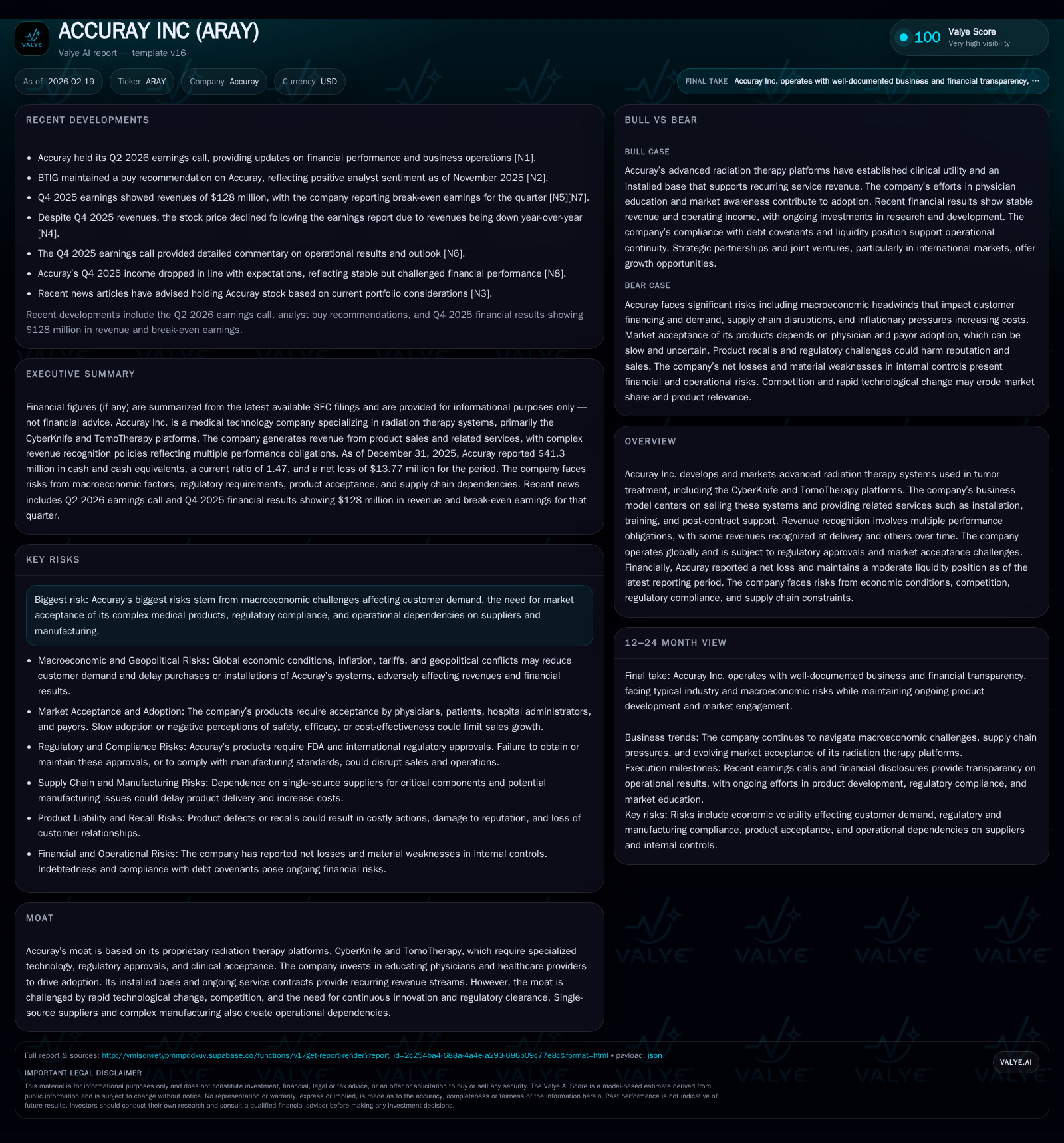

Accuray Inc. Recalibrates Profitability with Innovation-Driven Revenue Streams

Accuray’s proprietary radiation therapy platforms CyberKnife and TomoTherapy underpin its evolving financial and operational profile amid regulatory and market dynamics.

Accuray Inc., specializing in advanced radiation therapy systems, has shown signs of operational leverage through a rebound in operating income despite ongoing net losses. Its growth drivers center on the dual-platform strategy leveraging CyberKnife and TomoTherapy systems combined with global service contracts that generate recurring revenues. The company navigates regulatory complexities and innovation challenges, especially around AI integration and evolving FDA clearances. Capital structure constraints from recent debt facilities underscore careful liquidity management. While free cash flow remains under pressure due to steady capex needs, early traction on buybacks has ceased as innovation and regulatory milestones take precedence. Investors should monitor upcoming refinancing events and clinical adoption progress as key future catalysts.

Historical Financial Trajectory: Resilience Through Product and Service Mix

Accuray Inc.’s multi-year financial data highlight a firm navigating the complexity of selling high-technology radiation therapy systems intertwined with service contracts that yield recurring revenues. In fiscal year 2025 (ending June 30), the company reported an operating income of $7.8 million compared with a marginal $0.5 million in FY24 — a substantial year-over-year increase of approximately 1455% [F1]. Despite this improvement in operating profitability, Accuray continues to report net losses though significantly narrowed at −$1.6 million for FY25 versus −$15.5 million one year prior.

Revenue has broadly stabilized around $114 million (based on most recent disclosures), anchored by product sales primarily related to its CyberKnife and TomoTherapy platforms combined with incremental contributions from installation services, physician training programs, post-contract support and maintenance agreements [F1][S1]. This multi-element revenue mix introduces nuances in the timing of revenue recognition: product sales generally trigger upfront revenue recognition upon delivery while associated services extend over contract periods generating deferred revenue streams [S1]. As such, Accuray’s financial results reflect both discrete system sales volatility as well as more predictable service-based revenue.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 3 | 8 | 4 | +89.8% |

| 2024 | -16 | -12 | 1 | 4 | -67.5% |

| 2023 | -9 | 16 | 2 | 13 | -73.6% |

| 2022 | -5 | -2 | 8 | 5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -1 | -2.0 | |

| 2024 | -16 | -34.5 | |

| 2023 | 0 | 3 | -17.3 |

| 2022 | 0 | -7 | -10.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue disclosed only up to FY2018; recent annual revenue approximated from disclosures.

Core Drivers Behind Revenue Growth and Operating Income Expansion

Accuray's growth trajectory is tightly linked to the performance of its proprietary radiation therapy system platforms: CyberKnife, which specializes in stereotactic radiosurgery for tumors with sub-millimeter precision leveraging real-time imaging guidance; and TomoTherapy, focused on intensity-modulated radiation therapy combining CT imaging technology within the delivery platform [N1][S1]. These platforms benefit from long development cycles requiring sustained R&D investments, regulatory clearances across multiple jurisdictions including FDA approval pathways, as well as effective physician education programs supporting clinical adoption.

Central to Accuray's revenue model is the intricate multi-element contract structure comprising initial equipment sales recognized at point-of-delivery; extended warranty obligations; physician training courses often bundled or separately provided; ongoing maintenance service contracts; plus consumables licensing [S1]. The latter creates dependable annuity-style revenue once the installed base expands.

Service agreements are generally month-to-month beyond standard warranty periods reducing cancellability risk yet necessitating continuous customer engagement efforts internationally [S1]. Moreover, significant investments have been directed towards physician education initiatives designed to enhance clinical acceptance of these relatively complex treatment modalities which represent higher capital expenditures by hospitals than traditional radiation devices [N1]. This also acts as a moat through technology expertise dissemination.

Innovation and Regulatory Hurdles Impacting Future Growth Potential

Innovation remains at the core of Accuray's strategic imperative given intense competition from established radiotherapy modalities—including linear accelerators from larger incumbents—and rapid technological evolution in tumor treatment approaches [S6][S7][S8]. A rising element involves implementation of artificial intelligence both within internal manufacturing processes—to anticipate machinery part failures through predictive analytics—and externally embedded within products enhancing treatment personalization or workflow automation [S7][S12].

However, integrating AI technologies introduces nuanced regulatory scrutiny amid an evolving legal landscape at domestic (FDA regulations) and international levels (European Union AI Act framework). Compliance demands frequent updates to design controls, validation documentation and robust risk mitigation particularly regarding privacy protections given patient health data involvement [S7][S12]. Regulatory delays or requirements for extensive clinical data to demonstrate safety efficacy can stall time-to-market or product upgrades leading to financial drag.

The nature of Accuray’s products—complex medical devices incorporating laser technologies regulated under electronic product radiation control provisions—subjects them to periodic FDA inspections that can temporarily disrupt production if non-compliance issues arise [S18]. Maintaining compliance with ISO quality standards additionally requires rigorous supplier audits due to single-source suppliers for critical components which themselves carry risks impacting production continuity [S11][S18].

Evaluating Market Acceptance Challenges in a Competitive Radiotherapy Sector

A critical risk facing Accuray lies in securing broad market acceptance owing to both the technical complexity of its therapeutic systems and competitive displacement risks from alternative tumor treatments including emerging proton beam therapies or improved linac solutions enhanced by AI-driven capabilities [S9][S27]. Healthcare industry consolidation accelerates bargaining power concentration among purchasers creating pricing pressures damaging average selling prices.

Sales variability quarter-over-quarter is partly attributable to lengthy procurement cycles requiring capital approvals by hospitals amid budget constraints made more acute by uncertain reimbursement policies under public/private payors [S29]. Additionally, heightened tariffs imposed by governments notably between U.S.-China can disrupt cost structures or reduce sales volume particularly given China's sizeable healthcare market opportunity [S9].

Furthermore, third-party payor coverage intricacies critically influence procedure volumes utilizing Accuray’s platforms since insufficient reimbursement levels may limit hospital willingness to invest or promote treatments performed with CyberKnife/TomoTherapy devices [S27][S29].

Capital Structure Evolution and Covenants Influencing Financial Flexibility

On June 6, 2025, Accuray consummated a new senior secured credit agreement featuring a $150 million term loan facility (due June 2030), complemented by a $20 million delayed draw term loan facility plus a $20 million revolving credit facility—all subject to customary restrictive covenants governing leverage (not exceeding approximately 5.25× total leverage ratio), fixed charge coverage ratios, monthly liquidity requirements plus restrictions on incurring liens or additional indebtedness among others [S4][S10][S19][S20][S26].

At mid-2025 reporting date no amounts were drawn under the revolving credit line though availability exists contingent upon compliance with financial covenants; notably proceeds under delayed draw facility may be tapped specifically to retire outstanding convertible notes due mid-2026 totaling approximately $18 million principal amount [S4][S10][S26].

Interest terms offer options between SOFR+8.50% floor rate or alternative reference rates roughly around ~7.50%, alongside a PIK interest feature permitting capitalization of up to an additional ~6% interest annually raising effective financing costs which need careful cost-benefit consideration in future refinancing scenarios [S4].

This capital structure enhances liquidity support but imposes tight monitoring requirements on operating metrics affecting covenant compliance—highlighting moderate current liquidity ($41 million cash plus equivalents) juxtaposed against sizable near-term current liabilities (~$199 million) posing refinancing execution risk that must be closely managed given past covenant waiver history under legacy credit facilities [F1][S10][S13].

Cash Flows, Capital Expenditure, and Their Implications on Free Cash Flow

After experiencing meaningful fluctuations historically—including negative operating cash flow years such as FY24 (−$11.9M)—FY25 shows a modest return to positive operating cash generation ($2.86M) reflecting operational improvements aligned with margin gains [F1]. Nevertheless free cash flow remains negative due primarily to consistent capital expenditure outlays ($4.27M FY25) directed mainly towards maintaining complex manufacturing infrastructure vital for producing precision radiation devices along with ongoing software development costs linked to clinical research collaborations worldwide [F1][S21].

Capex intensity remains elevated relative to cash generation capacity typical for technology-intensive medical device developers managing product life cycle upgrades while also facing component supply chain challenges requiring automation investments increasing fixed asset bases [F1][S21].

Continued investment into property plant equipment apart from depreciation schedules is necessary not only for sustaining existing platforms but also for incremental AI integration modules supporting predictive maintenance capabilities underscoring capital discipline's tension between innovation funding priorities versus short-term liquidity preservation.

Shareholder Returns: Absence of Dividends but Early Buyback Insights

Accuray has not implemented dividend payments historically nor recently based on available SEC XBRL data suggesting all available capital is being redirected into operations or debt servicing obligations rather than returning wealth directly to shareholders via dividends or other distributions [F1].

Stock repurchase activity was material only in FY21 ($14 million buybacks noted), but no repurchases have occurred since fiscal year ending June 2023 indicating strategic emphasis shifted away from share price support towards capital conservation amid operational turnaround efforts plus impending debt maturities requiring prioritized liquidity allocation [F1].

This lack of direct shareholder distributions aligns with the company’s stage focusing on growth via innovation-driven top-line expansion before committing excess free cash flows toward returns policy decisions.

What to Watch: Milestones, Product Development, and Debt Refinancing Risks

Moving forward several key developments will substantially influence Accuray’s trajectory:

- Refinancing Milestones: Convertible debt outstanding matures June 2026 with partial exchange programs concluded but significant principal remaining (~$18M). Accessing delayed draw term facilities per covenant limits poses refinancing execution risk amidst volatile credit markets demanding close monitoring by stakeholders [N1][S4].

- Regulatory Approvals: Progression through FDA clearance pathways for enhancements/modifications including AI-enabled features will dictate commercial ramp-up feasibility particularly as regulatory frameworks evolve rapidly increasing compliance stringency [S6][S7][S8].

- Market Penetration: Clinical adoption rates of CyberKnife/TomoTherapy systems remain pivotal especially securing payor reimbursements amid tightening healthcare budgets globally determining sustainable organic revenue growth opportunities.

- Operational Execution: Meeting internal productivity benchmarks improving operating leverage while managing supply chain constraints involving single source components will be essential for margin expansion beyond recent improvements.

- Competitive Positioning: Maintaining technological differentiation amid proliferating radiotherapy innovations including proton therapies or enhanced linac variants accompanied by aggressive pricing strategies might pressure share gains reducing bargaining power over time.

Investors should prioritize tracking quarterly order book developments reflective of demand elasticity alongside updates shared during earnings calls/conferences elucidating responses regarding emerging regulations around AI use in medical devices along with management commentary around capital allocation trends including potential future share repurchases or dividend initiation.

Disclaimer: This analysis is provided solely for informational purposes without any recommendation or solicitation for investment decisions related to Accuray Inc., relying exclusively on publicly available filings dated up to February 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments