Inseego Corp. Streamlines Focus on 5G Wireless Solutions Amid Shifting Revenue Mix and Capital Structure Reshaping

INSG’s pivot away from telematics sharpens its North American 5G product and SaaS focus, balancing growth initiatives with a challenging capital structure.

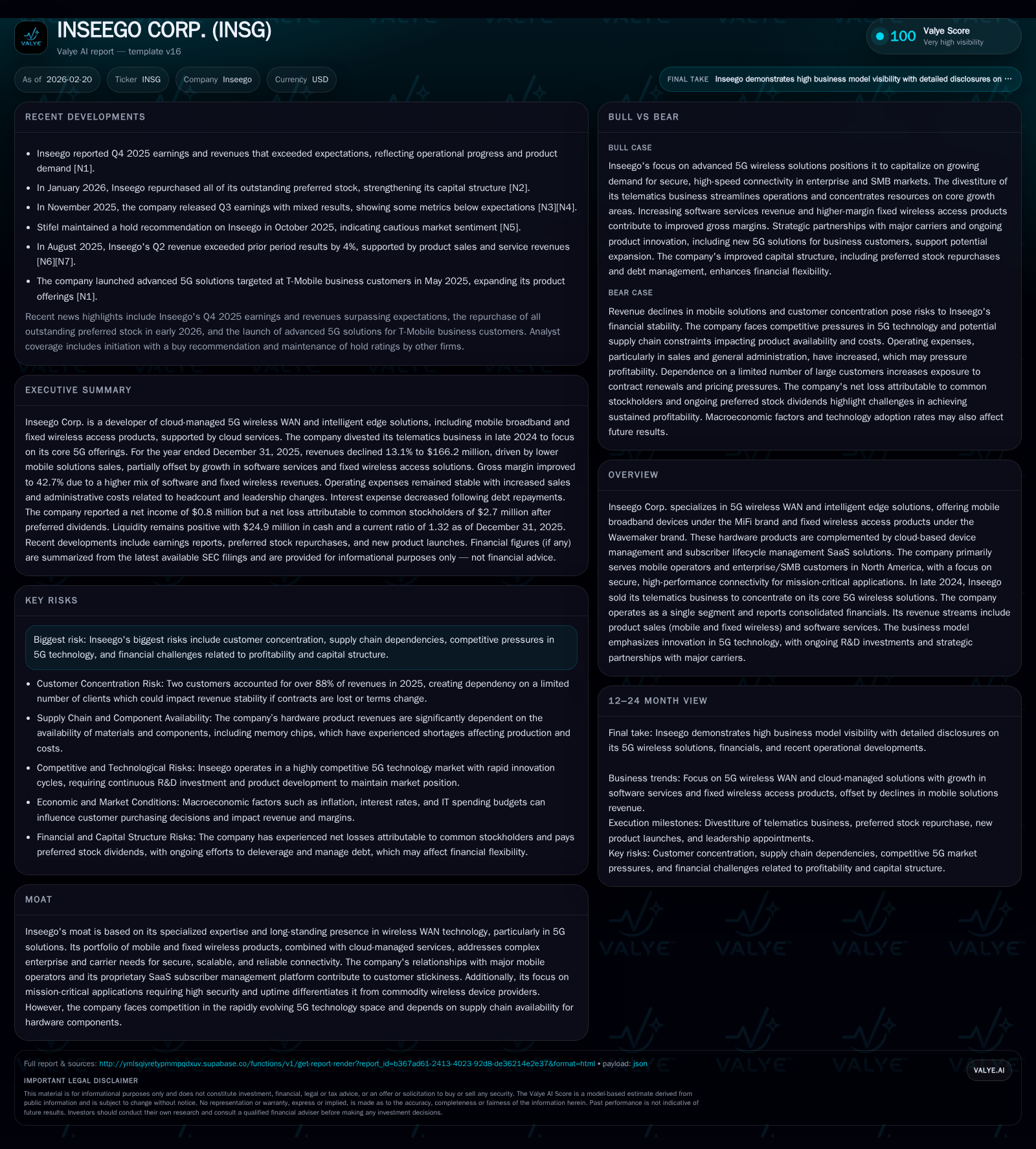

Inseego Corp. has realigned its strategic focus towards its core 5G wireless solutions business, divesting legacy telematics operations in late 2024 to emphasize mobile broadband and fixed wireless access solutions paired with cloud-managed services. Despite a revenue decline versus 2024, driven by reduced mobile solutions sales, higher-margin software and fixed wireless products have supported gross margin expansion. The company’s fiscal year 2025 reflected improving operating income and positive net income, albeit with ongoing customer concentration risks and supply chain dependencies. Capital structure improvements—including repurchasing preferred stock at a discount—have reduced financial overhang as Inseego navigates the competitive and technologically evolving 5G landscape.

Company Background and Strategic Refocus

Inseego Corp., historically known for its leadership in wireless WAN solutions spanning multiple generations of mobile technologies, has renewed its strategic emphasis on North American-centric 5G wireless offerings following the divestiture of its international telematics unit completed in Q4 2024 [S1][S9]. The divestment generated approximately $52 million cash proceeds and allowed the company to concentrate resources on its MiFi-branded mobile broadband devices and Wavemaker fixed wireless access (FWA) routers, alongside cloud-based subscriber management software services ("Inseego Subscribe" and "Inseego Connect") [S1][S16].

The company's target customers are predominantly major US and Canadian carriers — including T-Mobile, Verizon Wireless, AT&T, Rogers, and Telus — supplemented by enterprise and SMB vertical markets requiring mission-critical connectivity tailored for security and high availability [S1][S10]. This niche focus aims to differentiate Inseego from commodity wireless device providers through integrated hardware-software cloud orchestration capabilities that facilitate network visibility and automation.

Historical Financial Performance

Over recent years leading up to fiscal year (FY) 2025, Inseego's financials demonstrate transition dynamics shaped by strategic realignment and challenging industry conditions:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1 | 7 | 4 | 661000 | -81.7% |

| 2024 | 5 | 34 | 2 | 100000 | |

| 2023 | 7 | -36 | 704000 | ||

| 2022 | -68 | -33 | -58 | 1481000 | -41.2% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 7 | -20.7 |

| 2024 | 33 | -35.6 |

| 2023 | 6 | |

| 2022 | -35 |

Source: SEC companyfacts cache [F1].

*Full-year data for earlier years limited; detailed only for operating income/net income/CFO/capex when available [F1].

The revenue peak in FY2024 was lifted by stronger mobile solutions sales partially driven by market adoption of earlier product generations [S16]. However, declining mobile solutions revenues (-31%) in FY2025 reflect saturation pressures or shifts toward newer models not yet fully ramped [S23][S24]. Fixed wireless access revenue grew modestly (+4%) during this period, contributing nearly 30% of total sales now [S24], while software services revenue rose approximately $3.8 million year-over-year owing mainly to an extended CSP subscriber lifecycle management contract secured mid-2024 [S24].

Gross margins expanded to nearly 43% in FY2025 from 36% in FY2024, underscoring the impact of the higher-margin subscription software uplift combined with improved product mix [S24]. Cost of goods sold benefited from controlled product manufacturing costs despite inflationary concerns around component pricing [S23].

Operating expenses shifted slightly lower overall (-0.6%), with R&D expenditure stable at roughly $19.8 million or ~12% of revenues; increased sales & marketing spend (+9%) reflected growing headcount investment aimed at capturing new enterprise accounts; meanwhile G&A expenses rose significantly (+20%), likely attributable to ongoing corporate overhead and compliance costs post-divestiture [S26]. Despite these expense pressures, operating profit more than doubled to $4.3 million [F1], supporting the company's trajectory toward sustainable profitability.

Net income remains positive but thin ($0.8 million), partly due to interest expense related to the company's restructured debt profile [S6][S21]. The approximate ROE is negative near -20%, indicating that earnings remain insufficient relative to equity deficit persisting from prior years' losses [F1].

Operating cash flow declined sharply year-over-year from $33.5 million in FY2024 to only $7.2 million in FY2025 due primarily to working capital timing variations including collections on concentrated large customers [F1][S8]. Capital expenditures accelerated to $660K—higher than prior years—as Inseego invests more intensively into developing next-generation hardware platforms nearing production readiness [S27][S26].

Customer Concentration and Supply Chain Challenges

Customer concentration is a notable risk factor: two customers alone accounted for over 88% of revenues during FY2025, up from roughly three customers making up about three-quarters the prior year [S25]. This elevated dependency on a handful of carrier partners amplifies exposure to contract renewals, pricing pressure, or strategic purchasing shifts.

On the supply side, Inseego’s reliance on key component suppliers such as Qualcomm for chipsets underpins production constraints amid global semiconductor shortages that have affected memory chips critical for device function [S25][S23]. While Inseego actively manages non-cancellable purchase obligations upwards of $101 million extending several quarters out, the risk remains if supply disruptions or cost inflation persist without commensurate pricing flexibility.

Recent Capital Structure Developments

A critical near-term catalyst was January 14, 2026’s repurchase of all outstanding Series E Preferred Stock ($42 million liquidation value) at a roughly 38% discount for a combination of cash ($10 million), newly issued common shares (767K), and additional principal on existing senior secured notes ($8 million increase), thereby significantly deleveraging preferred equity obligations [N2][S25].

This move followed iterative reductions in burdening convertible notes culminating with maturity payments on May 1, 2025 clearing remaining balances of the previously outstanding low-interest convertible debt [S6][S8]. As a result, Inseego improved debt maturity profile concentrating into longer-dated ($40-49 million principal range), higher-interest (9%) senior secured notes due May 1, 2029; these notes are backed by first-priority liens on company assets excluding current assets which remain subordinated to revolving credit commitments [S7][S22][S11].

Furthermore, Inseego established a new revolving credit facility with BMO Bank N.A., allowing borrowings up to $15 million secured by eligible accounts receivable and inventory collateralized under typical borrowing base mechanics; no amounts were drawn as of December end-2025 though liquidity remained healthy with about $25 million cash balances/conveniently accessible working capital lines available [S13][S18].

This capital restructuring improves near-term flexibility but introduces obligations for semi-annual coupon interest payments on senior secured notes at relatively high rates alongside potential dilution risks from warrant issuances tied to short-term loans executed previously[S20]. Investors should watch evolving leverage metrics alongside EBITDA or free cash flow improvement as key milestones.

Future Growth Prospects

Growth drivers include:

- Increasing adoption of fixed wireless access technology especially from enterprises seeking alternatives or augmentations to wired WAN connectivity amidst remote/hybrid work trends;

- Expansion of Inseego Subscribe SaaS platform sales toward complex government/enterprise carrier clients managing subscriber lifecycles;

- Continued innovation leadership capturing new spectrum bands or IoT edge applications leveraging latest Qualcomm chipset advances.

Capping factors comprise:

- Limited geographic diversification with essentially all long-term assets and primary customer base within North America constrains scaling avenues;

- Supply chain uncertainties affecting timely product availability or margin compression;

- Highly concentrated customer base incurring meaningful contract negotiation risks;

- Competitive pressure from both larger OEMs offering integrated hardware/software ecosystems alongside emerging private networking players targeting vertical-specific markets.

While explicit management guidance was not disclosed in source materials beyond general forward-looking considerations around deployment cycles and competitive dynamics [N1], industry observers should monitor quarterly revenue splits between Mobile vs Fixed Wireless Access segments along with progression curves for subscriber management SaaS bookings for signs of material inflections.

Capital Allocation & Returns Assessment

Inseego has not declared dividends recently nor engaged meaningfully recently in common stock buybacks given financial reclamation priorities post-detangling from telematics operations [F1].[N2] Capital allocation emphasis has been on debt reduction through exchanges affecting convertible note holders as well as preferred stock repurchase transactions designed to reduce onerous cost layers.[S1][S25]

Free cash flow—estimated here as operating cash flow less capex—stands at roughly $6.53 million for FY2025 demonstrating improving operational efficiency yet meaningfully constrained absolute levels given scale ambitions.[F1]

Shareholders’ equity remains deeply negative although improving thanks largely to net income positivity offsetting accumulated deficit carryforwards—this metric bears watching especially as relates to dilution effects following preferred stock exchanges resulting in common stock issuance.[F1]

Return on equity approximates negative double digits implying residual challenges turning operating profitability into shareholder value creation absent further deleveraging or substantial profit expansion.[F1]

Industry Context Analysis

Within the wireless WAN space focused on enterprise-grade secure connectivity amidst rapid migration toward private networking paradigms—especially those harnessing SD-WAN overlays—the competitive landscape is marked by both telecom incumbents extending their portfolios and innovative startups exploiting cloud-managed edge functionality. Supply chain challenges remain acute globally affecting semiconductor sourcing—a structural industry-wide headwind influencing cost structures beyond Inseego alone. Meanwhile regulatory environments emphasizing security certifications are barriers favoring incumbents like Inseego that hold trusted carrier relationships. Pricing dynamics fluctuate between hardware unit volume declines offset by increasing software service penetration—mirroring broader telco equipment trends toward recurring revenue streams.

Conclusion

Inseego Corp.’s pivot away from legacy telematics toward a sharpened base within North American mobile broadband and fixed wireless access augmented by SaaS device management reflects a coherent strategy focused on sustainable growth areas within wireless WAN networks characterized by managed security demands. Though facing significant challenges—including revenue contraction driven by saturated mobile device markets coupled with heavy customer concentration risks balanced against improving gross margins—the company has made tangible strides bolstering profitability while restructuring financial obligations through preferred stock repurchases and debt refinancing. Close monitoring is warranted regarding performance benchmarks including quarter-to-quarter revenue segmentation shifts, R&D outcomes particularly related to next-generation hardware development progressions, cash flow consistency amid rising capex investments, leverage ratios post capital adjustments, and potential further dilutive effects stemming from share issuances accompanying financing activities. As Inseego navigates these tradeoffs between innovation-led growth investments against disciplined capital stewardship within a dynamic technological environment defined by global supply uncertainties and accelerating digital transformation needs among carriers and enterprises alike—it offers an insightful case study into focused execution within the specialized narrowband connectivity domain.

This analysis does not provide investment advice or recommendations but aims to furnish an informed overview based solely upon publicly available information as cited herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments