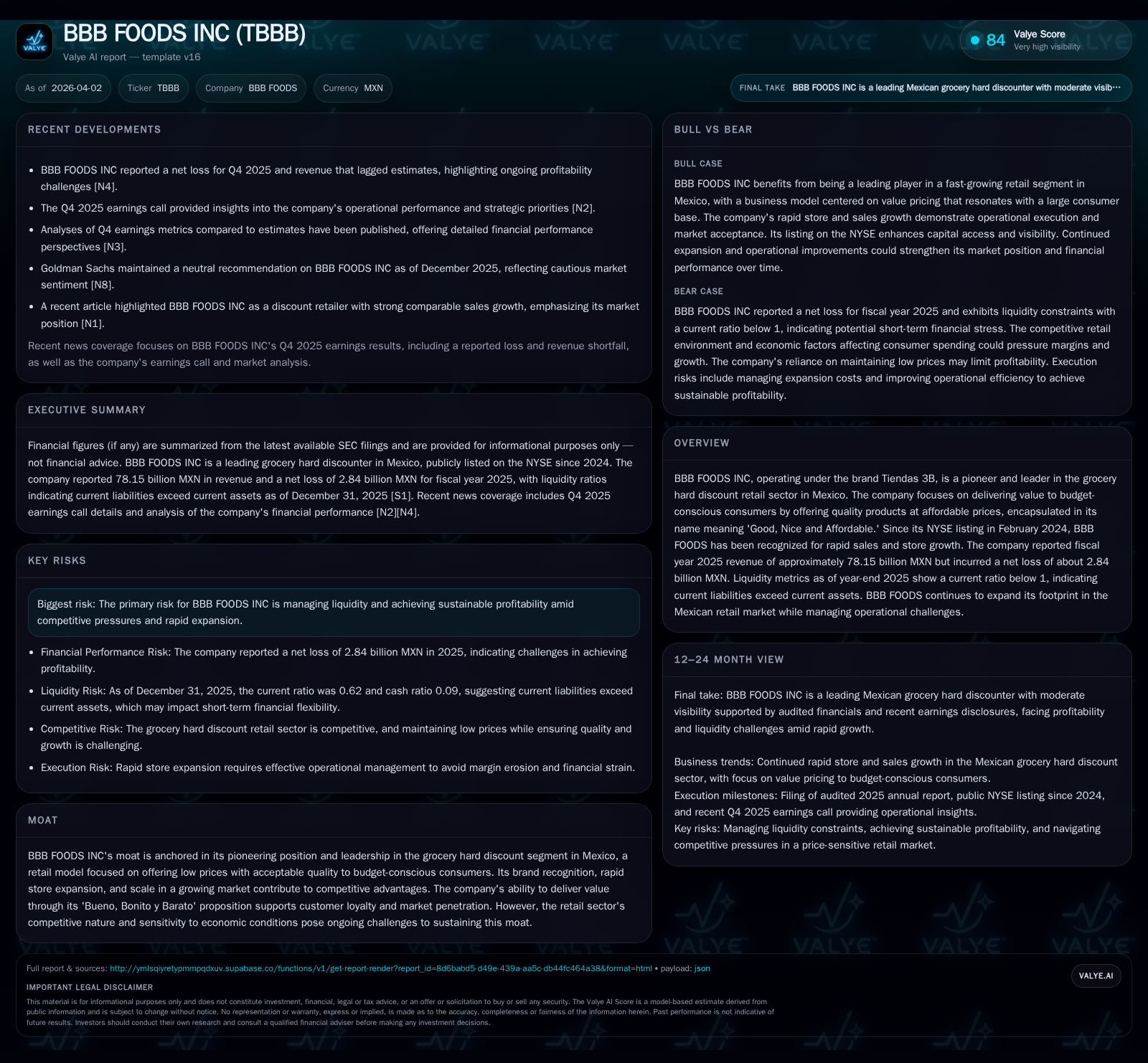

BBB Foods Inc (TBBB), operating the Tiendas 3B brand, is a leading grocery hard discount retailer in Mexico that achieved significant revenue growth of 36.1% in fiscal 2025, driven by an accelerated expansion rate of over 20% in store count. Despite scaling sales to over 78 billion MXN, the company posted a net loss of nearly 2.84 billion MXN due to elevated financial costs, share-based compensation expenses, and expansion-related investments. Liquidity remains tight with a current ratio of just 0.62. BBB Foods’ decentralized regional operating model facilitates rapid rollout but managing profitability and cash flow amid competitive pressures poses an ongoing risk.

Company Overview

BBB Foods Inc (ticker: TBBB), trading as Tiendas 3B since its NYSE listing in February 2024, stands as a pioneering entity in Mexico’s grocery hard discount sector—a retail segment focused on low-priced items without sacrificing essential quality for budget-savvy consumers. The name "Tiendas 3B" stems from the Mexican phrase “Bueno, Bonito y Barato” translating to "Good, Nice and Affordable," encapsulating their value proposition aimed at middle- and lower-income Mexican households seeking cost-effective grocery options [S2].

Past Growth and Historical Performance

Since its inception, BBB Foods accelerated its footprint expansion aggressively; in fiscal year (FY) 2025 alone, it opened nearly 600 net new stores—representing a remarkable ~21% increase compared to FY2024 store count—totaling over 3,346 outlets by year-end [S3]. This expansion is supported by four newly added distribution centers throughout the year, enhancing logistics efficiency within its decentralized regional operating model.

The top-line benefited strongly from this footprint growth combined with same-store sales growth rates, which reached approximately +16.6% in the fourth quarter of 2025 alone [S3]. Consequently, FY2025 revenue surged by +36.1% YoY to around Ps.78.15 billion (Mexican Pesos) [F1].

However, this robust revenue growth masked underlying profitability pressures. Despite prior years showing some net profitability (e.g., positive Ps.334 million in FY2024), fiscal year 2025 culminated in a significant net loss nearing Ps.-2.84 billion [F1]. Non-cash expenses related to share-based payments ballooned dramatically (noted over Ps.2.9 billion in Q4 alone per filings), alongside rising lease liabilities and financial costs linked to store expansions [S3][S8]. EBITDA contracted sharply to roughly Ps.1.22 billion comprising only a ~1.6% margin compared with prior better margins close to 5%, underscoring margin erosion linked mainly to operating leverage dilution and elevated expenses [F1][S13].

Summary Table: Key Financials (Ps thousands)

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 78.2 | -2.8 | +36.1% | -949.1% |

| 2024 | 57.4 | 0.3 | +30.3% | +209.2% |

| 2023 | 44.1 | -0.3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -68.8 |

| 2024 | 8.3 |

| 2023 | 6.6 |

Source: SEC companyfacts cache [F1].

Net income turned negative again in FY25 after a brief profitable phase; liquidity remains stretched given growing current liabilities outpacing current assets.

Operating Model and Strategic Positioning

BBB Foods employs a decentralized organizational structure optimized for scalability across Mexico’s diverse regions—each region comprises roughly up to five hundred stores supported by one distribution center with autonomous functional teams including human resources and real estate divisions tasked with local market responsiveness while maintaining centralized guidelines on product quality and operational compliance [S1]. The retail model emphasizes simplicity: limited SKUs concentrating on fast-moving consumer goods that appeal broadly within budget constraints.

This regional model supports rapid rollout while controlling logistical complexity—a notable competitive advantage enabling BBB Foods to maintain lean operations despite rapid geographic spread.

Future Growth Prospects

Going forward growth drivers reside primarily in continued store openings with management targeting upwards of several hundred new units per annum alongside potential expansion into less penetrated regions [S3]. Same-store sales momentum is expected to support compounding sales uplift as brand penetration deepens.

However downside risks are material: the retail discount segment remains intensely competitive with players competing on price and convenience amid macroeconomic volatility that could affect consumer spending patterns notably among lower-income groups [S1]. Currency fluctuations remain a concern given USD holdings from IPO proceeds translate variably into Pesos impacting reported cash balances [S9]. Rising interest rates or tightening credit terms could exacerbate financial pressure considering significant lease liabilities booked as long-term debt equivalents leveraging off balance sheet capital.

Forecasts and Key Milestones

While explicit forward guidance is not disclosed beyond standard language indicating plans for accelerated store rollout balanced by discipline over unit economics [N1], investors should monitor quarterly updates on:

- New store openings pace relative to targets

- Trajectory of same-store sales growth signaling organic demand resilience

- EBITDA margin progression reflecting cost controls on lease payments and share-based compensation impact

- Liquidity measures especially shifts in current ratio and cash burn profile amid investment cycle completion

- Any plans for refinancing or restructuring lease/debt profiles [S3]

Returns & Capital Allocation

BBB Foods carries a heavily leveraged balance sheet primarily underpinned by lease liabilities exceeding Ps.10 billion complemented by short-term borrowings approaching Ps.2 billion at year-end FY25 [F1][S12]. Capital expenditures are substantial given continuous store openings with capex outflows surpassing Ps.3.5 billion annually recently [S9].

Despite rapid equity build-up post IPO (capital stock nearing Ps.9.3 billion), cumulative losses have eroded retained earnings resulting in modest total equity above Ps.4 billion only post-IPO infusion [F1]. There are no declared dividends or buybacks reflecting management preference for reinvestment during hyper-growth phase plus balancing working capital needs [S22][S25].

Cash flow from operations improved sequentially through FY25 but remains pressured after investing activities; effective working capital management will be critical going forward particularly inventory turns and supplier liabilities optimization [S9][S16].

Risk Factors Summary

The company's moat arises from first-mover advantage within Mexico's hard-discount grocery format coupled with brand awareness bolstered by affordability appeal . Yet risks predominantly stem from:

- Managing liquidity under rapid physical expansion without compromising operational flexibility [S4]

- Sustaining profitability given rising operational costs including labor inflation and rental escalation [S13]

- Foreign exchange exposure linked to USD cash reserves impacting reported liquidity [S9]

- Competitive pricing environment possibly compressing margins over medium term [S1]

- Regulatory or macroeconomic shocks affecting consumer purchasing power within key demographics [S1]

Conclusion

BBB Foods has demonstrated notable prowess at scaling Mexico's discount grocery landscape with robust revenue growth fueled by aggressive store network expansion and solid same-store sales gains evident through FY25's performance metrics [F1][S3]. However turning scale into sustainable profitability remains elusive so far due primarily to elevated share-based compensation charges particular to post-IPO incentive plans plus financial burden stemming from pronounced lease liabilities coinciding with market expansions.

Liquidity stands as a focal challenge with a current ratio well below unity signifying short-term obligations exceed liquid assets—a typical feature during capex-intensive phases but one necessitating close monitoring [F1]. Management’s decentralized operating framework aids scalable rollout but navigating competitive pressures while improving profitability will require continued execution discipline alongside potentially strategic financial restructuring.

Key performance indicators such as EBITDA margin recovery trajectories alongside cash flow stabilization will be essential markers of successful transition toward durable earnings power amidst rapidly evolving Mexican grocery retail dynamics.

This analysis is based solely on information publicly available as of early April 2026 including BBB Foods’ SEC filings and recent earnings releases/articles referenced herein; it does not constitute investment advice or a recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments