TTEC Holdings Confronts Profitability Challenges Despite Innovation in AI-Driven Customer Experience

The 2025 fiscal year saw TTEC Holdings deliver strong cash flow improvement amid mounting operational losses and intensifying market competition.

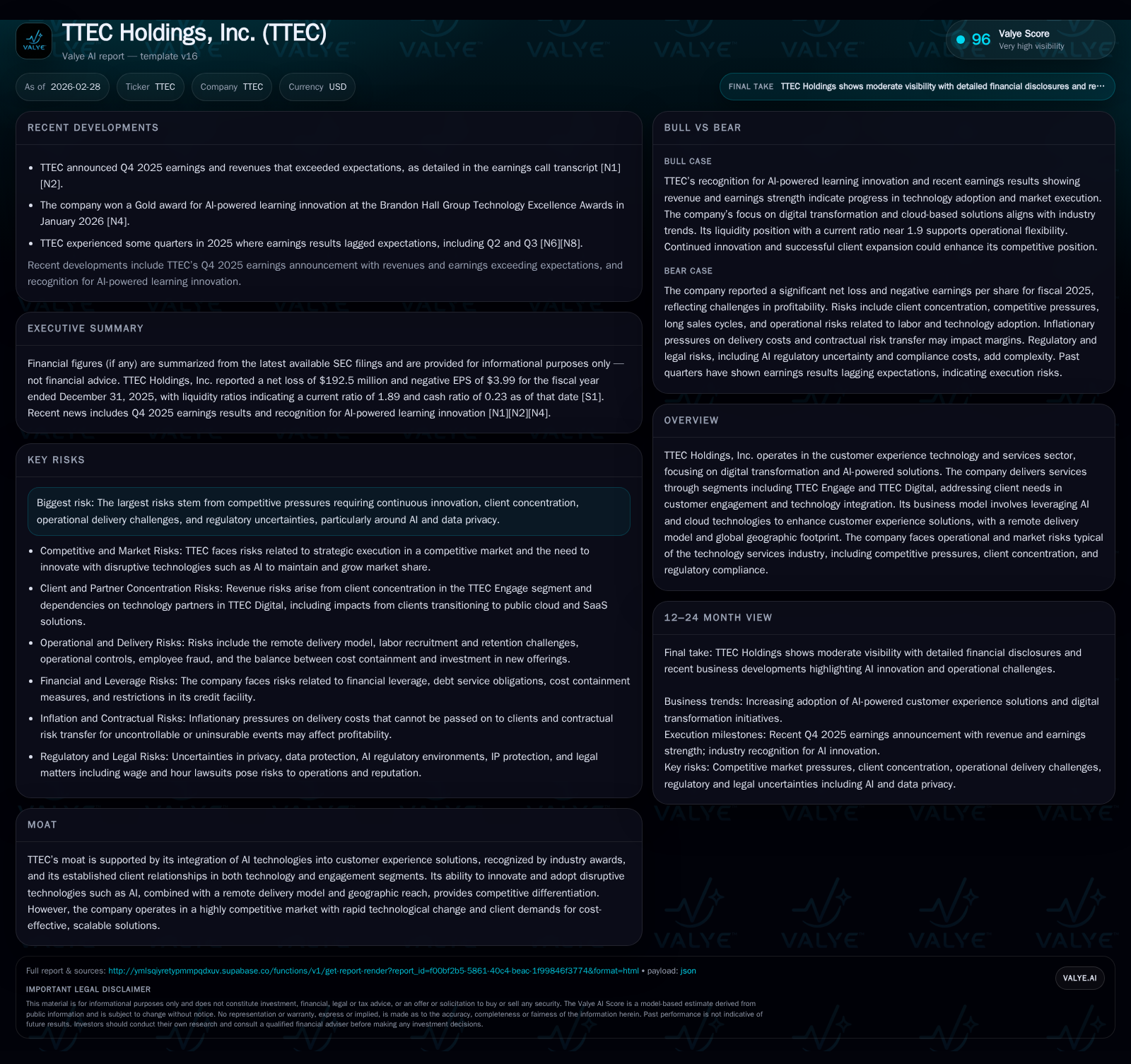

TTEC Holdings, Inc., a player in customer experience technology and services, reported continued top-line pressures and operating losses for 2025 despite notable advancements in AI integration. The company’s business model spans two key segments—TTEC Engage and TTEC Digital—with a global delivery footprint leveraging cloud and AI technologies. Financials reveal a sharp rebound in operating cash flow contrasted with persistent net losses, underscoring balancing acts between innovation investments and cost controls. Risks remain elevated from competitive dynamics, client concentration, regulatory scrutiny, and operational complexities inherent to its scale and technology transitions.

Business Overview and Market Positioning

TTEC Holdings, Inc. operates primarily within the customer experience technology and services sector. Its offering centers on digital transformation initiatives augmented by artificial intelligence, delivered through two main business units: TTEC Engage (customer engagement services) and TTEC Digital (technology solution integration). The firm combines AI-powered tools with cloud infrastructure to enhance end-client interactions.

A core competitive edge lies in its early adoption of AI into core customer experience frameworks—a focus that garnered industry recognition such as the Brandon Hall Group Technology Excellence Award for AI-Powered Learning Innovation in early 2026 [N4]. The ability to offer scalable remote service delivery across a global footprint adds further depth to its moat against competitors.

Historical Financial Performance

The financial summary over recent years shows substantial volatility primarily driven by strategic investments, restructuring charges, and market pressures. Revenue as per the latest annual filing rested around $419 million (historical data indexed up to fiscal year-end 2018) with operating income deteriorating sharply in 2024 and showing partial recovery in 2025 (though still negative). Net income showed a similar pattern of heavy impairment losses but with narrowing net loss margins recently.

Operating cash flow strength contrasts with accounting earnings losses—evidencing effective working capital management and focus on cash conversion even amid challenging revenue environments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -192 | 121 | -117 | 38 | +40.0% |

| 2024 | -321 | -59 | -174 | 45 | -3908.3% |

| 2023 | 8 | 145 | 118 | 68 | -91.8% |

| 2022 | 103 | 137 | 169 | 84 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 0 | 83 |

| 2024 | 3 | -104 |

| 2023 | 49 | 77 |

| 2022 | 48 | 53 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures from public filings are dated through prior periods; latest exact revenue data not updated post-2018 per available records [F1].

In detail:

- Operating income improved by approximately 32% in year-over-year comparison from declining losses sustained in early years to reduced operating deficits in FY25 [F1].

- Net loss reduced nearly by forty percent compared to FY24's significant hit [-$321M to -$192M] signaling some stabilization trends though still distant from profitability [F1].

- Cash flows improved dramatically (+305%) reflecting working capital focus amidst investment pullback [F1].

- Capital expenditures have been deliberately curtailed by ~15% as company recalibrates investments amid uncertain returns [F1].

- Dividend payments ceased entirely during FY25 after tapering distributions suggest discretionary capital reallocation [F1].

Key Growth Drivers and Constraints

Growth prospects stem from several vectors detailed by management commentary including:

- Expanding adoption of AI-enabled customer engagement platforms particularly within TTEC Engage segment's large enterprise client base.

- Scaling cloud-based SaaS implementations favored by TTEC Digital's emerging clientele adapting to public cloud service models.

- Leveraging remote workforce delivery efficiencies cutting overall costs while maintaining service continuity globally.

Constraints include:

- High client concentration risk within the engagement business where few large customers represent disproportionate revenue slices.

- Demand for continuous innovation increases R&D intensity forcing expense decisions balancing short-term profitability against long-term competitiveness.

- Operational challenges related to workforce recruitment/retention pressures at differential price points globally impacting margins.

- Regulatory uncertainty especially concerning AI regulation frameworks and data privacy laws that may impose compliance costs or restrict offerings noted prominently as risk factors across SEC filings [S4][S5][S10].

Outlook and Milestones to Watch

While explicit forward guidance is absent from filings or calls, several markers deserve attention:

- Execution success of new AI product rollouts designed to enhance service differentiation.

- Client acquisition/retention rates amid intensifying competition from larger IT services firms expanding their CX portfolios.

- Management commentary on contract durations reflecting lead time variability impacting near-term revenue visibility.

- Monitoring regulatory developments pertaining to AI governance which could remodel compliance landscapes abruptly.

Sector analysis suggests that the ongoing wave of digital CX modernization initiatives presents ample runway for firms capable of integrating robust analytics with automated solutions; however, scale advantages wielded by incumbents will keep pricing pressure persistent.

Returns Profile and Capital Allocation

Returns metrics underscore persistent profit recovery challenges:

- Approximate return on equity based on reported net income versus equity figures indicates elevated volatility due to negative net earnings despite equity base stability—roughly -190% ROE indicative of continuing losses but significant improvement vs prior year lows [F1].

Capital allocation has been conservative:

- Operating cash flows robust enough to comfortably cover capital expenditures yielding a free cash flow generation (~$83M) reinforcing balance sheet resilience without reliance on additional leverage [F1].

- No dividends distributed in latest fiscal implying prioritization towards deleveraging or reinvestment over shareholder payouts presently.[F1]

- No share buybacks recorded since at least the last reporting horizon suggesting capital preservation mindset amid uncertain earnings trajectory.[F1]

- Management appointments such as new Chief Accounting Officer reflect emphasis on strengthening governance amid transition phases [S20].

Liquidity remains satisfactory with current ratio near 1.9x evidencing sound short-term asset coverage relative to liabilities.[F1]

Risk Considerations

Risk disclosure is comprehensive noting:

- Market competition forcing rapid technological adoption cycles with potential risks of obsolescence.[S4][S5]

- Client concentration risk heightened specifically around TTEC Engage’s largest contracts creating revenue volatility exposure.[S2]

- Operational risks of delivering services remotely with consistent quality amidst labor cost inflation.[S6]

- Extensive regulatory uncertainty surrounding emerging AI laws globally complicating compliance regimes potentially inflating costs or limiting market access.[S9]

- Cybersecurity threats given dependency on third-party IT infrastructure and SaaS providers introduces non-trivial loss contingencies.[S8]

- Legal proceedings currently disclosed appear limited but could escalate depending on regulatory outcomes or contractual disputes.[S4]

Conclusion

TTEC Holdings resides at an inflection point balancing investments in innovative AI-driven customer experience technologies against operational inefficiencies that continue to weigh heavily on profitability metrics. While improving cash flows point to positive momentum on financial health fronts, recurring net losses highlight underlying structural challenges typical in high-investment tech services businesses transitioning through digital transformation phases.

Continued emphasis on leveraging AI as a differentiator coupled with disciplined capital management will be critical levers for future stability amidst ongoing sector competition intensification and regulatory evolution risks.

This report is based solely on information available through February 28, 2026, including public filings and verified news sources referenced herein, without provision of investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments