Tiendas 3B Achieves Impressive Expansion But Faces Mounting Financial and Legal Risks

BBB Foods' Tiendas 3B sustains rapid store growth and strong sales momentum while managing tightening liquidity and legal uncertainties.

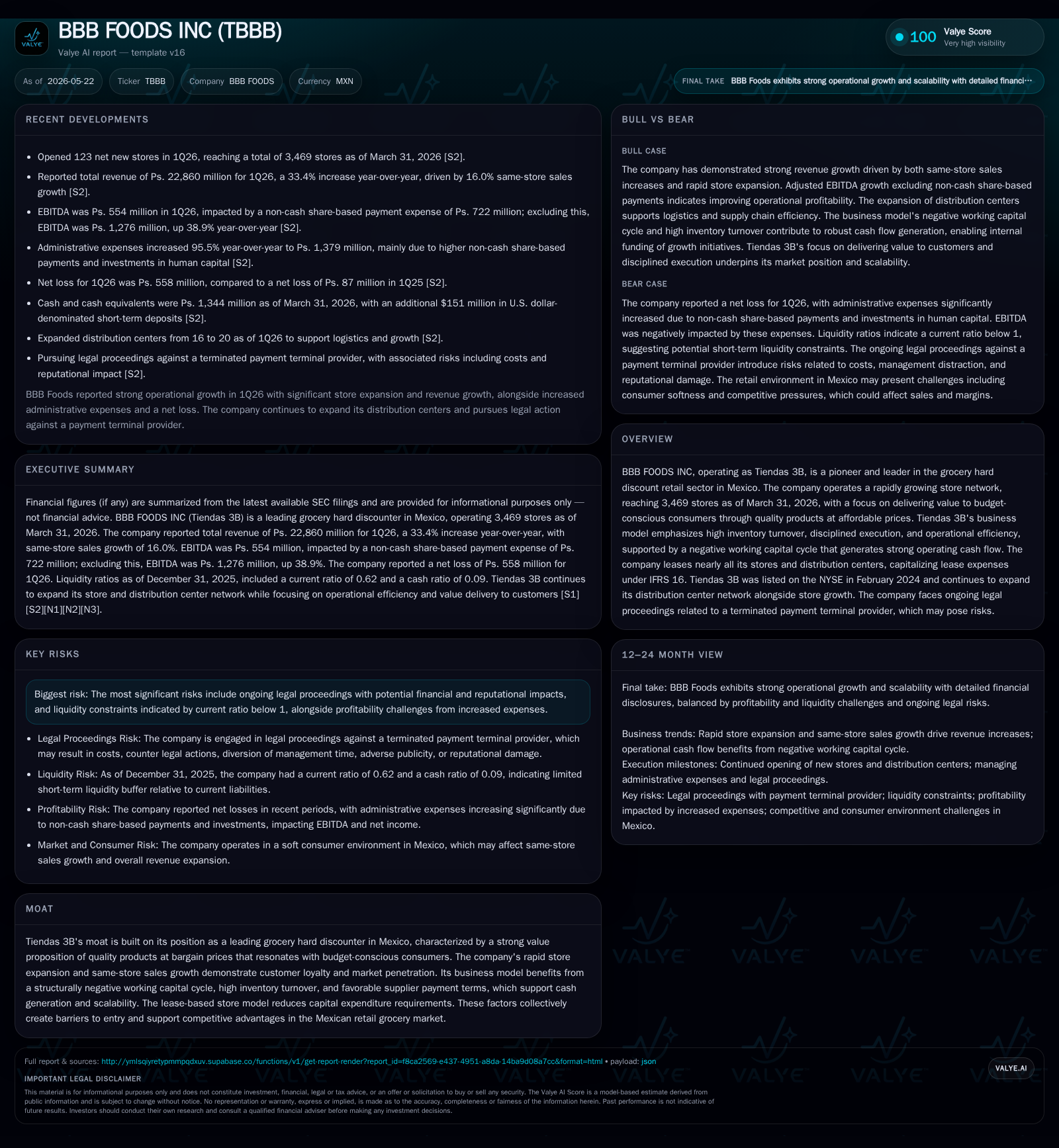

In the first quarter of 2026, BBB Foods Inc. (Tiendas 3B) expanded its store network to 3,469 locations, driven by a 16% same-store sales increase and 33.4% revenue growth. The company’s hard discount grocery model continues to resonate strongly with price-sensitive Mexican consumers, supported by operational efficiencies such as a negative working capital cycle and a capital-light lease strategy. However, rising financial costs primarily from lease liabilities and ongoing litigation related to terminated payment terminal contracts represent material risks to profitability and liquidity. Monitoring execution on store expansion, margin recovery post-share-based compensation impact, and resolution of legal matters will be critical in the near term.

Latest Quarterly Operating Update: Rapid Store Expansion and Sales Gains

BBB Foods Inc. kicked off 2026 with strong momentum, opening 123 net new stores in the first quarter to reach a network of 3,469 units as of March 31, 2026 [S2]. This marks continuation of an aggressive rollout strategy that positions Tiendas 3B among the fastest-growing retailers worldwide. Despite a challenging macroeconomic environment characterized by soft consumer demand in Mexico, Tiendas 3B achieved impressive same-store sales (SSS) growth of 16%, underscoring the appeal of its value-driven product offering.

Revenue rose to Ps. 22.86 billion in Q1 2026—a substantial 33.4% increase over the prior year—propelled by both network expansion and enhanced sales productivity in existing stores [S2]. Adjusted EBITDA excluding non-cash share-based payment expenses surged by nearly 39% to Ps. 1.276 billion, although reported EBITDA was compressed to Ps. 554 million reflecting significant equity compensation charges [S2]. This performance highlights solid operational execution amid margin headwinds.

Operating cash flow benefits from the company's structurally negative working capital pattern remained robust; net cash from operations increased markedly to Ps. 1.961 billion in Q1 from Ps. 1.195 billion a year earlier, reflecting effective management of inventory relative to payables [S2]

Business Model and Value-Focused Product Offering Driving Customer Loyalty

Tiendas 3B’s core business model centers on hard discount grocery retailing tailored to budget-conscious Mexican consumers seeking "Bueno, Bonito y Barato"—good quality products at bargain prices [S1], [S2]. The model's success rests on delivering irresistible value through a curated product assortment with heavy emphasis on private label goods, which accounted for over half of merchandise sales in recent periods [S1]. This appeals strongly in Mexico’s value-seeking retail landscape.

The company operates an asset-light model primarily utilizing leased stores and distribution centers under IFRS 16’s capitalization framework, which keeps upfront capital expenditures moderate while enabling rapid scale-up [S1], [S2]. Inventory turnover is high relative to supplier payment terms; this creates an inherently negative working capital cycle which not only supports liquidity but also funds ongoing expansion internally without reliance on external debt [S2], [S1].

Customer loyalty is bolstered by consistency in competitive pricing overseen by a dedicated Product and Pricing Committee comprising senior executives focused on product quality control, innovation, and pricing strategies that ensure relevancy in the target market segment [S1]

Industry Positioning: Leader in Mexico’s Grocery Hard Discount Segment

BBB Foods has established itself as a pioneer and front-runner within Mexico's grocery hard discount sector, which is still evolving but growing rapidly due to demographic trends favoring affordable retail formats [S1], [S2]. The company benefits from being among the first movers with deep local market understanding and broad geographic coverage via decentralized regional operations.

Its scale advantage enables efficient procurement while decentralization empowers quick decision-making across approximately eighteen logistical regions, each led by regional directors overseeing up to 200 stores alongside dedicated distribution centers [S1]. This nimble organizational structure lowers overheads relative to peers relying on centralized bureaucracy and enhances responsiveness to local competitive dynamics.

While direct peer financial data remains limited from disclosures, Tiendas 3B’s rapid store openings—averaging over one hundred per quarter recently—and sustained SSS improvements suggest meaningful pricing power and customer stickiness against traditional grocery chains or newer format entrants.

Operational Efficiencies Anchored by Negative Working Capital Dynamics

Operational effectiveness stems largely from prudent working capital management where inventory days remain tightly controlled against extended payables days provided by suppliers [S2], [S1]. This dynamic allows Tiendas 3B not only to convert sales into cash swiftly but also deploy internally generated funds directly toward retail rollout and logistics investments without diluting returns through external financing.

Logistics hubs aligned regionally enable streamlined inbound replenishment supporting high SKU availability despite low unit price points—a key challenge in discount retailing.

The leased property strategy offers flexibility crucial for fast growth while minimizing fixed asset depreciation burdens; right-of-use assets under IFRS accounting do elevate lease-related expenses technically but mitigate traditional capital-intensive risk profiles [S1], [S2].

Growth Drivers: Store Network Scale, Same-Store Sales Momentum, and Logistics Expansion

Beyond sheer store count increases (123 net new stores opened in Q1 alone), sustained strong SSS uplift (+16% in Q1) reflects successful consumer engagement strategies characterized by expanding basket size (more SKUs per transaction), frequent purchases, and consistent value messaging supported by disciplined pricing committees controlling promotions [S2], [N1].

Geographic footprint gains combined with logistical scale-up—evidenced by increasing distribution center counts—improve supply chain resiliency while reducing unit fulfillment costs which should yield operational leverage as maturity approaches across newer store cohorts [S1], [S2]. Older stores maintain SSS growth well above inflation indicating structural demand rather than temporary cyclical spikes.

Human capital investment aimed at strengthening management capabilities at district/zone levels supports scalability of operations alongside automation efforts aimed at inventory control precision might further lift margins once fixed cost absorption improves.

Key Risks: Liquidity Constraints, Legal Proceedings, and Competitive Headwinds

Financially, BBB Foods faces nontrivial challenges:

- The current ratio stood at a lowly sub-1 level of approximately 0.62 as of December 2025 end [F1], signaling potential short-term liquidity pressure despite ongoing positive operating cash flows.

- Rising financial costs saw a sharp increase (+43.6% YoY) primarily driven by heightened interest expenses linked to expanded lease liabilities necessitated by accelerated store/buildout activity rather than traditional borrowings; this weighs heavily on profitability metrics currently [S2].

- Unresolved litigation surrounding the terminated relationship with a payment terminal provider which entailed writing off receivables of Ps.230 million plus ongoing legal expenses pose reputational risks alongside possible financial contingencies that could affect earnings continuity or raise provisions if adverse judgments occur [S11], [S1].

Further competition intensification or macroeconomic slowdowns affecting low-income consumer spending patterns would also pressure margins or slow expansion pace despite favorable structural drivers.

Near-Term Catalysts and What to Watch Next

Key near-term milestones include:

- Monthly or quarterly updates on same-store sales trends will reveal whether recent gains are sustainable post-pandemic recovery phase or influenced by transitory factors.

- Monitoring total store openings per quarter will evidence if aggressive expansion can be maintained without diluting existing store profitability or overextending regional management bandwidth.

- Legal resolution progress pertaining to the payment terminal dispute could materially impact reported earnings profiles depending on indemnity outcomes.

- Commentary around margin improvement trajectories following normalization of share-based payment impacts will shed light on underlying operating leverage.

- Liquidity metrics including changes in current ratio or working capital conversion efficiency will be key indicators whether funding pressures intensify needing external solutions.

Financial Overview: Liquidity Status and Expense Dynamics

For Q1 2026, total revenues reached Ps.22.86 billion representing a strong growth signal while net reported EBITDA dropped to Ps.554 million from prior year levels due largely to non-cash share-based compensation charges totaling Ps.722 million [S2]. Adjusted EBITDA rose significantly showing core operating health.

Operating cash flows remain positive at nearly Ps.2 billion for the quarter underpinning ongoing internal funding capability though this is partially offset by increased financial costs on lease liabilities which rose over 40% YoY reflecting expanded contractual obligations accompanying rapid footprint growth [S2]

Balance sheet data as of December 31, 2025 indicate cash plus equivalents totaled roughly Ps.1.43 billion while current assets measured Ps.9.73 billion against current liabilities of approximately Ps.15.6 billion yielding a concerning current ratio near 0.62—highlighting the importance of continued tight working capital management amidst growth ambitions alongside capital markets access or refinancing preparedness if macro conditions tighten further [F1]

While BBB Foods maintains gross margins around 16%, compression from administrative expenses linked partly to its public company status expense run-rate including share-based compensation dampens net profitability despite strong topline growth and favorable unit economics.

This analysis is based exclusively on publicly available SEC filings dated through May 6, 2026 ([S2], [S3]), supplemented with official news transcripts ([N1]-[N3]) and structured financial data from companyfacts ([F1]). It does not constitute investment advice but aims to provide an evidence-supported assessment of BBB Foods’ business dynamics amid evolving operational challenges.

Financial position in context

As of 2025-12-31, companyfacts shows 1,427,248,000 MXN in cash and equivalents [F1]. Current assets of 9,726,148,000 MXN and current liabilities of 15,602,290,000 MXN imply a current ratio near 0.62x for 2025-12-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments