Zimmer Biomet's Earnings Slip Highlights Restructuring Impact and Cybersecurity Vigilance

2025 results reflect the financial pressures of Zimmer Biomet's global restructuring while reaffirming robust cybersecurity oversight.

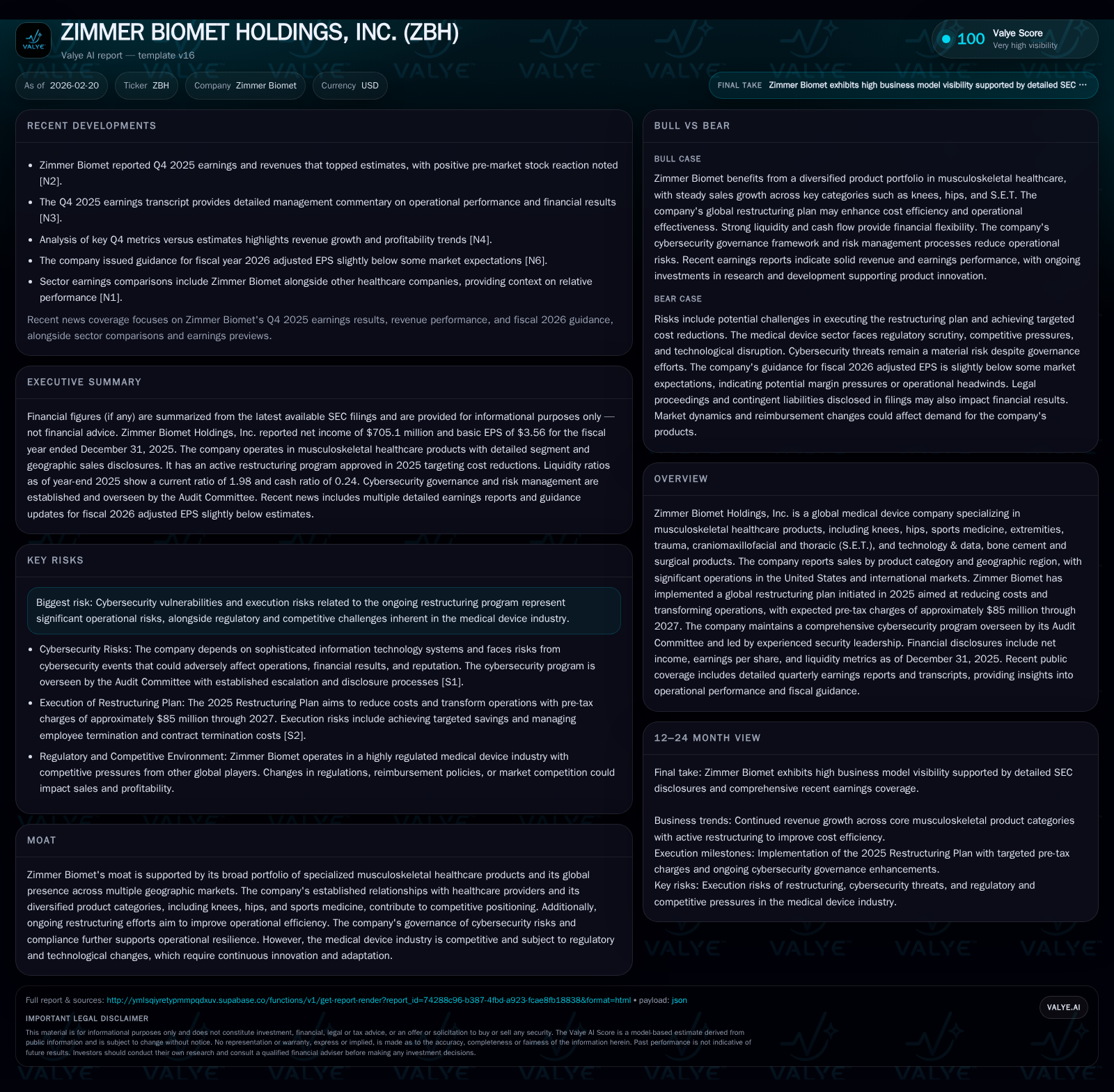

Zimmer Biomet experienced a notable decline in operating and net income in 2025, largely attributed to its ongoing global restructuring plan that anticipates approximately $85 million in pre-tax charges through 2027. Despite the earnings contraction, the company’s diversified musculoskeletal device portfolio maintains competitive positioning across key geographies. Concurrently, Zimmer Biomet has strengthened its cybersecurity governance framework, positioning it to mitigate growing digital risks within the medical device sector. Going forward, operational efficiency gains from restructuring and careful capital allocation underpin the near-term outlook amid competitive and regulatory challenges.

Earnings Trends and Restructuring Effects in 2025

Zimmer Biomet's financial results for fiscal year 2025 reveal significant pressure on profitability driven by its strategic global restructuring initiative launched in early 2025. Operating income dropped from $1.286 billion in FY2024 to approximately $1.098 billion in FY2025, marking a 14.6% year-over-year decline [F1]. This contraction reflects not only ongoing operational challenges but also pre-tax charges estimated around $85 million expected to be recognized through to 2027 [N10][S1]. Net income followed a sharper downward trajectory, decreasing by 22% to about $705 million from $904 million the prior year [F1].

Despite these headwinds, Zimmer Biomet delivered better-than-expected results for Q4 2025 that topped analyst estimates on both earnings and revenue metrics [N2][N3][N4][N5]. The Q4 performance signals disciplined operational control amidst transition phases.

Margins have been particularly impacted as restructuring expenses create short-term earnings dilution even as they are geared to long-term efficiency gains.

Operational Portfolio and Market Positioning in Musculoskeletal Healthcare

Zimmer Biomet's core strength lies in its comprehensive portfolio of musculoskeletal healthcare products that span several high-value segments including knees, hips, sports medicine, extremities & trauma, craniomaxillofacial and thoracic (S.E.T.), as well as related technology & data-driven solutions plus bone cement and surgical products . This breadth diversifies revenue streams and embeds the company deeply within providers’ procedural workflows globally.

A sizable portion of Zimmer Biomet’s business derives from implantable devices that require rigorous clinical validation and regulatory approval, underlining barriers to entry for competitors yet necessitating continuous innovation. The company's presence remains especially strong across the United States—its largest market—and extends into international territories encompassing Europe, Asia-Pacific, and other regions . Such geographic diversity supports resilience against localized disruptions but entails complexities tied to tailored regulatory environments.

Within medical device value chains like Zimmer Biomet’s, integrated offerings combining implants with advanced surgical instrumentation and data analytics tools enable capture of greater procedural value — a competitive advantage difficult to replicate without significant scale and R&D investment.

Cybersecurity Governance as a Pillar of Operational Resilience

Amid escalating cyber threats facing healthcare technology firms, Zimmer Biomet has enhanced its cybersecurity program as a foundational element of operational resilience [S1]. The Audit Committee of the Board directly oversees cybersecurity risk management processes independently but coordinated within overall enterprise risk frameworks.

The company’s VP & Chief Information Security Officer (CISO), who carries over three decades of cross-industry IT security leadership experience, leads a dedicated global information security team responsible for governance, risk compliance (GRC), incident response functions, and continuous threat monitoring [S1]. This team includes personnel with advanced degrees and professional security certifications.

Zimmer Biomet employs a multi-tier disclosure committee structure whereby information security incidents are reviewed by a specialized subcommittee containing representatives from legal, accounting, internal audit and information security disciplines. Material cyber events are promptly escalated to the full Audit Committee per established escalation protocols [S1]. Periodic independent third-party assessments further validate the effectiveness of this layered defense posture.

This comprehensive cybersecurity governance aims to minimize potential financial impacts or reputational harm stemming from evolving digital attack vectors targeting proprietary data or device software integrity.

Future Growth Drivers and Headwinds: Guidance Insights and Market Dynamics

For fiscal year 2026, Zimmer Biomet projects adjusted earnings per share slightly below analyst consensus estimates [N10]. This guidance acknowledges lingering cost pressures from ongoing restructuring initiatives while forecasting incremental efficiency improvements over time.

Key growth drivers center on successful transformation of operations through streamlining global footprints alongside continued innovation across high-demand specialty segments such as joint reconstruction and sports medicine [N10][S1]. Additionally, expansion opportunities remain within technology-enabled care pathways including data analytics platforms linked to surgical outcomes.

However, potential headwinds persist due to intensified competition among orthopedic device manufacturers globally alongside regulatory scrutiny that can delay new product approvals or impose compliance costs—all noted risks within the company's disclosures [S19]. Sustaining R&D effectiveness will be critical given shifting reimbursement paradigms influencing hospital purchasing decisions.

Execution on announced restructuring milestones will be vital; inefficiencies that linger beyond expected timelines could limit margin recovery prospects.

Capital Deployment: Cash Flow Strength, Dividends, and Share Repurchases

Zimmer Biomet ended FY2025 with robust operating cash flow totaling approximately $1.697 billion—a 13% increase year-over-year demonstrating solid underlying business cash generation capacity despite restructuring expenses [F1]. Capital expenditures were moderate at roughly $225 million (+10% YoY), supporting necessary equipment refreshes without excessive investor capital demands.

Subtracting capex yields estimated free cash flow near $1.47 billion for 2025—ample liquidity to fund dividends (~$190 million paid annually) alongside share repurchase programs which contracted noticeably in scale during the latest reporting period from $868 million in FY2024 down to $487 million in FY2025 [F1].

Return on equity stands lower than historical averages at about 5.6%, indicating current profit margins weigh on shareholder returns as restructuring investments rebalance capital allocation priorities [F1]. This return level underscores a transitional phase where capital efficiency is being recalibrated amidst strategic shifts.

Debt management dynamics include senior note issuances/refinancings discussed in prior filings although no material changes were highlighted as immediate near-term risks [S6]. Maintaining leverage discipline remains essential during this transformative period.

Key Metrics Table: Historical Operating Income, Net Income, Cash Flows, and Investment

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 705 | 1098 | 225 | -22.0% |

| 2024 | 904 | 1286 | 204 | -11.7% |

| 2023 | 1024 | 1278 | 291 | +342.5% |

| 2022 | 231 | 696 | 188 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, CFO, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 190 | 487 | 5.6 |

| 2024 | 196 | 868 | 7.2 |

| 2023 | 201 | 692 | 8.2 |

| 2022 | 201 | 126 | 1.9 |

Source: SEC companyfacts cache [F1].

Note: Operating Cash Flow prior to FY2025 not available in provided tags.

This table illustrates Zimmer Biomet’s growth surge through FY2023 followed by contraction linked closely with restructuring-related margin pressures in FY2025.

Outlook Analysis: Watchpoints Beyond Formal Forecasts

Looking ahead beyond present formal guidance durations, monitoring execution progress on Zimmer Biomet’s multi-year restructuring plan is crucial—especially since remaining pre-tax charges extend through the end of calendar year 2027 [N10][S1]. Timely realization of efficiency gains will influence margin trends thereafter.

Cybersecurity incident disclosures or shifts in risk environment bear watching given increasingly aggressive threat landscapes potentially impacting operational continuity or incurring remediation costs. Staying abreast of independent third-party assessment results reported periodically may signal adjustments in risk posture.

Regulatory developments affecting medical device approvals or import/export regulations represent an ongoing source of external uncertainty inherent to Zimmer Biomet’s business segments; any novel verdicts or policy changes at major jurisdictions could impact product launch timing or compliance expense structures [S19].

In sum, investors should track progress on structural cost containment alongside innovation pipeline momentum—two levers central to achieving sustainable growth post-restructuring phase.

This analysis is based on publicly available information as of February 20, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments