urban-gro’s Radical Retrenchment: From CEA Design-Build Pioneer to Focused Equipment Reseller

urban-gro, Inc.’s contraction from integrated Controlled Environment Agriculture services to a narrow reseller role underscores the challenges of sustaining competitive advantages amid financial and market pressures.

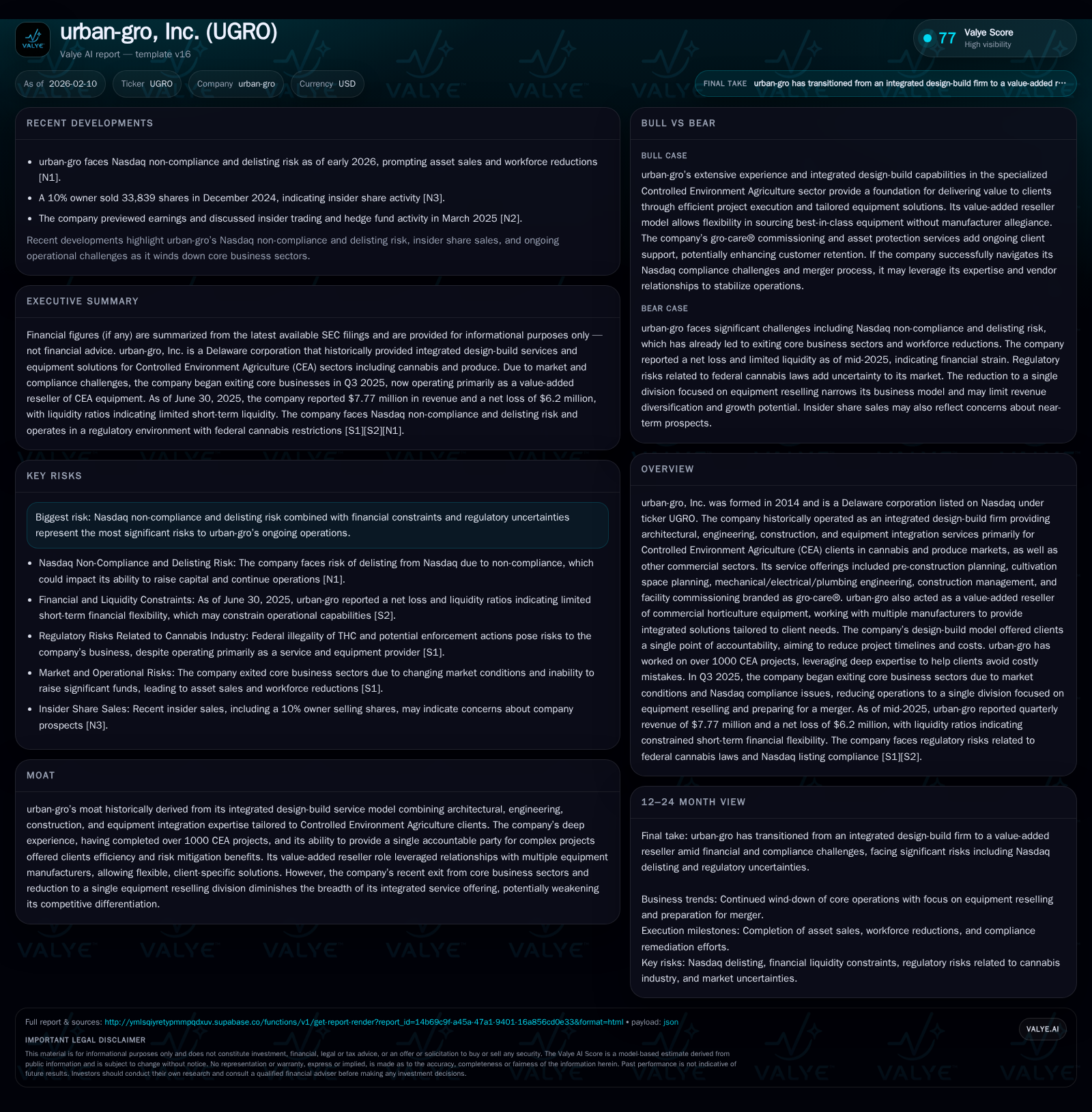

Founded in 2014, urban-gro rose as a leading integrator in Controlled Environment Agriculture (CEA), combining design, engineering, construction, and equipment integration targeting cannabis and produce markets. However, after escalating losses and liquidity crises, it dramatically exited its core design-build operations by late 2025, retaining only a single division as an equipment value-added reseller. This shift marks a steep erosion of its once-comprehensive moat. Regulatory risks including Nasdaq non-compliance compound the company’s difficulties amid evolving market and legal landscapes in CEA sectors.

From Integrated Design-Build Leader to Streamlined Reseller: urban-gro’s Shift

urban-gro was conceived as a pioneer in the Controlled Environment Agriculture (CEA) sector—notably cannabis and produce cultivation—offering clients a fully integrated design-build experience. This model encompassed architectural planning, mechanical/electrical/plumbing (MEP) engineering, construction management, and sophisticated equipment integration under a unified gro-care® brand. Such integration promised clients reduced project timelines and cost efficiencies through a single accountable party managing complex build-outs.

This broad scope rapidly expanded urban-gro's footprint across North America and Europe from its founding in 2014 through organic growth and acquisitions. By early 2020s, the company counted over 1,000 CEA projects executed—a testament to its depth of experience and trusted industry presence [S1].

However, facing deteriorating market conditions exacerbated by regulatory complexities around cannabis-related operations and hardening capital markets for growth-stage companies, urban-gro confronted mounting financial strain. Efforts to raise funds were stymied by Nasdaq compliance issues and investor wariness toward volatile sector players.

By Q3 2025, management made the consequential decision to exit core service sectors including design/build operations entirely. Subsequent months saw widescale asset sales and workforce reductions as urban-gro pivoted sharply toward a leaner business model focused exclusively on equipment reselling within the CEA space. Today, only one legacy division remains: acting as a value-added reseller (VAR) sourcing horticulture lighting systems, irrigation controls, microbial mitigation devices, and other cultivation equipment [S1].

This strategic retraction symbolizes both an adaptive survival move and a significant relinquishment of prior ambitions.

Anatomy of the Moat: How urban-gro’s Competitive Edge Evolved and Eroded

Originally urban-gro’s moat was built upon synergies between multi-disciplinary design expertise and intricate knowledge of horticultural technologies—a combination that few competitors matched. Offering end-to-end solutions allowed clients simplified project management alongside innovative environmental controls critical for high-stakes CEA facilities.

Moreover, the company maintained vendor-agnostic equipment relationships enabling bespoke solutions aligned tightly with client needs rather than off-the-shelf packages [valye_report_excerpt]. This advantage materially differentiated urban-gro from commodity-focused wholesalers or direct-from-manufacturer sales.

Yet this robust competitive edge has dissipated alongside business deconsolidation. By shedding engineering and construction arms—and with no longer internal teams managing installation or commissioning—urban-gro now primarily offers transactional equipment sales bundled with expert advisory input rather than holistic turnkey services.

While retained knowledge of horticultural equipment interactions remains valuable for customers navigating complex grow environments, the breadth that once encompassed over 1,000 comprehensive projects is now confined to selling components rather than designing integrated ecosystems [valye_report_excerpt].

Consequently, clients seeking large-scale CEA build-outs likely turn elsewhere for full-spectrum providers capable of reducing risk through seamless project execution.

Financial Turnaround Roadblocks: Chronic Losses and Cash Flow Pressures

Despite early revenue growth—from $25.8 million in 2020 to almost $70 million in 2023—urban-gro’s bottom line consistently showed substantial deficits. Net losses ballooned from $5.1 million (2020) to $36.5 million (2024), reflecting operating inefficiencies amid expansion pressures [S1].

Cash flow tells an equally somber story; negative cash flow from operations exceeded $10 million in fiscal year 2023 itself before easing marginally in 2024 yet remaining negative at about $2.8 million [S1]. These persistent outflows precipitated urgent liquidity constraints.

Revenue collapsed precipitously following corporate restructuring efforts: trailing six-month revenues halved again to roughly $7.8 million by mid-2025 [F1]. The stark decline mirrors rapid divestitures paired with shrinking service volumes inherent to relinquishing higher-margin design/build operations.

Current assets at June 30, 2025 amounted to approximately $7.4 million against current liabilities exceeding $43 million—yielding a perilous current ratio near 0.17 that signals imminent working capital insufficiency absent capital raises or debt restructuring [F1].

This imbalance underscores the tenuous operational capacity remaining without objective changes.

Nasdaq Non-Compliance: Regulatory Risks Threatening Listing Status

An impending threat compounds financial distress: urban-gro currently faces formal Nasdaq non-compliance notices centered on minimum bid price rules or other listing standards [N1]. Such warnings place the company at risk of delisting if remedial steps are not taken promptly.

Given that Nasdaq presence is crucial for equity market access and liquidity visibility among institutional investors—and essential for broader fundraising—the risk jeopardizes already tight capital pathways [S1][S2].

The company candidly acknowledges these risks within SEC filings as existential threats capable of material adverse effect upon operations or share price stability [S1], embedding regulatory vulnerability within the firm’s overall risk profile.

Market Dynamics in Controlled Environment Agriculture: Opportunities and Obstacles

CEA as an industry remains nascent but rapidly evolving; it encompasses cultivation methodologies using controlled environmental variables such as light spectra modulation, humidity regulation, fertigation systems, microbial controls—all areas where technical expertise matters deeply.

However, legal ambiguity surrounding cannabis cultivation continues shifting with state-by-state regulatory reforms in North America while produce vertical farming is undergoing scaling challenges balancing technology costs against yields [S1][valye_report_excerpt]. This uneven landscape shapes client confidence unevenly.

Further complicating matters are consumer sentiment swings tied to cannabis legalization debates impacting investment appetites downstream. Suppliers focused narrowly on cannabis may face demand volatility absent diversification strategies.

Urban-gro historically diversified service offerings into healthcare-industrial-commercial sectors beyond cannabis but retrenchment curtails such optionality today [S1]. Thus it remains exposed chiefly to fluctuations affecting CEA operator capital expenditure cycles.

Current Business Model and Partnerships: Tailoring Equipment Solutions for CEA

Presently urban-gro operates predominantly as a value-added reseller emphasizing customization rather than commoditized sales volume [valye_report_excerpt]. Its role entails leveraging vendor partnerships with established manufacturers across lighting technologies, rolling bench systems for efficient space utilization, fertigation automation components alongside odor reduction innovations applicable in closed-loop grow rooms.

The 'equipment agnostic' approach allows selection best fitting specified client budgets/design parameters without allegiance constraints—a notable strength distinguishing urban-gro from mono-vendor suppliers or mass-market distributors reliant on standard catalogues.

Expertise remains vital here; understanding intricate system interdependencies gives clients assurance that purchased systems function cohesively under variable growing conditions despite loss of full architectural/engineering capabilities internally.

Competitors within this narrow reseller segment tend more towards either wholesale commodity dealers or online retailers lacking consultative depth [valye_report_excerpt]. Urban-gro thus retains some competitive edges even amidst contraction.

Debt, Liquidity, and Operational Capacity: A Balance Sheet Under Stress

As recounted earlier via F1 data points above—the balance sheet highlights acute stress points with current liabilities dwarfed by markedly lower current assets post restructuring [F1]. This mismatch presses urgent questions around how ongoing obligations are met absent fresh financing or asset monetization proceeds.

While cash & equivalents were recorded near $18.6 million as recently as Q3 2022 [F1], dwindling revenues coupled with operational burn have eroded liquid reserves rapidly during protracted wind-down efforts leading into mid-2025 when cash metrics became more constrained.[F1]

Debt servicing or short term creditor pressures may therefore limit financial flexibility undermining capacity to maintain workforce levels or vendor commitments critical for ongoing VAR activities known to remain minimal compared with legacy multi-service operations.

Controlling operating expenses is emphasized repeatedly by management aiming toward eventual positive cash flow—but success rests on stabilizing revenue base within this narrower remit which remains an open challenge given sector uncertainties [S1].

The Path Forward: Restructuring, M&A Prospects, and Strategic Realignment

urban-gro publicly signals ongoing efforts preparing for potential merger transactions following asset dispositions aimed at salvaging shareholder value or ensuring continuity under new ownership structures [valye_report_excerpt],[N1]. Such moves typify companies facing severe structural headwinds seeking consolidation-driven lifelines.

Strategies may include bolstering VAR capabilities combined with organic repositioning toward adjacent commercial verticals outside cannabis-focused cultivation while controlling fixed infrastructure costs tightly.[S1]

However the feasibility depends heavily on external market factors like regulatory clarity improvements in cannabis laws paired with capital market receptivity toward specialized ag-tech providers battered by prior years’ tumultuous trends.

Simply put: recovering scale sufficient to regain original competitive advantages appears unlikely absent significant external catalysts; instead survival will likely aim at maintaining niche VAR relevance until broader sector stabilization occurs.

Disclaimer: This analysis is an informational overview based solely on publicly available data up to February 10, 2026 (sources included). It does not constitute investment advice nor an endorsement of any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments