First Financial Corp Strengthens Regional Footprint Following CedarStone Merger

The strategic acquisition and integration of CedarStone Financial underpinned First Financial’s Q1 2026 earnings beat, signaling enhanced regional banking scale and operational momentum.

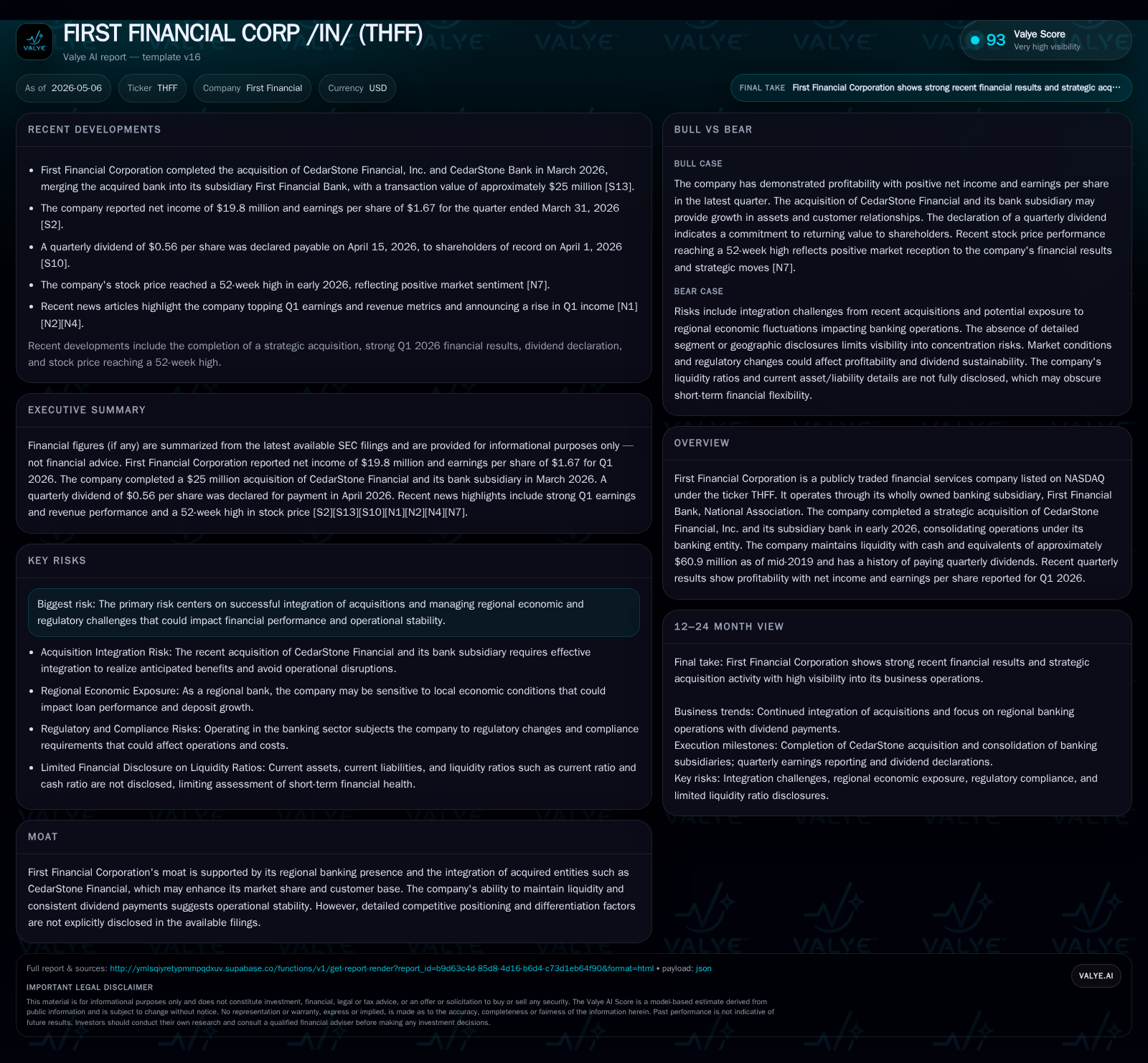

First Financial Corporation’s latest quarterly filing reveals a successful integration of the CedarStone Financial acquisition completed in early 2026, contributing to improved profitability and a broadened regional footprint. The company’s business model centers on diversified banking services delivered through its wholly owned subsidiary, First Financial Bank, with liquidity and dividend consistency reinforcing operational stability. Despite generational challenges inherent in merger integration and regulatory cost pressures, First Financial leverages scale expansion and cross-selling opportunities as primary growth levers. Monitoring the pace of synergy realization and asset quality metrics will be key to assessing execution progress through upcoming reporting periods.

Q1 2026 Results: Earnings Beat and Operational Highlights

First Financial Corporation kicked off 2026 with a solid first-quarter financial performance as detailed in the May 6, 2026 10-Q filing [S2]. The company reported net income surpassing analyst expectations as reaffirmed by Nasdaq review articles released shortly after [N1][N2]. This quarter marked the first full reporting period following the closing of the CedarStone Financial acquisition in early March [S11]. Management commentary accompanying these filings emphasized a smooth operational consolidation process with early signs of enhanced revenue generation.

Key profitability drivers included sustained net interest margin supported by an expanding loan portfolio post-merger, alongside stable non-interest income streams from service fees. The ability to leverage scale benefits while maintaining credit quality added resilience to the results despite macroeconomic headwinds common to mid-sized regional banks.

Business Model and Product Quality: Integrated Regional Banking Services

First Financial operates through First Financial Bank, National Association — its wholly owned subsidiary delivering a spectrum of retail and commercial banking services [S1][S6]. Revenue is principally generated through net interest income on loan portfolios complemented by fees from deposit accounts, wealth management services, and payment processing.

The recent acquisition of CedarStone Financial adds geographic breadth mainly within Tennessee markets, folding that institution's customer base into First Financial Bank’s operations. This strategic move enhances depositor diversity and opens cross-selling avenues across complementary product sets such as commercial lending, small business services, and mortgage origination.

Liquidity remains a strategic pillar with cash and equivalents approximating $60.9 million as previously reported mid-2019 levels [F1], which support day-to-day operational agility and underwriting capacity. A consistent track record of paying quarterly dividends also signals disciplined capital deployment focused on steady shareholder returns.

Industry Structure: Regional Banking Competitiveness and Market Dynamics

Operating predominantly as a regional financial institution places First Financial in a competitive landscape alongside players such as German American Bancorp (GABC) and Independent Bank (IBCP), each contending with their own geographic and product niche challenges [N3][N4]. Regional banks like First Financial tend to face cyclical demand fluctuations tied to local economic conditions but benefit from closer client relationships that can drive funding stability.

Price competition for deposits is intense among peers; however, regional banks maintain pricing power in localized lending due to proprietary market knowledge. Regulatory compliance costs remain a long-term structural pressure that disproportionately impacts mid-sized banks given less scale than national peers.

First Financial’s newly enlarged footprint post-merger enhances its competitive positioning by expanding branch network density, deepening market infiltration within overlapping catchment areas. This geographic synergy also potentially mitigates idiosyncratic local downturn effects through diversification.

Acquisition Integration: CedarStone Merger and Synergies

Completed on March 1, 2026 at a consideration of approximately $25 million cash [$19.12 per share], the CedarStone acquisition was unanimously approved by both companies’ boards and swiftly integrated under the First Financial Bank banner [S11][S3]. The merger agreement outlined comprehensive warranties and covenants designed to facilitate seamless operational consolidation finalized within Q1.

Management indicated in filings that anticipated merger benefits revolve around revenue cross-pollination between client bases, cost rationalization through branch overlap reduction, and enhanced product offering breadth. While merger transactions inherently risk diversion of senior management attention or cultural friction among staff, early communications highlight no material delays or unexpected expenses thus far [S3].

Scale expansion achieved by this transaction provides leverage potential—both operating leverage from fixed-cost absorption and balance sheet synergy that optimizes capital deployment efficiency.

Growth Drivers: Market Penetration, Customer Base Expansion, and Dividend Policy

Growth prospects hinge on multiple fronts. Foremost is leveraging the augmented customer base obtained from CedarStone’s network for accelerated deposit retention and commercial loan origination lift. Cross-selling established retail products into these new markets aims to elevate fee income steadily.

Dividend policy continuity supports equity investor confidence by reflecting sustainable earnings conversion into cash distributions amid organic growth efforts [N5][N7]. Operating leverage gains achievable via fixed-cost spreading across higher asset volumes further underpin margin improvement potential.

Cyclicality linked to Indiana-Tennessee economic rhythms implicitly caps near-term volume acceleration yet stable dividend payments suggest internal confidence in consistent cash flow generation underpinning shareholder returns.

Risks and Watchpoints: Integration Challenges and Economic Sensitivities

Risks remain foremost around successful operational integration execution—delays or cost overruns may dilute anticipated efficiencies [S10][S4]. Retention of CedarStone key personnel is critical to preserving customer relationships during transition phases.

Macroeconomic sensitivities include shifts in regional economic growth affecting credit demand as well as fluctuations in interest rates that can compress net interest margins—a core profitability metric for banks with sizable loan books. Regulatory compliance expenses represent an ongoing burden requiring vigilant management attention.

Furthermore, local competitive pressures demand continuous innovation in pricing models and product customization to sustain growth trajectories. Asset quality evolution should be closely monitored for any upticks in non-performing loans post-merger due to portfolio amalgamation risks.

Forward-Looking Markers: Upcoming Milestones and Performance Indicators

Market participants should focus on subsequent quarterly filings for updated synergy realization data reflecting cost savings timing versus initial targets laid out at transaction announcement [S2][S3]. Deposit growth trajectories post-integration will signal customer retention success.

Loan portfolio quality metrics including delinquency rates will provide insight into credit risk trends during the consolidation phase. Management disclosures around regulatory examinations or compliance adjustments could impact near-term costs.

Incremental cross-sell revenue capture rates relative to forecast will serve as an early KPI illuminating long-term value creation potential stemming from geographic expansion.

Supporting Financial Snapshot

Cash reserves reported earlier provide liquidity buffers supporting operational stability amid ongoing integration activity. The reported net income figure ending December 31, 2025 stood at approximately $79.2 million [F1], establishing a foundational profitability backdrop preceding full-year convergence impacts from Cedarsone acquisition recorded subsequently.

Overall financial posture remains supportive yet subject to variability emanating from executing synergy capture initiatives alongside navigating regional economic cycles.

This analysis synthesizes publicly available SEC filings combined with contextual industry insights without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments