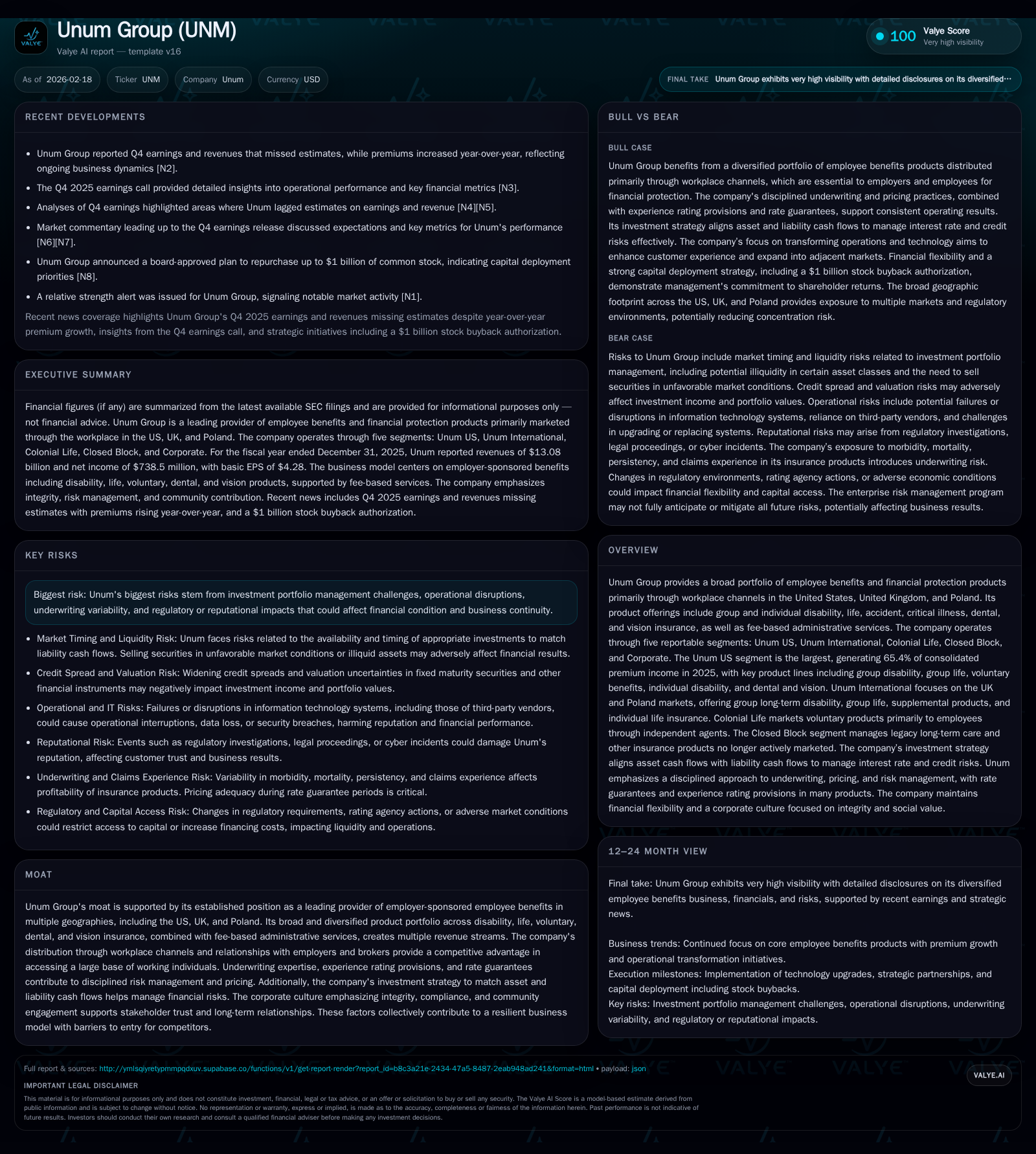

Unum Group's Multi-Channel Approach to Employee Benefits Drives Modest Growth

Unum Group leverages a diversified geographic and product footprint alongside disciplined capital deployment amid earnings volatility.

Unum Group sustains revenue growth at a modest 1.5% in 2025 driven by its multi-channel employee benefits portfolio spanning the US, UK, and Poland, despite facing significant net income pressure with a 58.5% decline. The company's core Unum US segment dominates premium income but contends with underwriting and claims challenges that have compressed profitability and operating cash flows. With an approximate 6.6% ROE, Unum remains committed to shareholder returns through dividends and aggressive buybacks, even as free cash flow tightens. Risk factors centered on underwriting assumptions, investment portfolio sensitivity, and regulatory exposures persist. Growth prospects hinge on digital transformation, voluntary benefits expansion, and effective risk management against competitive headwinds.

Historical Growth Patterns: Revenue Gains Meet Earnings Headwinds

Unum Group's financial results for fiscal year 2025 reveal a nuanced picture of steady top-line expansion overshadowed by a pronounced contraction in net income and operating cash flows. Revenues reached $13.08 billion, marking a modest increase of approximately 1.5% versus $12.89 billion reported in 2024 [F1]. However, net income fell dramatically by 58.5%, from $1.78 billion in the prior year down to $738.5 million in 2025 [F1], signaling margin compression likely linked to underwriting strain and elevated claim experience.

Operating cash flow also suffered a significant decline of 54.6%, retreating to $687.7 million from $1.51 billion a year earlier [F1]. This sharp drop underscores emerging capital adequacy pressures faced by Unum as it navigates claim liabilities alongside evolving actuarial assumptions surrounding disability durations and mortality factors [S1]. Capital expenditures remained largely stable on an absolute basis at $132 million with a slight rise of roughly 5.3% compared to the prior year’s $126 million spend [F1]. Return on equity at an estimated 6.6% in 2025 reflects subdued profitability relative to equity base of about $11.19 billion [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 13.1 | 739 | 688 | 132 | +1.5% | -58.5% |

| 2024 | 12.9 | 1779 | 1513 | 126 | +4.0% | +38.6% |

| 2023 | 12.4 | 1284 | 1203 | 135 | +3.3% | -2.3% |

| 2022 | 12.0 | 1314 | 1419 | 102 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 306 | 1010 | 555 |

| 2024 | 297 | 973 | 1388 |

| 2023 | 277 | 250 | 1068 |

| 2022 | 254 | 200 | 1317 |

Source: SEC companyfacts cache [F1].

Note: Operating Income figures are unavailable for recent years in provided data.

Segmental Performance and Geographic Footprint Analysis

Unum’s business operates primarily through three principal reporting segments: Unum US, Unum International (focused on UK and Poland), and Colonial Life; additional segments include Closed Block and Corporate [S8][S17]. The Unum US segment remains dominant, delivering approximately two-thirds (65.4%) of consolidated premium income in calendar year 2025 [S8]. This segment mainly covers group disability (long-term and short-term), group life insurance including accidental death & dismemberment (AD&D), voluntary benefits such as supplemental life products, individual disability insurance, plus dental and vision coverages.

The international unit contributes around a tenth (10%) of premiums mainly from group long-term disability schemes in the UK as well as individual life insurance offerings in Poland [S8][S17]. Colonial Life accounts for nearly one-fifth of premiums (17%) focusing on voluntary workplace benefits sold directly to employees via workplace channels which augment employer-sponsored plans.

The portfolio breadth—disability, life, dental, vision—and multi-market presence create diversified income streams that theoretically smooth volatility exposures inherent in claims patterns across regions with distinct regulatory environments.

Underwriting discipline is central to Unum’s moat: actuarial assumptions on future policy benefit liabilities are regularly calibrated within established frameworks incorporating experience-rating provisions that allow premium adjustments aligned with claims emergence trends [S1][S18]. Rate guarantees underpin contracts particularly for noncancelable individual disability products limiting repricing flexibility but stabilizing risk exposure over long claim durations typical of disability lines [S18]. In group markets like US long-term disability or life insurance tiers, repricing actions respond laboriously given competitive renewal dynamics but act as critical levers managing profitability amidst adverse claim incidence or administrative expense inflation.

Capital Deployment and Shareholder Returns: Dividends and Buybacks Scrutinized

Despite persistent earnings pressure reflected in collapsing net profits for fiscal year-end December 31, 2025, Unum continued deploying capital aggressively toward shareholder returns with nearly one-third billion dollars paid in dividends ($306 million) and over $1 billion dedicated to share repurchases during the same period [F1]. The buyback figure is particularly notable — more than tripling from fiscal year ’23 levels ($250 million) — evidencing a strategic priority on capital return even under cash flow constraints.

Free cash flow—approximated here as operating cash flow minus capital expenditures—tightened markedly to about $555 million from upwards of $1.38 billion two years prior [F1], highlighting mounting liquidity strain despite disciplined capex policies.

Near-term sustainability implications emerge considering an ROE around a tepid mid-single digit level (6.6%) combined with volatile earnings generation that may hinder consistent excess returns over capital cost thresholds typical for insurers maintaining robust credit ratings [F1][S21]. Nonetheless, management's approach underscores confidence in long-term value accretion fueled by strategic investments coupled with an assertive buyback posture enhancing per-share metrics.

Emerging Risks in Underwriting and Investment Portfolios

Key risk vectors identified within Unum's filings emphasize complexities inherent to actuarial assumptions determining the liability for future policy benefits—a cornerstone variable directly affecting earnings recognized under GAAP accounting principles [S11][S23]. These assumptions encompass claim incidence rates influenced by macroeconomic factors such as unemployment trends impacting disability claims frequency as well as social behavioral shifts including work ethic perceptions which can cause material variance versus expected outcomes over time [S1]. Claims duration uncertainties compounded by medical advances potentially extending or shortening benefit periods pose additional modeling challenges altering reserve adequacy determination substantially.

Repricing agility differs markedly between product lines: while group disability contracts can undergo periodic price adjustments responding to adverse claim trends albeit with lag times limiting immediate impact realization; certain individual disability policies feature fixed premiums reflectively insulating insurers from quick corrective rate hikes thus increasing risk exposure if actual claims worsen persistently beyond assumptions [S18].

Investment portfolio risks pivot around interest rate sensitivity—declining yields reduce net investment income supporting pricing assumptions—coupled with default risks embedded predominantly within fixed maturity securities composing the bulk of invested assets [S24][S25]. The company's asset-liability matching strategy involves quarterly scenario tests around cash flow duration alignment but remains vulnerable to macro-financial shocks limiting liquidity access or impacting reinvestment yields negatively.

Regulatory landscape complexity introduces further uncertainty notably through supervisory reviews potentially imposing increased reserving requirements or operational constraints adversely affecting earnings capacity or capital adequacy thresholds especially given global jurisdictional variance between U.S., U.K., and Poland operations reflected across subsidiaries [S13][S16].

Additionally emerging operational risks relate to artificial intelligence adoption accelerating automation across underwriting, claims adjudication, and customer engagement functions; compliance ambiguities inherent to AI regulation introduce legal exposures alongside potential reputational damage should failures occur amidst fast-evolving technological ecosystems [S20].

Future Growth Drivers and Market Challenges

Management articulates focused growth initiatives targeting core business expansion augmented by technology-driven transformation aimed at enhancing customer experience and operational efficiency while simultaneously broadening market reach through adjacent product lines notably voluntary benefits which represent an attractive supplement fitting within employer-sponsored channels servicing middle-income workers historically underserved by mainstream financial protection solutions [N2][S12].

Digital integration efforts span enrollment platforms facilitating seamless multi-product offerings increasing employee participation rates—a crucial penetration metric enhancing portfolio resilience amid competitive market pressures characterized by innovations pulling share toward incumbents offering flexible enrollment experiences supported by data analytics.

Geographic diversification offers natural hedging against idiosyncratic regional downturns or localized regulatory shocks given differing demographic profiles underpinning disability prevalence or mortality rates between North America versus Europe especially within aging populations driving long-term care demand dynamics differently than younger workforce segments predominant across U.S.-based employer groups.

Yet economic headwinds such as inflation-induced premium sensitivity reductions or wage growth stagnation remain potential growth caps while intensifying competition—both traditional insurers scaling via M&A activity plus new entrants leveraging insurtech capabilities—and heightened regulatory scrutiny temper aggressive pricing strategies underpinning new business acquisition economics critically important for renewal persistency trajectories sustaining lifetime value metrics framework governing profitability benchmarks [S15][N2].

Forward Indicators: Key Milestones and Watchpoints for Investors

Explicit company guidance remains limited from public disclosures; therefore stakeholders should closely monitor quarterly updates detailing premium renewal rates couples with underlying loss ratios providing insight into whether repricing measures effectively offset adverse claims experience unfolding post-2025 results announcement cycle [N3][N1]. Changes in claim duration patterns linked to ongoing medical progress or societal norm shifts could materially influence future periods requiring dynamic actuary recalibrations affecting reserve build-up or release timing.

Investment yield trajectory amidst evolving interest rate cycles—particularly fixed-income coupon re-investment environments—will be critical given their direct causality linking portfolio returns supporting discount rate assumptions embedded within policy liability calculations fundamentally impacting earnings quality over time horizons exceeding routine reporting intervals [N3][S24].

Regulatory developments both domestic (e.g., state insurance departments’ rate increase approvals) and international (e.g., PRA mandates on solvency margins) merit scrutiny due to potential capital contribution requirements affecting dividend capacity or strategic flexibility around line exits/acquisitions worth tracking closely through filings or analyst briefings concurrent with earnings calls documenting updated management outlooks highlighting operational pivots undertaken during transition phases addressing emerging risks identified herein.

Corporate Governance, Culture, and Regulatory Risk Considerations

Unum Group’s culture anchors on delivering socially valuable financial protection products grounded firmly in integrity-centric operations seeking alignment with stakeholder interests encompassing customers reliant on timely claims settlements alongside communities supported via corporate social responsibility initiatives outlined extensively reflecting commitments toward sustainability integration incrementally embedding environmental-social-governance (ESG) factors into investment decision-making processes advancing responsible investing mandates consistent with evolving stakeholder expectations manifested globally among large institutional owner bases targeting ESG alpha capture strategies alongside risk mitigation objectives within complex financial services firms like insurers today [S5][N2].

Nonetheless litigation risk remains salient given the volume of claim disputes including single claimant actions occasionally seeking punitive damages challenging claims handling judgments which carry reputational implications potentially damaging market positioning beyond direct financial reserves maintained within prudential thresholds described transparently illustrating risk appetite calibrated conservatively yet exposed inevitably to case law outcome unpredictabilities requiring continuous monitoring alongside robust legal defense infrastructures supporting claims teams actively managing adverse outcomes likely shaping provisions recorded periodically within financial disclosures aligned tightly with regulatory compliance standards designed to maintain insurer trustworthiness essential for long-term licensed operations across multinational jurisdictions subjected constantly to audits/examinations enforced stringently given policyholder protection prioritization over shareholder interests uniquely characterizing regulated insurance frameworks globally contrasting unconstrained corporate sectors prevalent elsewhere [S4][S22][S23].

Moreover rapid incorporation of AI-driven tools heightens regulatory surveillance amplified by nascent legal frameworks emphasizing data privacy plus bias mitigation necessitating evolved governance protocols ensuring ethical application preventing inadvertent operational disruption thereby safeguarding institutional reputation foundationally intertwined with competitive viability long term facing intensifying scrutiny from regulators heightened concurrently with tech innovation adoption pace acceleration posing material yet manageable risks contingent upon governance efficacy sustained vigilantly moving forward operationalizing learnt lessons iteratively improving compliance robustness integral components fortifying enduring enterprise resilience under evolving external conditions documented meticulously within periodic SEC filings centralizing transparency commitments mandated publicly listed insurers embodying best practice norms exemplified regularly underscoring accountability ethos entrenched comprehensively across corporate levels senior leadership teams actively engaged executing multifaceted risk oversight extending well beyond traditional underwriting nor investment spheres embracing holistic enterprise risk management frameworks continuously adapting dynamically preserving stakeholder confidence foundationally critical sustaining franchise equity imperilled otherwise absent proactive measures documented scrupulously herein [S4][N2][N3].

Disclaimer: This analysis is based solely on publicly available information including SEC filings ([F1], [S#]) and verified news reports ([N#]) without speculation beyond presented data points; it does not constitute investment advice but aims to provide comprehensive context on Unum Group’s business operations, financial performance trends, strategic posture, risk profile, and forward-looking considerations relevant within the employee benefits insurance sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments