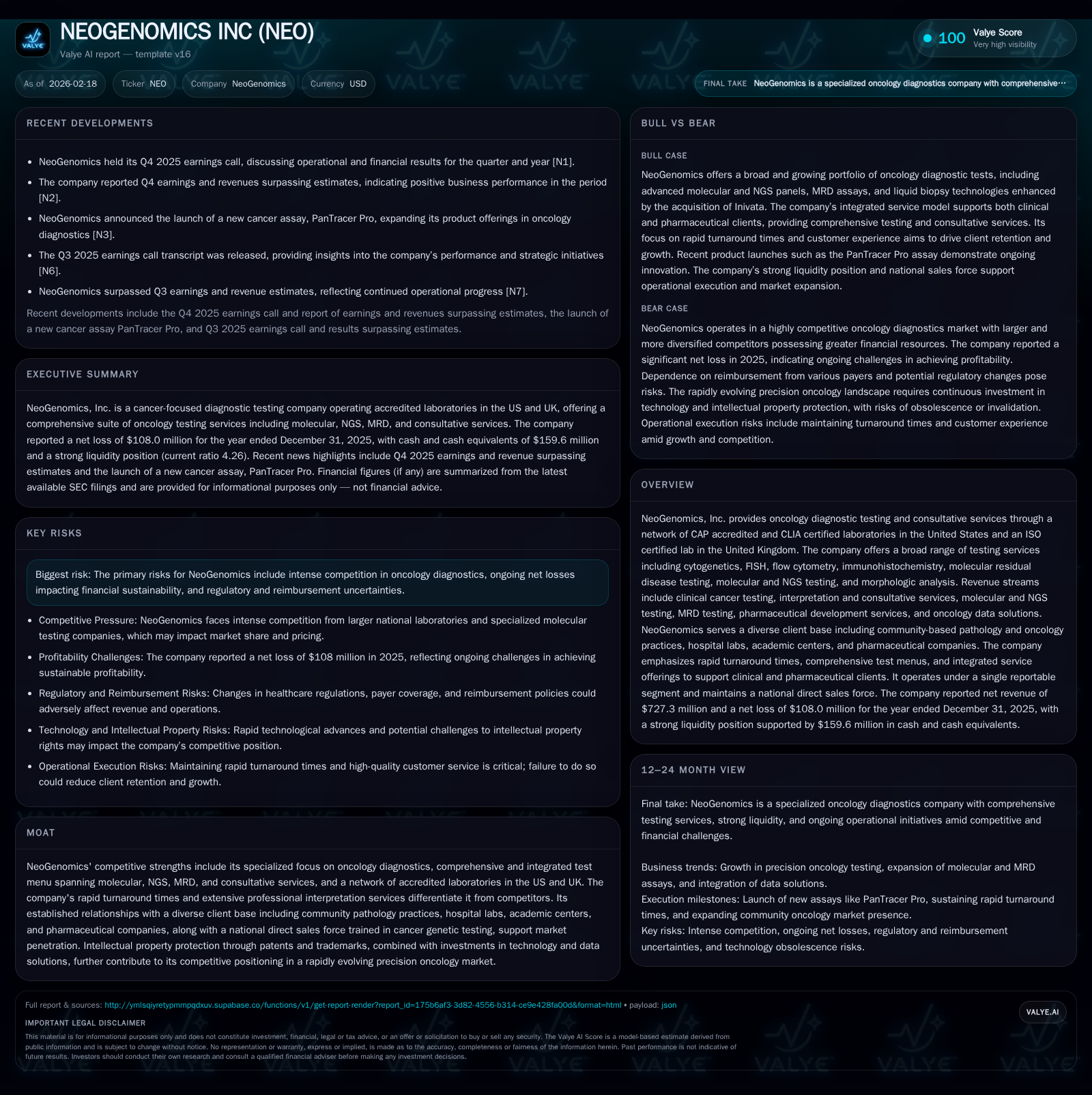

NeoGenomics' Strategic Focus on Oncology Diagnostics Challenges Financial Sustainability

NeoGenomics pursues growth in oncology diagnostic testing amid ongoing operating losses and regulatory risks.

NeoGenomics Inc. operates a specialized oncology diagnostics network with CAP-accredited and ISO-certified labs across the US and UK, offering molecular, cytogenetics, NGS, and MRD testing services. Historical financials reveal persistent operating losses despite modest cash flow generation and sustained capex investment aimed at expanding test menus and technology platforms. The company faces regulatory, reimbursement, and litigation risks that could constrain future growth and financial stability. Despite these challenges, NeoGenomics aims to grow through new product launches, market penetration in community oncology, and operational enhancements focused on therapy selection and MRD testing.

Company Overview

NeoGenomics Inc. is a cancer-focused diagnostics company operating accredited laboratories throughout the United States and the United Kingdom. Its service portfolio spans technical laboratory tests like cytogenetics (chromosome analysis), fluorescence in situ hybridization (FISH), flow cytometry, immunohistochemistry, molecular residual disease (MRD) assays, next-generation sequencing (NGS), alongside professional interpretation provided by licensed pathology experts specializing in oncology [S1]. This specialization positions NeoGenomics within the precision oncology segment where demand centers on rapidly evolving genetic and molecular diagnostic capabilities.

Historical Financial Performance

Between fiscal years 2022 and 2025, NeoGenomics recorded consistent operating losses though losses have diminished over time. Operating income improved from -$157.6 million in 2022 to -$115.9 million in 2025 (-25.8% year-over-year change most recently), while net income losses narrowed from -$144.3 million to -$108 million during the same period (-37.2% YoY) [F1]. The narrowing net loss reflects operational improvement but continued unprofitability.

Operating cash flow followed a similar trajectory turning positive in recent years (+$5.2 million in 2025 vs negative $66 million in 2022), yet heavy capital expenditures continue to produce negative free cash flow; for instance free cash flow was roughly -$21.8 million in 2025 [F1]. These investments mainly fund laboratory instrumentation upgrades, IT systems including new LIMS implementations critical for handling increasing sample volume with quality control demands [S14][S27].

The company’s balance sheet reveals ample liquidity: $159.6 million in cash plus current assets of $376 million against current liabilities below $88 million yields a healthy current ratio exceeding 4x as of end-2025 [F1]. Equity levels declined moderately over four years due to accumulated losses but remain robust at approximately $836 million at year-end 2025 [F1]. No dividend payments or buyback programs have been reported recently; share repurchases recorded were tax withholding related retirements of employee-restricted stock rather than open-market buybacks [S12].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -108 | 5 | -116 | 27 | -37.2% |

| 2024 | -79 | 7 | -92 | 41 | +10.5% |

| 2023 | -88 | -2 | -108 | 29 | +39.0% |

| 2022 | -144 | -66 | -158 | 31 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -22 | -12.9 |

| 2024 | -34 | -8.7 |

| 2023 | -31 | -9.3 |

| 2022 | -97 | -14.5 |

Source: SEC companyfacts cache [F1].

*Revenue provided only for semiannual periods prior to recent years; hence annual revenue not comparable. **Comparisons limited due to quarter/period differences.

Market Positioning & Competitive Edge

NeoGenomics' moat derives from its all-encompassing focus on cancer diagnostics featuring one of the industry's broadest integrated service menus — covering cytogenetics to advanced molecular assays — supported by rapid turnaround times and extensive clinical interpretation services [S18]. Their laboratories hold CAP accreditation and CLIA certification throughout the U.S., with ISO certification in their UK lab fostering confidence among institutional clients.

Their customer base is diverse ranging from community oncologists/pathologists through hospital labs, academic centers to pharmaceutical companies requiring support for clinical trials [S1][S17]. This diversity helps mitigate client concentration risk since no single customer accounts for over 10% of revenues [S24]. Nonetheless, competition from larger entities such as Quest Diagnostics or LabCorp as well as niche oncology diagnostics firms like Guardant Health or Caris Life Sciences remains intense along price points, breadth-of-menu offerings, IT interface sophistication for ordering/sample collection convenience as well as consultative value-adds post-testing [S18].

Growth Prospects & Catalysts

NeoGenomics articulates growth plans centered on launching differentiated assays targeting therapy selection guidance and ultra-sensitive minimal residual disease detection aligned to precision medicine trends [N3][S17]. The recent launch of the PanTracer Pro assay represents an example of expanding their oncology molecular test catalog using proprietary technology to enhance sensitivity—important for earlier detection of relapse or treatment response.

Additionally, intentional penetration into the burgeoning community oncology segment leverages their established nationwide direct sales force trained specifically on cancer genetics testing nuances—a focus area less served by large generalist labs [S17]. Strategic partnerships aimed at accelerating topline growth through expanded market reach are key components alongside continuous IT systems improvements intending to reduce margins via automation and operational excellence.

Regulatory & Legal Risks

A persistent overhang relates to regulatory compliance in billing practices notably involving federal healthcare programs such as Medicare/Medicaid that contribute about 13% of revenues per year consistently [S5][S21]. The company has voluntarily disclosed certain consulting contracts potentially implicating fraud/waste/abuse laws since an investigation initiated internally in late-2021 continues with an existing reserve of $11.2 million booked reflecting estimated probable loss exposure [S4][S10]. The ultimate financial outcome remains uncertain given ongoing governmental reviews which could impose fines or operational restrictions.

Further litigation includes shareholder derivative suits linked to alleged misstatements predominantly resolved intellectually through favorable invalidation rulings against competitors’ patents on assays formerly contested by NeoGenomics alleviating some IP litigation risk burden through past proceedings [S8][S9]. Nonetheless, the typical uncertainties inherent in litigation—and associated costs—remain present especially dealing with both professional liability exposures intrinsic to cancer testing errors or delays alongside intellectual property challenges.

Capital Allocation & Financial Strategy

NeoGenomics’ balance sheet management includes retiring its $201 million convertible notes due May 2025 without replacement debt issuance reported during calendar year 2025 effectively reducing near-term leverage concerns [S19][S23][S14]. Interest burdens on retired notes had been minimal (~1.25%) but amortization effects contributed to modest interest expenses historically.

Capex spending has been substantial reflecting investment intensity required for technological innovation inside clinical laboratories—$27 million deployed in LY versus over $41 million prior year indicating a meaningful ramp down consistent with completion phases of major equipment rollouts or technology deployments such as LIMS [F1][S14]. Operating cash flows being positive albeit modest suggests improving core business economics though full free cash flow remains constrained.

Currently no dividends have been issued nor significant share repurchases announced save for retirements related to restricted stock tax withholding activities that do not reflect opportunistic buybacks [S12]. Given ongoing losses ROE remains negative at approximately -13%, indicating that creating shareholder value via underlying earnings will require sustained margin improvements beyond revenue growth alone.

What To Watch Forward (Analysis)

Observers should monitor revenue trajectory explicitly disclosed going forward since historical revenue data is sparse outside non-standardized quarterly disclosures [N1][N2]. Key milestones will include successful uptake rates for novel assays like PanTracer Pro especially within community oncology settings where patient volumes can offer scalable top-line inflections.

The resolution of governmental investigations remains critical; any adverse findings leading to material penalties or exclusion from government program reimbursements could materially impair cash flows given Medicare’s role albeit limited portion of total revenue.

Operational adoption success of LIMS systems will play into cost structure improvements enabling faster turnaround times—and margin recovery—which are core strategic objectives amidst stiff competition demanding both quality and price efficiency.

Lastly competitive dynamics may shift if regulatory frameworks governing laboratory-developed tests change unexpectedly despite recent court rulings which currently preserve status quo risking increased compliance costs or delays in commercialization pipelines.

Conclusion

NeoGenomics remains a specialized actor with meaningful technological breadth serving an oncology diagnostics niche that is expected to grow with advances in precision medicine therapy selection tools and ultra-sensitive disease monitoring techniques like MRD testing.[N3][S17] However, these opportunities come against persistent operating losses exacerbated by high R&D/capex investment profiles coupled with significant regulatory/legal risks that temper financial sustainability.[F1][S4] Liquidity appears sufficient near term.[F1] Execution risk surrounds commercial success within competitive landscapes dominated by larger players with deeper financial reserves.[S18]

This blend frames NeoGenomics as a precision oncology diagnostic innovator working toward scale profitability under uncertain regulatory clouds—a company positioning itself through targeted product innovations and channel expansions while bearing heightened execution complexity.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available SEC filings and news sources as cited; it does not constitute investment advice or recommendations regarding NeoGenomics Inc.’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments