Kenvue’s Earnings Surge and Strategic Merger: Charting Consumer Health Leadership

Kenvue’s robust financial performance post-spinoff pairs with a transformative merger on the horizon, redefining its role in consumer health.

Since its 2023 separation from Johnson & Johnson, Kenvue has demonstrated impressive earnings growth fueled by operational efficiencies and strategic marketing investments. The company’s global leadership in consumer health is anchored by a portfolio of iconic brands and a digitally enhanced supply chain. With shareholder approvals secured, the pending Kimberly-Clark merger introduces potential scale benefits but remains contingent on regulatory clearance. Investors should watch for execution on operational milestones and regulatory developments while monitoring evolving risks tied to litigation and supply chain dynamics.

Historical Financial Performance Highlights and Key Drivers

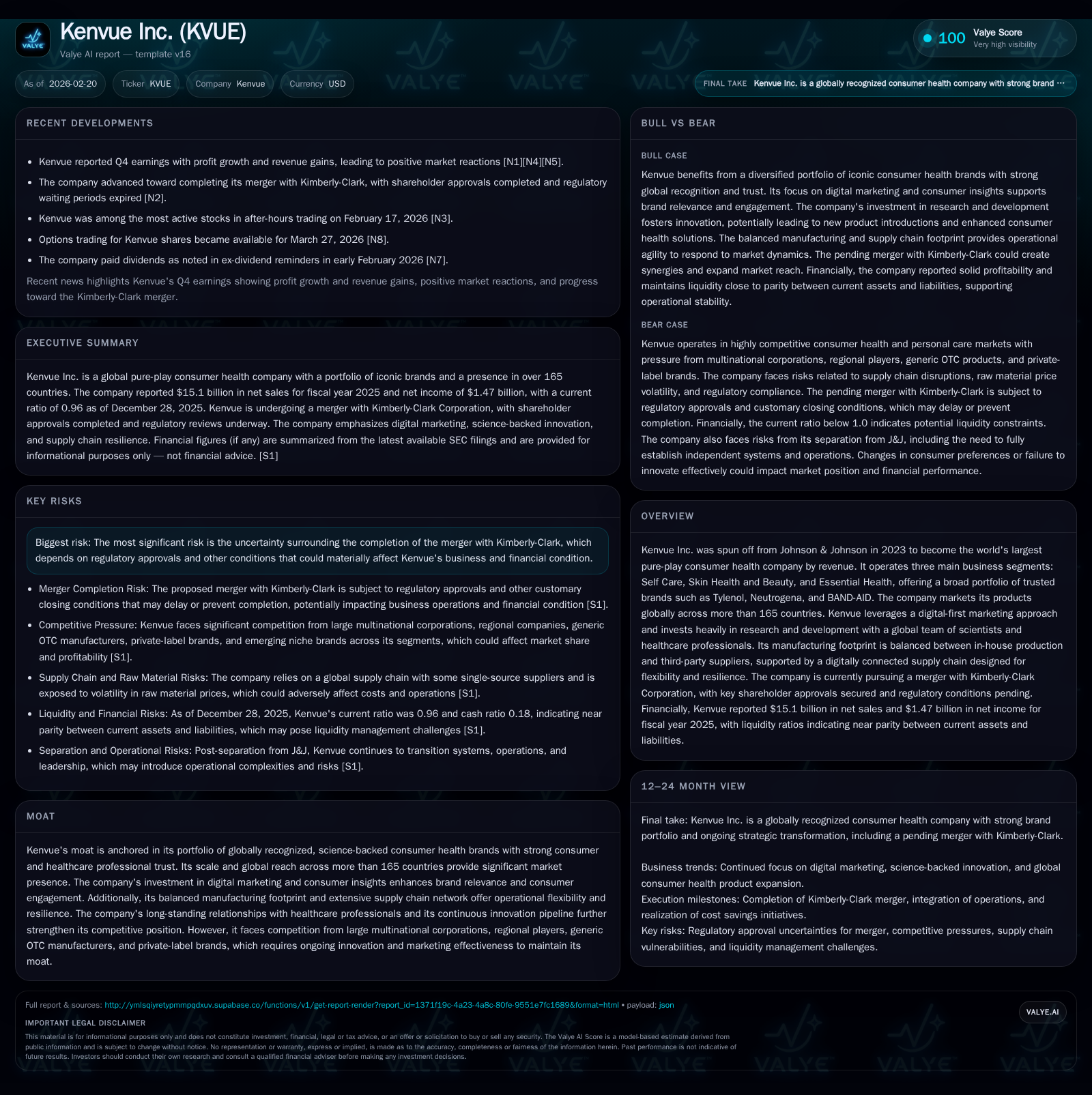

Kenvue has showcased an impressive trajectory in its initial years as a standalone entity following its spinoff from Johnson & Johnson in 2023. Operating income fell slightly from $2.51 billion in FY2023 to $1.84 billion in FY2024 but surged by 31.1% to $2.41 billion in FY2025 [F1]. This rebound signals successful operational adjustments post-separation. Net income followed a more pronounced upward path, expanding from $327 million in FY2023 to $1.03 billion in FY2024 and then soaring 42.7% to $1.47 billion in FY2025 [F1].

Operating cash flow experienced a significant drop post-spinoff from a peak of $3.17 billion in FY2023 down to $1.77 billion in FY2024 but stabilizing with a 24.2% recovery to $2.20 billion by FY2025 [F1]. Capital expenditures have been managed tightly, hovering near $475 million in the latest fiscal year, marginally above prior years reflecting moderate reinvestment into plant and equipment [F1]. Meanwhile, dividend payments doubled since the IPO year to $1.58 billion in FY2025 while share repurchases remain conservative relative to cash flows at about $197 million last year [F1].

Underlying these improvements are enhanced marketing effectiveness and cost discipline initiatives contributing to increased profitability margins.

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1470 | 2.2 | 2.4 | 475 | +42.7% |

| 2024 | 1030 | 1.8 | 1.8 | 434 | +215.0% |

| 2023 | 327 | 3.2 | 2.5 | 469 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 1581 | 197 | 1.7 |

| 2024 | 1552 | 235 | 1.3 |

| 2023 | 766 | 2.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; YoY calculations based on available metrics only.

Post-Spinoff Operational Transformation and Digital Strategy

Separation from J&J compelled Kenvue to rapidly modernize and fully own its operating model [S1]. A key thrust has been scaling precision marketing capabilities that harness advanced data analytics tailored to consumer behavior insights — elements critical for targeting efficacy within highly competitive OTC categories.

The company emphasizes e-commerce analytics integration alongside traditional retail channel management, aligned with broader industry trends where direct-to-consumer digital engagement increasingly drives brand loyalty metrics.

Supply chain digitization efforts enable an agile manufacturing footprint balanced between owned plants and third-party suppliers globally; this flexibility mitigates disruptions while supporting customized demand fulfillment across regions [S1]. Such capabilities enhance responsiveness that is vital amid growing retail alliance bargaining power and consumer preference volatility [S16].

Growth Strategy and Market Positioning in Consumer Health

Kenvue operates through three major segments: Self Care, Skin Health & Beauty, and Essential Health — encompassing iconic brands like Tylenol, Neutrogena, and BAND-AID that cumulatively reach consumers across more than 165 countries worldwide [S1,S16]. The breadth facilitates geographic diversification while mitigating dependence on any single market.

Investment in R&D is underpinned by collaboration with healthcare professionals whose endorsement provides scientific validation bolstering brand equity [S18]. This moat is critical given increasing challenges from generic OTC players and private-label competitors pressing price points globally.

Brand relevance is maintained through continuous innovation pipelines driven by multi-disciplinary science teams integrating consumer insights into product evolution — a hallmark of Kenvue's approach designed to offset commoditization risks prevalent in mature OTC markets.

Merger Progress and Regulatory Considerations

The transformational merger with Kimberly-Clark Corporation marks a pivotal event for Kenvue’s strategic roadmap, promising expanded scale advantages and cross-segment synergies [N1,N3]. Shareholder approvals have been secured affirming investor alignment behind the deal terms.

However, regulatory approvals remain pending — notably sensitive given antitrust scrutiny common for consolidations combining two consumer goods giants [S5,S6]. This regulatory uncertainty introduces material risk potentially impacting near-term business continuity plans.

Integration complexity will require meticulous planning considering cultural fit alongside supply chain harmonization challenges intrinsic to merging large multinational operations.

Capital Allocation: Dividends, Buybacks, Cash Flow, and ROE Analysis

Kenvue balances capital return priorities prudently against reinvestment imperatives tied to growth transformation programs [F1]. The company annually doubled dividends paid from approximately $766 million at spinoff year end (FY2023) to $1.58 billion in FY2025 — supporting attractive yield profiles for income-focused shareholders.

Modest stock buybacks compared with dividends reflect either cautious capital deployment amid the pending merger or strategic preservation of liquidity as highlighted by current ratio below parity at about 0.96 indicating tighter working capital conditions [F1].

Free cash flow generation remains strong at approximately $1.72 billion last fiscal year (operating cash flow minus capex), offering coverage comfortably above dividend distributions ensuring sustainability absent unforeseen shocks [F1]. Return on equity at ~13.7% conveys efficient utilization of shareholders’ equity despite elevated investments into growth initiatives post-separation.

Evolving Risk Landscape: Regulatory, Legal, and Supply Chain Challenges

Operating independently has subjected Kenvue to mounting regulatory scrutiny manifesting through increased compliance complexity spanning multiple jurisdictions including the US FDA, FTC regulations on advertising transparency, European cosmetic product frameworks, China’s OTC product rules among others .

Product liability exposure remains significant with ongoing litigation tied largely to acetaminophen safety allegations as well as previous talc-related claims inherited via J&J separation agreements [S6,S19,S27]. Such legal proceedings entail both financial expenses and reputational risk which management actively monitors.

Supply chain resilience continues under pressure due to reliance on third-party manufacturers amid macroeconomic volatility including inflationary input cost pressures, geopolitical trade controls, and raw material sourcing complexities requiring advanced risk mitigation measures embedded within the digital supply network architecture [S8,S9,S16].

Compliance with anti-corruption laws including FCPA along with emerging human rights legislation also adds layers of governance expectations especially across sprawling global operations posing operational burden yet critical for ethical brand stewardship [S11,S15].

Outlook and What Investors Should Monitor Next

While explicit forward guidance from Kenvue is limited given ongoing merger negotiations [N3], operational milestones such as achieving targeted cost savings under the ‘Our Vue Forward’ restructuring initiative will be key near-term indicators of sustained transformation success [S1].

Market penetration metrics especially within e-commerce channels alongside maturation of digital engagement strategies shall offer insights into durability of revenue growth trajectories post-merger completion or standalone scenarios.

Regulatory developments pertaining to merger approval constitute pivotal catalysts; any delay or unfavorable rulings could induce strategic reroutes impacting financial forecasts.

Additionally, investor attention should remain fixated on legal proceedings outcomes related to OTC product safety claims since adverse rulings could materially influence earnings volatility over coming years.

This report is intended purely for informational purposes and does not constitute investment advice or recommendations regarding Kenvue Inc or any other securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments