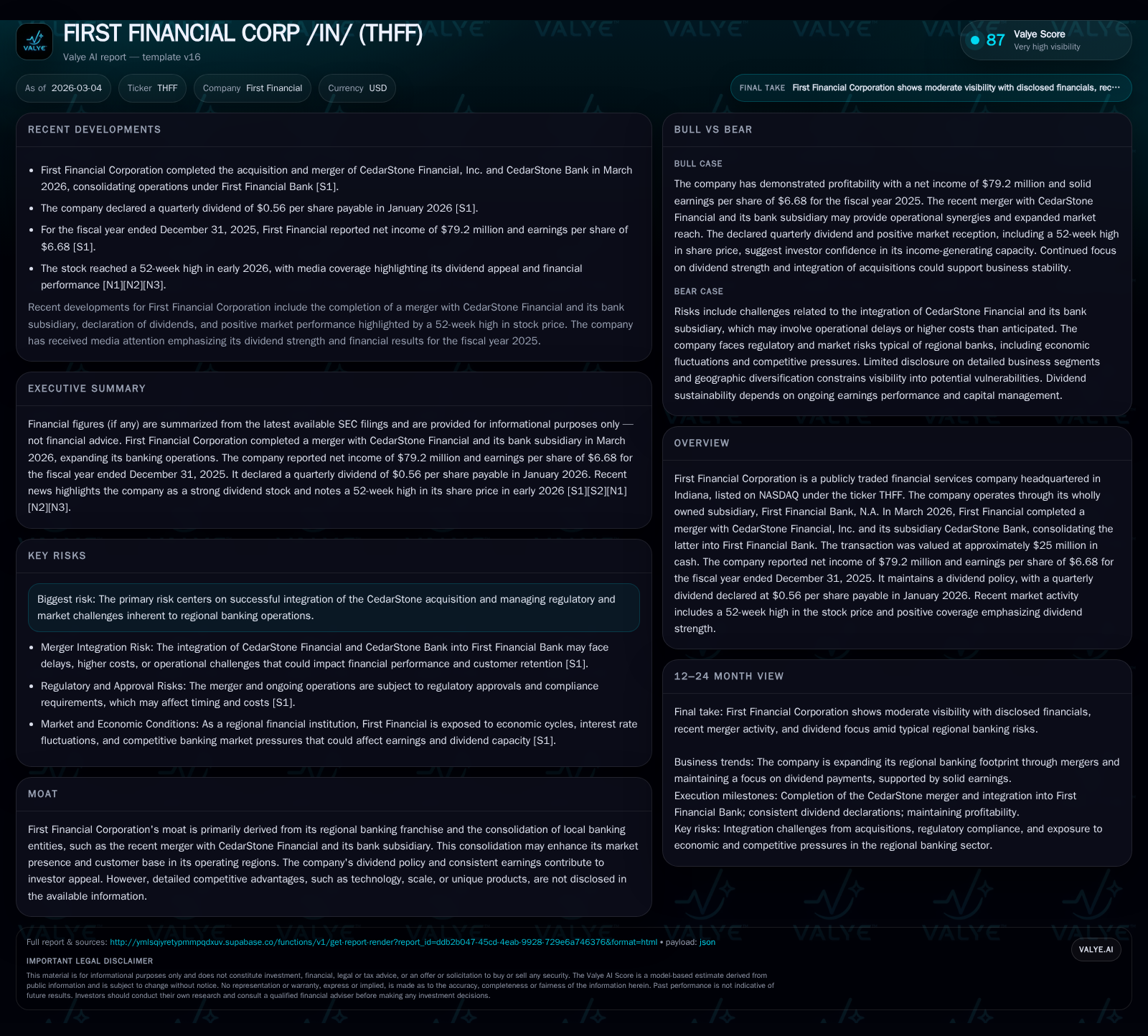

First Financial Corp’s Strategic Expansion and Dividend Strength Drive 2025 Performance

A merger with CedarStone and disciplined capital returns fueled First Financial’s robust net income growth and operational cash flow in 2025.

First Financial Corporation achieved a notable 67.5% surge in net income in fiscal 2025, driven by organic operations and completed just after year-end the $25 million acquisition of CedarStone Financial. The merger expands its regional banking footprint and customer base, reinforcing its competitive positioning. Alongside growth ambitions, the company maintained a strong dividend policy with quarterly payouts and modest share repurchases, reflecting disciplined capital allocation amid integration risks typical for regional consolidations.

2021-2025: Profitability and Cash Flow Trajectory Amid Evolving Regional Footprint

First Financial Corporation demonstrated a clear trajectory of financial improvement expanding sharply in profitability and cash flow by the close of 2025. Net income advanced from $47.3 million in 2024 to $79.2 million in 2025—a striking 67.5% increase reflecting both organic strength and contributions tied to strategic initiatives [F1]. Operating cash flow grew concomitantly by nearly half (49.8%), reaching $90.4 million, underscoring efficient core operations within a regional banking framework prone to stable deposit bases.

Capital expenditures followed a more conservative path, dipping from approximately $6.1 million in the prior year to about $3.98 million in 2025 (-34.8%), indicative of controlled reinvestment while maintaining branch infrastructure or technology platforms relevant to local banking demands [F1]. Total shareholder equity ended the year at approximately $651 million after rising through the period, fostering an approximate return on equity (ROE) near 12.2%, which signals solid value generation relative to invested capital [F1].

Dividends paid out rose moderately to $24.2 million in alignment with expanding earnings; share repurchases were notably restrained at around $0.8 million after spikes earlier in the period (especially FY2022) [F1]. This balance suggests a capital return approach favoring sustainable dividends complemented by opportunistic buybacks.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 79 | 90 | 4 | |

| 2023 | 47 | 60 | 6 | -33.5% |

| 2022 | 71 | 79 | 1 | +34.2% |

| 2021 | 53 | 55 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 24 | 1 | 86 |

| 2023 | 21 | 0 | 54 |

| 2022 | 14 | 28 | 77 |

| 2021 | 14 | 42 | 51 |

Source: SEC companyfacts cache [F1].

*Note: FY2024 figures inferred based on YoY calculations presented for FY2025 [F1].

Overall, this financial profile aligns with a regional bank balancing steady organic growth and strategic expansion ahead of a major merger.

Merger Impact: Unlocking Scale and Market Position through CedarStone Acquisition

In early March 2026, First Financial Corporation consummated an all-cash acquisition of CedarStone Financial, Inc., including its wholly owned subsidiary CedarStone Bank, valued at approximately $25 million [N9][S3]. This deal expands First Financial’s regional footprint into Tennessee markets beyond its Indiana base, broadening its customer base and lending capabilities.

The merger agreement was approved unanimously by both boards and included comprehensive covenants ensuring operational continuity until closing alongside customary regulatory approvals [S16][S18]. Integration risks flagged relate primarily to delays or complexities inherent in merging IT systems, aligning corporate cultures, employee retention pressures, and realizing targeted cost synergies [S4][S6][S8]. Such issues are endemic to regional banking consolidations where overlapping branch networks and product offerings must be rationalized without alienating core clients.

This acquisition enhances First Financial’s market presence by consolidating two community banking franchises under one roof —a classic play for scale efficiencies coupled with incremental cross-selling opportunities that can improve net interest margins over time if successfully executed . The immediate post-merger phase will likely focus heavily on regulatory compliance adherence given enhanced scrutiny on bank consolidations nationally.

Hence, while the transaction marks an important milestone fueling recent net income gains, practical integration challenges underscore a cautious optimism toward sustainable long-term uplift.

Analyzing Dividend Policy and Shareholder Returns in a Competitive Banking Environment

Maintaining an attractive dividend has been central to First Financial’s investor appeal alongside its recent profit upswing [N5][N8]. The company declared a quarterly dividend of $0.56 per share payable starting January 15, 2026—consistent with its payout pattern expanding in step with earnings improvements [S20].

Given the nearly doubling of net income in FY2025 relative to prior years but dividends rising more moderately suggests a sustainable payout ratio targeting long-term financial health while preserving flexibility for reinvestment or acquisitions.

Meanwhile, share repurchases have been markedly subdued post-FY2022 peaks—with $0.8 million spent on buybacks in FY2025 signaling prudent capital discipline rather than aggressive stock reduction programs [F1]. This measured repurchase activity complements dividends as part of a balanced capital return strategy tailored to maximize shareholder yield without impairing liquidity buffers essential for regulatory capital adequacy.

In sum, First Financial manages its return policies thoughtfully amid competitive pressures faced by regional banks contending with rising deposit costs and margin compression.

Capital Structure, Liquidity, and Risk Management Following Recent Expansion

As of December 31, 2025, First Financial reported total shareholder equity surpassing $650 million—a robust buffer that supports expansion efforts including the completed CedarStone acquisition and potential further consolidation moves [F1]. Available liquidity profiles reflect solid cash balances supplemented by access to debt markets under prudent terms [S8–S14].

Regulatory filings emphasize continuing risk factors centered on satisfactory integration outcomes post-merger such as meeting timelines, managing unexpected liabilities or litigation exposures tied to the transaction [S4][S6]. Moreover, compliance environments demand heightened vigilance as merged entities face uniform standards across states impacting loan underwriting guidelines or capital adequacy rules.

Notably absent are any indications of material leverage stress or credit deterioration—implying cautious asset base management aligning with conventional community bank risk appetites while navigating increased competition from fintech entrants that pressure fee-based revenues further tightening margins.

This balance sheet strength undergirds planned dividend maintenance even as growth ambitions press upward.

Growth Prospects: Integration Challenges and Opportunities Ahead

Forward-looking statements made around the merger announcement underscore expectations for timely realization of synergistic benefits encompassing expanded deposit networks and revenue diversification [N9][S3][S8].

Potential upside is found especially through cross-selling loan products across newly joined customer bases enhancing fee income streams beyond traditional net interest margin reliance typical for community banks operating within concentrated geographies.

Conversely, timing risks persist given possible delays tied to technology platform harmonization or staff retention fallout which could weigh temporarily on operating expenses or credit quality metrics during transition phases.

Overall outlook reflects guarded optimism grounded on realistic execution timelines informed by historical precedents within the sector where integrations often span multiple quarters before achieving planned efficiency gains fully.

Financial Milestones to Watch: What Could Shape THFF’s 2026 Outcome

Absent explicit forward guidance from First Financial itself [N9], analysts and observers should monitor quarterly updates focusing on loan portfolio health—specifically delinquencies post-integration—as well as noninterest income trajectories which may indicate successful cross-selling progress relative to standalone periods [N2][N7].

Expense synergy realization pace will also serve as a key barometer given its direct impact on operating leverage that can influence future net margin expansion or contraction.

External developments affecting interest rate environments regionally remain pertinent due to their direct influence on lending margins within middle-market banking niches served by THFF.

These operational milestones comprise an essential watchlist furnishing insight into whether anticipated merger advantages translate into sustainable earnings growth beyond initial headline figures.

Sector Insights: Common Regional Bank Considerations on Consolidation and Regulation

Regional banks engaging in consolidation frequently wrestle with challenges ranging from integrating disparate IT systems to maintaining customer loyalty amid changing brand identities—a phenomenon described as market fragmentation reversal yet fraught with customer retention hazards as rationalization proceeds . Regulatory capital constraints heighten post-merger given combined entity asset pools typically requiring recalibrated risk-weighted asset assessments pushing banks toward bolstered liquidity buffers.

Branch network rationalization is almost inevitable leading not only to cost savings but also contentious local political dynamics impacting customer sentiment.

In this context First Financial’s careful handling of CedarStone absorption reflects standard industry prudence accentuated by explicit forward-looking cautionary language within filings reaffirming inherent uncertainties common across similar deals nationally [S4][S6].

Ultimately successful consolidation demands harmonizing growth aspirations with rigorous risk management frameworks capable of adapting quickly amid evolving regulatory landscapes shaping American regional banking models today.

This analysis synthesizes publicly available data from company financial reports and SEC filings up to March 4, 2026 along with corroborating news sources without extrapolating beyond disclosed facts or speculating on unreported metrics or future outcomes beyond evidenced statements.

It is intended solely for informational purposes without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments