ARRAY Digital Infrastructure’s Post-Transformation Growth and Leverage Challenges

Exploring ARRAY’s strategic refocus on tower leasing post-divestiture, financial shifts, and critical leverage considerations shaping its outlook.

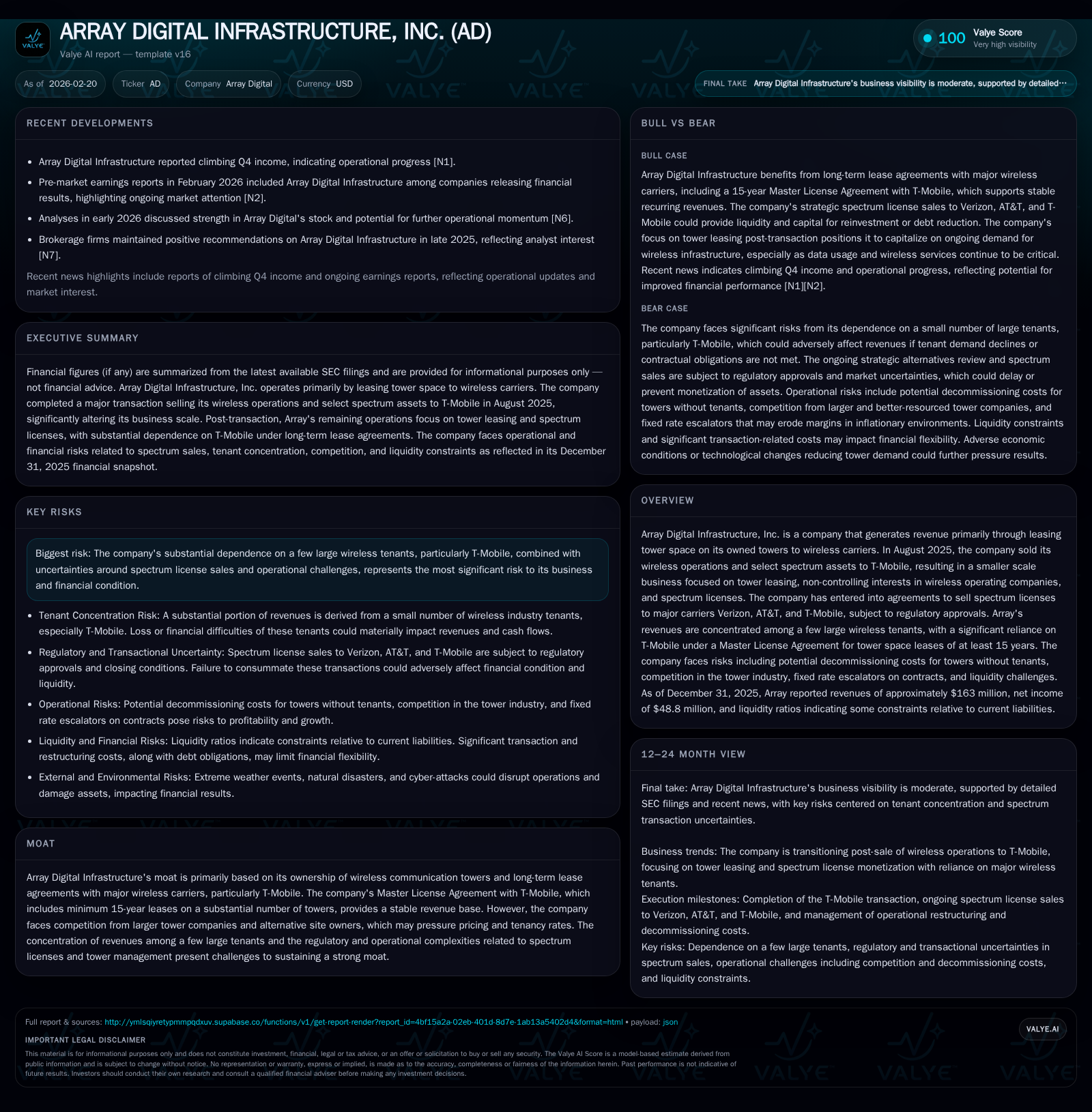

ARRAY Digital Infrastructure dramatically shifted its business model in August 2025 by selling wireless operations and spectrum assets to T-Mobile, pivoting to a leaner tower leasing enterprise. This transition triggered a staggering revenue contraction alongside a net income rebound, underpinned by long-term leases with T-Mobile and other major tenants. The company’s refinancing moves reduced debt burden but introduced covenant constraints amid uncertain spectrum sales and decommissioning obligations. Monitoring spectrum transaction completions, tenant stability, and liquidity will be pivotal to assessing ARRAY’s recovery path.

From Wireless Operations to Tower Leasing: A Strategic Pivot

In August 2025, ARRAY Digital Infrastructure implemented a transformational restructuring through the sale of its wireless operations and select spectrum assets to T-Mobile [S1][S2]. This pivotal transaction radically shrank ARRAY's business scope from a vertically integrated wireless operator to a focused provider of wireless infrastructure — primarily ownership of towers leased out to wireless carriers.

The divestiture had immediate operational reverberations: the company's revenues pivoted almost exclusively towards leasing space on its owned towers under long-term agreements, notably the Master License Agreement (MLA) with T-Mobile which mandates minimum lease terms of 15 years. Additionally, ARRAY retained non-controlling interests in several wireless operating partnerships and held spectrum licenses slated for sale pursuant to agreements with Verizon, AT&T, and T-Mobile [S2].

This new structure introduced complexities including elevated restructuring expenses, contingent advisory fees related to ongoing asset disposals, and uncertainty regarding usage of remaining towers without tenants—some may require costly decommissioning due to lease expirations or tenant relocations [S2]. Operationally, this smaller footprint necessitated recalibrated cost structures while relying heavily on the scale and commitment embedded in the MLA.

Revenue Collapse and Profitability Rebound: Understanding FY2025 Financials

The financial impact of the transformation was dramatic in FY2025. Annual revenue plummeted from $3.77 billion in FY2024 to $163 million in FY2025—a year-over-year collapse of approximately 95.7% [F1]. This stark drop reflected both the divestiture removing high-revenue operating segments and the narrowed focus on tower leasing activities.

Operating income swung more negative—from an already modest loss of $12 million in FY2024 deep into an operating loss of $92.5 million for FY2025 [F1]. This deterioration incorporated restructuring charges associated with the divestiture and a significantly smaller operational base.

In contrast, net income swung positively to $48.8 million (a 225% improvement over prior year losses), driven mainly by gains from discontinued operations upon sale closure and favorable tax effects arising from valuation allowances linked to asset sales [F1][N5].

Operating cash flows remained robust at approximately $201 million despite revenue shrinkage—a reflection of reduced working capital needs post-sale and efficient cash conversion from recurring tower leases [F1]. Capital expenditures contracted sharply by roughly 95%, underscoring the scaled-back asset investment strategy now centered on maintenance rather than network expansion [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0.2 | 49 | 201 | -93 | -95.7% | +225.0% |

| 2024 | 3.8 | -39 | 883 | -12 | -3.5% | -172.2% |

| 2023 | 3.9 | 54 | 866 | 139 | -6.3% | +80.0% |

| 2022 | 4.2 | 30 | 832 | 69 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 21 | 174 | 1.9 |

| 2024 | 54 | 346 | -0.9 |

| 2023 | 0 | 258 | 1.2 |

| 2022 | 43 | 230 | 0.7 |

Source: SEC companyfacts cache [F1].

*Note: All figures for FY2025 reflect post-divestiture operations focused on tower leasing [F1].

Operational Footprint Post-Divestiture: Stability via Long-Term Leases

Post-sale operations revolve predominantly around the MLA with T-Mobile, which anchors ARRAY’s financial stability through committed leases spanning at least fifteen years on numerous towers [S2][S13]. This agreement mitigates churn risk inherent in colocation contracts common in telecommunications infrastructure.

However, ARRAY's customer base is highly concentrated among a small number of large carriers including Verizon and AT&T as secondary tenants [S11][S18]. Such concentration elevates counterparty risk — loss or downsizing by any major tenant could disproportionally affect revenue streams.

Industry practice often includes fixed rate annual escalators within tower lease contracts; ARRAY notes that these escalators are predominantly fixed rather than CPI-linked [S11]. Over extended timeframes of these agreements, this creates potential margin pressure if inflation outpaces contractual escalations or operating cost inflation accelerates faster than revenues.

Competitive dynamics remain challenging as ARRAY confronts larger tower operators with more extensive nationwide portfolios offering broader location options to tenants—a structural disadvantage that may limit pricing flexibility or between-tower tenancy expansion [S11].

Spectrum License Transactions: Pending Sales and Regulatory Hurdles

Complementing tower leasing revenues are proceeds anticipated from licensed spectrum sales under agreements entered into with Verizon, AT&T, and T-Mobile [N1][S2]. These transactions remain contingent on regulatory approvals by entities including the FCC and antitrust bodies.

Regulatory approval status thus introduces timing uncertainty surrounding significant capital inflows that would enhance ARRAY’s liquidity profile or enable further debt reduction or shareholder returns [S2][N1]. Moreover, these sales likely trigger contractual provisions reducing revolving credit capacity once cumulative license proceeds reach $500 million [S6][S8].

The successful closing of these deals remains critical—failure or delay could maintain pressure on liquidity metrics and increase financial leverage risks.

Capital Structure Transition: Debt Refinancing and Liquidity Profile

Following the divestiture closes in August 2025, ARRAY undertook notable refinancing steps:

- Fully repaid legacy term loans totaling approximately $713 million [S8], substantially deleveraging initial debt stacks.

- Entered a new term loan facility with CoBank borrowing $325 million at SOFR +2.50%, maturing June 2030 [S8].

- Maintains an unsecured revolving credit facility ($300M max borrowing), unused as of September but restricted by covenants tied to proceeds from spectrum license sales [S6][S7][S15].

Financial covenants impose a Consolidated Leverage Ratio ceiling of ≤3.5x net debt/EBITDA and interest coverage ratio ≥3x quarterly [S8][S15]. At September quarter-end metrics showed compliance amid restructuring effects.

Cash balances stood at $113 million at fiscal close—providing reasonable runway though further spectrum sale proceeds are critical for broader capital strategy flexibility [F1][S6].

Asset retirement obligations escalated slightly due to reassessed future decommissioning estimates related to non-leased towers—an emerging contingent liability that requires careful monitoring [S7].

Shareholder Returns Amid Transformation: Buybacks, Dividends, and ROE

Capital return activity slowed substantially as ARRAY navigated its transition:

- Approximately $21.4 million deployed on share repurchases in FY2025—a marked decrease reflecting caution during strategic realignment [F1][S27].

- No dividends declared post-divestiture; previous special dividend of $23/share was paid concurrent with transaction closing but no recurring payments are evident in recent filings [S25].

- Return on equity modest at ~1.9%, commensurate with limited retained earnings growth against reduced equity base amid restructuring effects [F1].

These patterns indicate conservative capital allocation reflective of balance sheet repair priorities over shareholder yield enhancement currently.

Navigating Tenant Concentration Risk and Decommissioning Obligations

Twenty-first century telecommunications infrastructure companies increasingly face tenant concentration challenges; ARRAY exemplifies this with dependency on T-Mobile’s MLA obligations covering large portions of its portfolio [S11][S13]. This dependency means any tenancy interruption could produce outsized revenue volatility.

Furthermore, towers without current tenants pose asset retirement cost risks stemming from dismantlement efforts inclusive of ground lease obligations—creating financial downside contingent claims that could impact future free cash flow profiles [S2].[S7]

What to Watch: Milestones and Risks in the Near Term

Investors and analysts should monitor:

- Progression towards closing spectrum license sales fully approved by relevant regulators – critical inflection point for capital structure adjustments [N1][S2].

- Compliance with covenant thresholds tied directly to leverage ratios given volatile trailing earnings metrics could precipitate restrictions or refinancing needs [S15].

- Tenant retention under key MLA leases espoused by T-Mobile as well as renewal rates across secondary customers amidst growing industry competition [S11].[S18]

- Evolution of restructuring costs trajectory which continues beyond deal close impacting operating income potential near term [N5].[S2]

- Developments concerning asset retirement obligations size estimates aligned with actual tower retirements executed post-divestiture.

Analysis Summary:

ARRAY Digital Infrastructure's refocused business model embraces an asset-light tower leasing platform fortified by long-term tenant commitments but faces elevated operational risks linked to tenant concentration combined with regulatory dependencies affecting spectrum monetization timing. The company’s prudent management of capital structure combined with robust operating cash flows provide constructive footing; however, lingering liabilities related to asset retirements alongside competitive sector dynamics require attentive oversight. Going forward, realization of pending spectrum deals paired with stable tenancy execution will largely dictate whether growth ambitions clear structural leverage challenges inherent in post-transformation phases.

Disclaimer: This analysis is informational only and does not constitute investment advice or recommendation regarding buying or selling securities associated with Array Digital Infrastructure. All data presented is derived explicitly from cited sources as of report date February 20, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments