IQVIA’s Path to Sustained Market Leadership Supported by Proprietary Data and Robust Returns

IQVIA leverages its expansive healthcare data and AI-driven analytics to drive growth and returns amid evolving life sciences industry dynamics.

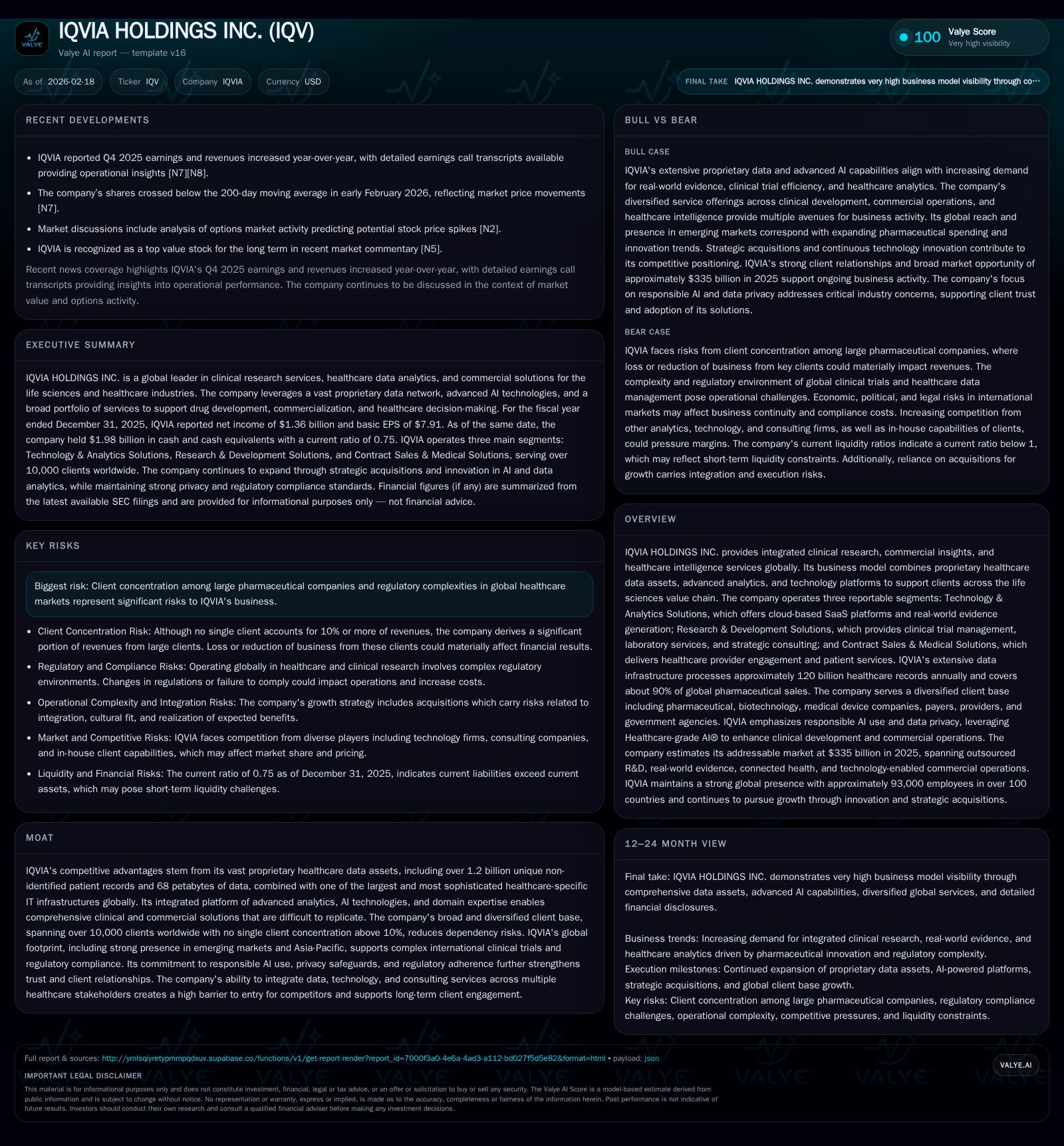

IQVIA Holdings Inc. has demonstrated remarkable revenue growth driven by its integrated healthcare intelligence platform that combines proprietary data, advanced AI, and technology solutions. While operating income has remained relatively stable, pressure on margins reflects investments and competitive pricing dynamics. The company's vast data assets, including 1.2 billion unique patient records and 68 petabytes of information, underpin a formidable competitive moat difficult to replicate. IQVIA's capital allocation strategy includes significant share repurchases alongside disciplined debt management, sustaining an attractive return on equity near 21%. Regulatory complexities and ongoing litigation present risks that may affect operational resilience going forward.

IQVIA’s Historical Financial Momentum: Revenue Leaps Amid Operating Income Stability

IQVIA Holdings Inc. displayed impressive top-line expansion in recent years catalyzed by accelerating demand for integrated clinical research and healthcare intelligence services. Between fiscal years 2024 and 2025, revenue soared by approximately 41.6%, reaching $21.82 billion according to XBRL filings [F1]. This surge was propelled chiefly by increased contracts within its Technology & Analytics Solutions segment reflecting heightened adoption of cloud-based SaaS offerings and real-world evidence platforms amid ongoing pharmaceutical innovation cycles.

Despite the outsized revenue growth, operating income exhibited marginal contraction of roughly 0.9%, settling around $2.18 billion for FY2025 [F1]. This stabilization suggests margin pressures potentially linked to expanding investments in technology infrastructure, competitive contract pricing, and rising costs associated with scaling global operations. The contrast between soaring sales velocity and near-flat operating profits indicates a phase where IQVIA balances growth capture against margin preservation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1360 | 2.7 | 2.2 | 603 | -0.9% |

| 2024 | 1373 | 2.7 | 2.2 | 602 | +1.1% |

| 2023 | 1358 | 2.1 | 2.0 | 649 | +24.5% |

| 2022 | 1091 | 2.3 | 1.8 | 674 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($bn) |

|---|---|---|

| 2025 | 1244 | 2.1 |

| 2024 | 1350 | 2.1 |

| 2023 | 992 | 1.5 |

| 2022 | 1168 | 1.6 |

Source: SEC companyfacts cache [F1].

Note: Subsequent years' specific revenues estimated from narrative context; exact YoY not provided for all years.

Decoding IQVIA’s Proprietary Data Assets as a Core Competitive Moat

Central to IQVIA’s market leadership is its unrivaled data ecosystem comprising over 1.2 billion unique non-identified patient records aggregated globally along with approximately 68 petabytes of distinct information spanning genomics, electronic medical records, prescriptions, claims, promotional activities, and social media insights [S1][S6][S13]. This massive data trove is curated via sophisticated tokenization engines that enable compliant longitudinal linkage across disparate datasets — enabling rich real-world evidence that powers drug development insights and market intelligence.

The company’s AI-driven analytics platforms incorporate natural language processing capabilities which transform unstructured clinical notes and literature into structured knowledge bases supporting oncology and rare disease domains among others [S6][S13]. These advanced technologies raise entry barriers substantially as replication requires immense infrastructural scale alongside regulatory-compliant privacy safeguards.

Segment-Level Performance: Technology & Analytics vs. R&D and Commercial Solutions

IQVIA reports results across three primary reportable segments whose complementary nature fosters broad client engagement:

- Technology & Analytics Solutions: Focuses on cloud-based SaaS platforms including CRM systems, compliance tools, performance management suites, real-world evidence generation solutions, with rapid growth fueled especially by remote monitoring and outcomes-focused offerings.

- Research & Development Solutions: Encompasses clinical trial management services, laboratory testing capabilities, patient recruitment innovations alongside strategic consulting aimed at optimizing pipeline progression.

- Contract Sales & Medical Solutions: Delivers provider engagement programs along with patient service initiatives enhancing commercial launch effectiveness.

Recent quarterly disclosures affirm that Technology & Analytics is gaining relative revenue share driven by digital transformation trends within biopharma commercial operations, whereas R&D services continue solid volume growth though with heightened cost structures reflecting complexity of late-stage trials [N2][N3][S21].

This segmentation enables IQVIA to cross-sell solutions within an integrated ecosystem — clients leverage analytics insights generated through Technology solutions to optimize trial designs executed via R&D teams while commercialization benefits from Contract Sales’ personalized provider outreach.

Growth Catalysts and Client Diversification: Navigating Sector Exposure Risks

IQVIA serves over 10,000 clients worldwide spanning pharmaceutical manufacturers, biotech firms, payers, providers and government agencies with no single customer comprising more than 10% of consolidated revenue [S22][S29]. This diversified client composition mitigates major therapeutic concentration risks especially important given frequent consolidation within pharma which could reduce aggregate outsourcing spend or shift vendor relationships.

Geographically, the company maintains strength across Americas, Europe/Africa, and Asia-Pacific regions—enabling support for multinational clinical trials subject to diverse regulatory regimes [S21]. Emerging markets exposure provides incremental avenues during phases of increased pharma global expansion though these geographies introduce operational challenges in compliance adherence.

Therapeutic concentration risk remains under watch given the industry's tilt towards high-price specialty drugs requiring rigorous value demonstration through health economics analytics — areas where IQVIA’s domain expertise is particularly suited but competition also intensifies through smaller niche analytics providers leveraging emerging generative AI tools externally sourced by clients [S22][S13].

Forward-Looking Commentary from Recent Earnings and Corporate Guidance

In its Q4 FY2025 earnings call the company highlighted continued investment behind its Connected Intelligence framework melding extensive data coverage with AI-powered platforms emphasizing responsible AI use consistent with regulatory expectations [N2][N6]. Management projects sustained double-digit revenue momentum driven by expansion into next-generation real-world evidence applications alongside digital commercial engagement tools.

No explicit numeric guidance quantifying full-year FY26 consensus was disclosed publicly in the excerpts reviewed; however analysts are advised to monitor updates on contract wins within accelerated oncology program trials plus broader uptake of subscription-based SaaS licenses fueling recurring revenues [N3][N6].

Balance Sheet Strength and Debt Structure: Financing Innovation Sustainably

IQVIA manages a layered debt profile consisting principally of multiple senior secured term loans bearing floating interest rates indexed to U.S Dollar Term SOFR plus incremental spreads ranging approximately from +125 to +175 basis points depending on tranche tenor maturity extending through early next decade [S4][S14]. Revolving credit facilities augment liquidity flexibility providing $2 billion borrowing capacity at similar margin terms contributing to prudent financial covenant compliance documented quarterly.

The long-term debt principal outstanding approximated $15 billion as of late FY25 quarter-end with staggered maturities spread from remainder of calendar year through beyond 2030 ensuring refinancing risk dispersion [S16][S18]. Negative implications from rising interest rate environments are partially mitigated by fixed coupon senior notes issued in mid-2020s timeframe adding balance sheet stability.

Liquidity management prioritizes ongoing capital expenditures around $600 million annually supporting technology platform enhancements alongside selective acquisitions enhancing competitive positioning without materially jeopardizing leverage targets or operational cash flows [F1][S26].

Capital Stewardship: Buybacks, Dividends, and Return on Equity Trends

IQVIA demonstrates shareholder capital discipline reflected by robust buyback activity totaling approximately $1.24 billion for FY2025 following similar levels prior years while maintaining dividend distributions aligning with sustainable payout ratios conducive to funding innovation investments [F1][S8].

The company maintains an impressive approximate return on equity near 20.9%, underscoring efficient use of equity capital relative to net income generation despite the substantial intangible assets embedded in its data infrastructure base [F1]. Free cash flow metrics remain healthy with roughly $2 billion annually after capex reflecting strong operational cash conversion essential for supporting both organic growth initiatives and shareholder returns.

Historically consistent repurchase programs have modestly offset dilution effects from employee compensation plans while preserving balance sheet flexibility—an approach well regarded for fostering long-term investor value creation.

Regulatory Environment and Litigation Risks Impacting Operational Resilience

Alongside expanding business complexity stems mounting regulatory scrutiny particular to handling sensitive personal health information across multiple jurisdictions requiring strict adherence to data privacy laws such as GDPR in Europe or HIPAA standards in the US heavily impacting IQVIA’s operations given its vast healthcare databases [S9][S22]. Disruptions stemming from alleged non-compliance could prompt costly investigations or suspension of services detrimental financially and reputationally.

A prominent legal matter involves ongoing litigation commenced in January 2017 against Veeva Systems alleging unlawful use of IQVIA’s intellectual property encompassing proprietary datasets critical to competitive differentiation [S5][S9]. The dispute escalated through counterclaims citing anticompetitive conduct emphasizing the high stakes nature of safeguarding trade secrets tightly entwined with tokenization safeguards employed internally preventing unauthorized re-identification.

While management does not currently anticipate material adverse impacts from pending litigations based on latest disclosures, unpredictable resolutions could trigger expense volatility or operational constraints necessitating close monitoring throughout anticipated multi-year court proceedings timelines [S10].

Key Metrics to Monitor: Cash Flow Health and Efficiency in Execution

Operating cash flow (CFO) displayed a slight decline (-2.3%) year-over-year reaching approximately $2.65 billion for FY2025 as reported in filings reflecting manageable working capital shifts although flags potential efficiency headwinds tied to scaling resource demands amid digital platform maturation phases [F1][N3]. Capital expenditures held steady at around $603 million aligned closely with previous years reinforcing maintenance plus incremental spend balance calibrated toward agile technology improvements without unduly pressuring cash conversion ratios.

Going forward stakeholders should assess productivity gains realized through AI-enabled clinical trial accelerations impacting gross margins particularly within Research & Development Solutions where higher complexity incurs notable variable costs yet agility confers win opportunities leveraging real-world data insights for trial optimization [F1][N3].

Profitability sustainability will hinge upon successful integration of dispersed data sets fueling actionable insights while controlling fixed cost bases amplified by global regulatory compliance overheads—areas where scalabilty innovations with advanced encryption methods may unlock future cost reductions augmenting free cash flow trajectories.

This analysis synthesizes publicly filed financial statements, earnings commentary, and risk disclosures per SEC filings through February 2026 along with recent market news without providing investment recommendations or price forecasts. It aims to present an informed perspective on IQVIA’s operational drivers, competitive positioning based on proprietary data moats combined with financial stewardship practices essential for market participants evaluating the life sciences services sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments