UNITED BANKSHARES' Expansion and Financial Shifts Driven by Piedmont Acquisition and Mortgage Channel Consolidation

United Bankshares expanded its regional footprint via acquisition and streamlined mortgage operations while maintaining capital strength and dividend growth.

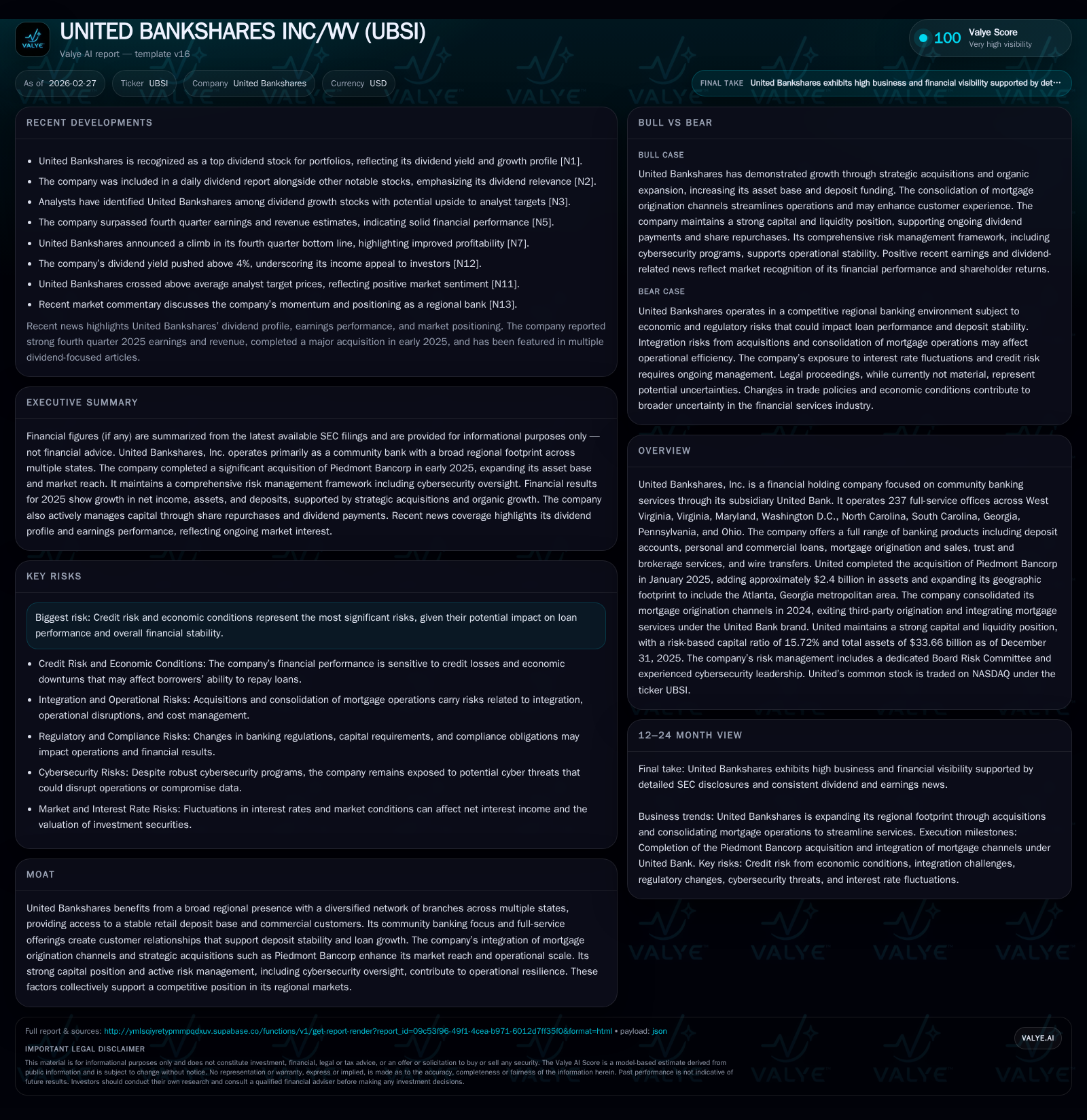

United Bankshares Inc. (UBSI) reported a significant asset and deposit base increase following the January 2025 acquisition of Piedmont Bancorp, adding $2.4 billion in assets and extending into the Atlanta metro market. The company consolidated its mortgage origination channels during 2024, exiting third-party origination and integrating under a single United Bank brand, aiming to streamline operations and enhance customer experience. Despite a YoY revenue decline in recent reported figures, UBSI achieved substantial net income growth supported by strong loan portfolio expansions, deposit increases, and prudent capital management including dividends and share repurchases. Risks remain primarily tied to credit performance and broader economic conditions.

Historical Performance and Growth Drivers

United Bankshares Inc., through its principal subsidiary United Bank, operates an extensive network of 237 offices across several states including West Virginia, Virginia, Maryland, Washington D.C., North Carolina, South Carolina, Georgia, Pennsylvania, and Ohio [S1][S4]. Historically, United has emphasized community banking services ranging from deposits to various loan products including personal, commercial, construction, residential real estate lending as well as trust and brokerage services.

Between 2022 and 2025, UBSI has demonstrated a trajectory of profit growth accompanied by robust cash flow generation despite modest declines in revenue figures. The company's reported revenues dropped approximately 5.7% from $330.96 million in FY2021 to $311.96 million in FY2022 based on available data [F1]. However, net income exhibited resilience with a jump from approximately $79.39 million in FY2023 to $128.83 million in FY2025 (+36.5% YoY) supported by expanding operations [F1]. Operating cash flow similarly increased from about $435 million (FY2023) to nearly $499 million (FY2025), underscoring operational strength amid broader industry challenges [F1].

Critical historical catalysts driving this performance include:

- The acquisition of Piedmont Bancorp completed on January 10th, 2025 added around $2.4 billion in total assets and expanded United’s geographic footprint notably into the Atlanta metropolitan area [S1][S20]. This deal increased loans by approximately $2 billion including purchase accounting adjustments [S12].

- A strategic move during first quarter 2024 consolidated mortgage origination activities under United Bank after exiting third-party originations by late 2023 [S4][S20]. This streamlined mortgage delivery channels that previously included George Mason Mortgage LLC and Crescent Mortgage Company.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 129 | 499 | 18 | +36.5% |

| 2024 | 94 | 445 | 12 | +18.9% |

| 2023 | 79 | 435 | 12 | -20.4% |

| 2022 | 100 | 761 | 17 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 209 | 127 | 481 |

| 2024 | 201 | 1 | 433 |

| 2023 | 195 | 1 | 424 |

| 2022 | 193 | 79 | 744 |

Source: SEC companyfacts cache [F1].

*Direct annual revenue numbers post-FY22 unavailable publicly; representations based on latest financial statements [F1][S3][S4]

Future Growth Prospects

Several factors outlined by United Bankships position it for continued growth:

- Geographical Expansion via Acquisition: The Piedmont Bancorp transaction brought immediate scale benefits with increased deposits ($2.11 billion), loans ($2 billion), and equity ($200 million), plus entry into key metro areas like Atlanta which provide new market opportunity [S20][S25]. Future acquisitions could follow this playbook given successful integration.

- Mortgage Origination Channel Rationalization: Having exited third-party origination sources and consolidated prior affiliations into a singular branding focused under United Bank should enhance operational efficiencies, reduce cost duplication and potentially improve margins in the mortgage segment [S4][N1].

- Diverse Loan Portfolio: UBSI continues emphasizing commercial real estate lending which represented a large slice (~50%) of total loans at year-end 2025 according to SEC filings [S16], alongside construction & land development lending with modest consumer loan exposure—this diversification within the credit book provides balanced risk return potential.

- Stable Core Deposits Base: Deposit growth was both organic ($993 million) and acquisition-driven ($2+ billion) giving the bank a sizeable low-cost funding base critical for margin preservation [S25].

Constraints or risks that could cap growth include:

- Economic Sensitivity: Credit risk remains prominent given potential adverse effects from economic downturns or higher interest rates on borrower ability to repay [S9][N1].

- Mortgage Market Volatility: Shifting regulatory or interest rate environments could impact mortgage origination volumes adversely.

- Integration Risks: Although past acquisitions have been integrated successfully, future merger activity always carries execution risks.

Forecasts / Milestones / Expectations

UBSI’s explicit forward guidance is not detailed publicly but key metrics to watch include:

- Continued organic deposit and loan growth rates particularly in new markets like Atlanta.

- Earnings progression reflecting integration synergies captured from Piedmont acquisition.

- Dividend payout changes; recent increases signal management’s confidence though balance must be maintained with capital needs.

- Share repurchase cadence which spiked substantially in fiscal 2025 ($127 million vs roughly ~$1 million prior years) indicating possible management belief stock is attractively valued or excess capital available for returns [S7].

Emerging credit trends especially watch nonperforming loans or allowance build-ups will be critical for investors monitoring risk trajectory [S15].

Returns / Capital Allocation

Investors should note that despite slower revenue growth trends recently (-5.7% YoY from data available), net income showed strong upward momentum (+36% YoY), suggesting improved cost controls or higher net interest margins possibly aided by deposit repricing or loan mix shifts [F1]. Approximate ROE computed as net income over equity stands near a modest ~2.3% for latest annual periods based on snapshot figures — likely influenced by elevated equity base stemming from acquisition-related increases [F1].

Capital allocation strategies reveal:

- A consistent dividend policy with incremental raises culminating in $209 million paid out in fiscal 2025 ($1.49 per share) slightly above prior year levels [F1][S14].

- Aggressive share buybacks scaled up dramatically during 2025 totaling nearly $127 million compared to about $1 million doubled-digit millions over prior several years under the prior plan revocation/replacement scenario approved late in calendar year [S7].

- Moderate capital expenditures reflective of branch network maintenance/technology upgrades at circa $18 million for FY25 [F1].

- Robust shareholders' equity grew over 10% year-on-year reaching just under $5.5 billion [$F1], supported largely by earnings retention combined with acquisition-related common stock issuances.

Capital adequacy ratios remain comfortably above regulatory thresholds—risk-based ratio stood at approximately 15.72%, CET1 ratio at about 13+%, indicating financial flexibility alongside sound risk management frameworks summarized extensively through the governance oversight structures for enterprise risk including cybersecurity monitoring detailed by the company’s Risk Committee setup reporting directly to Board level [S1][S9].

Sector Analysis Context (Analysis)

Regional banks such as UBSI face ongoing pressures balancing competitive loan pricing with deposit costs amid a patchy interest environment shaped by central bank policy shifts throughout recent years; however, successful expansion through deals enhances scale economies helping mitigate margin compression typical elsewhere. Community banking franchises benefit from high touch client relationships underpinning core deposit stability — an entrenched advantage forming part of UBSI’s moat given its multiple-state presence leveraging sizable brick-and-mortar footprints combined with diversified commercial lending streams. Amid rising cyber threats across the financial sector range alongside increased regulatory scrutiny around credit quality standards post-pandemic cycles, banks with dedicated sophisticated Risk Committees embedding NIST cybersecurity frameworks and professional CISO leadership are better positioned operationally—a factor explicitly documented for UBSI reflecting institutional maturity beyond mere transactional banking. Mortgage originations represent an area where mid-sized regional banks increasingly consolidate efforts internally away from brokered real estate channels due to better control over pricing dynamics and customer experience—a trend UBSI exemplifies with its channel restructuring completed last year. Finally, liquidity buffers remain paramount; UBSI’s substantial holdings in liquid securities coupled with diverse deposit bases ensure ample short-term flexibility critical for managing net interest income volatility inherent when long duration loans are funded chiefly through shorter duration deposits.

Risks Detailed by Company Disclosures

The foremost risks articulated include credit risk exposure sensitive to borrower performance variability potentially worsened by macroeconomic shocks or sectoral downturns impacting collateral values such as commercial real estate valuations [S9][S15]. Regulatory uncertainties around monetary policy shifts form additional mitigants though management reports comprehensive ongoing monitoring processes. Cybersecurity threats receive heightened attention with multiple layers of oversight including quarterly board reviews facilitated by seasoned CISO personnel possessing over two decades of institutional knowledge within United Bank’s structure—risk mitigation also encompasses employee awareness programs ensuring reporting lines remain active during incidents [S1]. Liquidity dependencies are regularly stress-tested via Asset Liability Committee frameworks supporting adequate access through Federal Home Loan Bank lines alongside correspondent bank facilities with significant unused borrowing capacities described at fiscal year-end demonstrating readiness against unforeseen funding demands [S6][S25][S26]. No material litigation issues appear disclosed affecting near-term financial stability as per recent filings management commentary.

Conclusion

United Bankshares displays characteristics typical of conservative yet opportunistic regional community banks advancing through strategic acquisitions augmenting scale whilst maintaining steady operational rationalizations such as mortgage channel consolidations enhancing efficiencies heading into future cycles. Strong capital ratios coupled with disciplined cash flow generation have enabled attractive shareholder returns via dividends and progressive share repurchases despite uneven revenue trends stemming largely from post-acquisition accounting transitions. Ongoing vigilance regarding credit risk exposures amid uncertain macroeconomic backdrops remains imperative alongside adaptability toward evolving regulatory compliance requirements particularly around cybersecurity governance frameworks evident within company disclosures. Investors tracking milestones should focus on organic loan/deposit growth rates outside acquired entities plus margin trajectories reflecting integration success plus any shifts signaling credit quality trends revealed quarterly. This synthesis refrains from investment recommendations but offers insight into structural company fundamentals backed rigorously by recent SEC filings ([S#]), factual news releases ([N#]), and official financial data ([F1]) up through early calendar year 2026.

This analysis is intended solely for informational purposes without providing investment advice or recommendations regarding United Bankshares Inc., its securities or affiliated entities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments