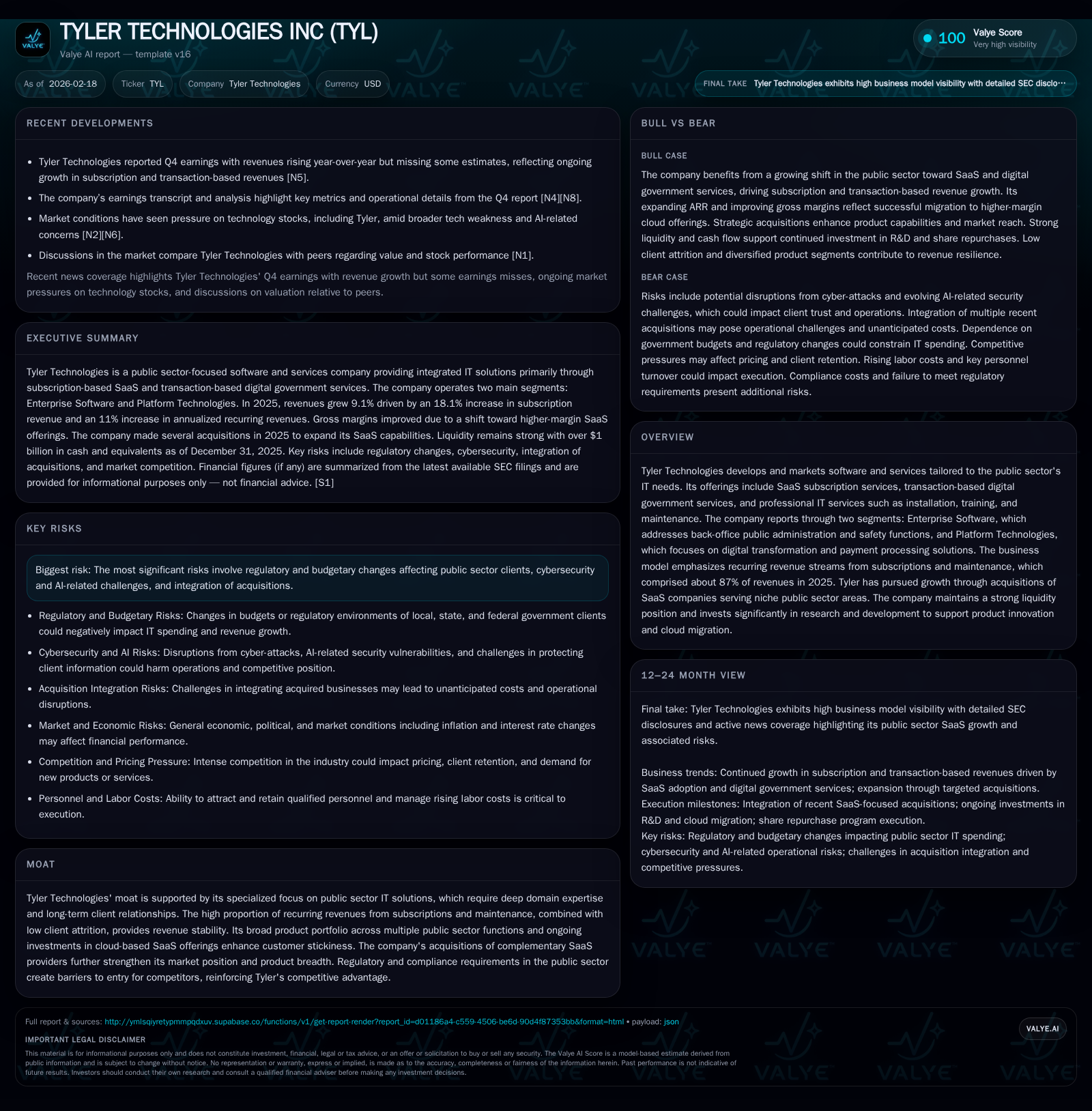

Tyler Technologies: Strengthening SaaS Leadership with Disciplined Capital Allocation

TYL’s pivot to SaaS subscription revenue and stable capital deployment underpin sustainable growth across its public sector IT solutions.

Tyler Technologies has demonstrated robust historical growth driven by an expanding SaaS revenue base and a strategic focus on recurring digital government service offerings. Enterprise Software leads revenue expansion while Platform Technologies navigates margin pressures from transactional business dynamics. The company’s disciplined capital allocation—marked by aggressive share repurchases and sustained R&D investments—supports innovation and shareholder returns. Moving forward, cloud migration, targeted acquisitions, and evolving public sector budgets are key catalysts, balanced against risks in AI regulation, cybersecurity, and post-acquisition integration.

Robust Historical Revenue and Profit Growth Backed by SaaS Transformation

Tyler Technologies (TYL) has delivered consistent top-line expansion over recent years, significantly fueled by its transformation toward subscription-based SaaS products tailored for the public sector's IT needs. For fiscal year 2025, TYL reported revenues of approximately $2.33 billion, reflecting a healthy 15.1% increase year-over-year [F1]. Concurrently, operating income grew nearly 20% to $357.7 million demonstrating operational leverage benefiting from a revenue mix shift favoring higher-margin SaaS offerings [F1][S4]. Net income followed suit with a 20% lift to $315.6 million.

This growth trajectory is underscored by gross margin expansion from 43.8% in 2024 to 46.5% in 2025 — a notable 270 basis point gain primarily attributable to increasing subscription revenues relative to declining traditional software license sales [S4]. Capital expenditure requirements declined by roughly 22% YoY to $16 million as cloud migration reduces on-premises infrastructure spend while reallocating resources to software development and R&D initiatives [F1][S4][S8]. Operating cash flow impressively scaled by about 4.6% reaching $653.5 million supporting substantial free cash flow generation exceeding $637 million after capex [F1][S16][S17].

The following table summarizes Tyler's annual financial performance over the prior four years:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 316 | 654 | 358 | 16 | +20.0% |

| 2024 | 263 | 625 | 300 | 21 | +58.5% |

| 2023 | 166 | 380 | 219 | 21 | +1.0% |

| 2022 | 164 | 381 | 214 | 23 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 175 | 638 | 8.5 |

| 2024 | 604 | 7.8 | |

| 2023 | 0 | 360 | 5.6 |

| 2022 | 0 | 359 | 6.3 |

Source: SEC companyfacts cache [F1].

Note: Some columns omitted due to limited data availability.

Segment Contributions: Enterprise Software vs Platform Technologies Performance

TYL reports results through two principal business segments that drive overall financial outcomes differently: Enterprise Software (ES) and Platform Technologies (PT). The ES segment focuses on mission-critical back-office public administration—including courts, public safety, education, and property functions—while PT provides transformative digital solutions such as payment processing platforms and workflow optimization tools [S7][S11].

In fiscal year 2025, Enterprise Software outperformed markedly benefiting from an ongoing SaaS subscription surge with revenues growing substantially (+27%) leading to a robust operating income improvement of about +21%, totaling roughly $661 million—a clear driver of corporate profitability gains [S19][S26]. Conversely, Platform Technologies experienced a slight contraction in operating income (-9%) influenced by contract-related loss reserves ($10.7 million), merchant fee inflation and headwinds within professional services revenues despite modest subscription revenue gains (~+5%) [S26].

This differential performance reflects inherent tradeoffs between segments: ES yields steady recurring subscription streams underpinned by multi-year contracts enhancing visibility and scalability; PT grapples more directly with volatile transaction volumes that fluctuate seasonally with digital government activities alongside pressure from rising merchant fees and contract disputes.

Growth Drivers Shift Toward SaaS and Digital Government Services

At the core of Tyler’s top-line acceleration lies its transition toward recurring revenue models rooted in SaaS subscriptions and digital transaction processing fees tied closely to government IT automation trends [N1][N2][S18]. By the end of calendar year 2025, recurring revenues—including subscriptions and maintenance—accounted for approximately 87% of total sales with annual recurring revenue (ARR) crossing the $2 billion threshold representing an increase of ~11% year-over-year [S18].

Growth also benefits from deliberate acquisitions such as EduLink (education compliance), CloudGavel (legal warrant management), Emergency Networking (emergency services), and MyGov (community development platforms)—each expanding Tyler’s footprint into specialized niche markets adjacent to core offerings while enriching the product portfolio and cross-selling opportunities [S19][N14]. These acquisitions uphold Tyler's focus on cloud-native SaaS capabilities aligned with public sector digital transformation imperatives.

Though Q4 results revealed pressure points including earnings misses reflecting margin compression largely due to increased R&D expenditures for cloud migration efforts and some contract disputes impacting transaction revenues ([N2]), management emphasizes innovation investments as critical for sustaining competitive differentiation amidst rapid technology adoption curves including AI enhancements embedded in platform upgrades [N1][N14].[S23]

Navigating Public Sector Budget and Regulatory Dynamics

Despite recurring revenue strength, Tyler remains exposed to fundamental risks tied to client budgetary constraints inherent within local/state/federal agencies where IT spending cycles are often subject to political influence and fiscal austerity measures [S1][S10]. Compliance mandates coupled with emerging cybersecurity threats amplify complexity necessitating rigorous controls over data protection given the sensitive nature of governmental information handled across its systems.

Additionally, evolving regulatory scrutiny around artificial intelligence represents both an opportunity and challenge for TYL as it integrates AI-driven product features while monitoring compliance landscapes that could delay go-to-market timelines or elevate development costs materially [S1][N7][N12]. The company acknowledges these headwinds openly within risk disclosures yet pursues an adaptive approach balancing innovation rigor with conservative compliance oversight.

Future Outlook: Cloud Migration, Acquisitions, and Innovation Pipeline

Looking ahead into early fiscal year 2026, Tyler solidified growth prospects via signing definitive agreements to acquire remaining interests in key targets paying approximately $212.5 million in cash expected closure early Q1 ’26—further consolidating its niche SaaS leadership position [S5][N14]. Capital expenditures are forecasted conservatively between $24–26 million annually focusing predominantly on infrastructure refreshes (~$10 million capitalized software development) supporting scalable cloud deployments rather than heavy hardware investments indicative of legacy models [S5].

The company continues robust R&D scaling with headcount expanding significantly (+57%) year-over-year dedicated principally to developing advanced next-generation SaaS functionalities including those leveraging AI capabilities within core products which enhance operational efficiency for clients while creating barriers for new entrants [S13][N1].[N14]

Market commentary from analysts like DA Davidson reiterates confidence in TYL’s execution capacity alongside cautious optimism surrounding cyclical budget pressures mitigated by multi-year contracts underpinning visibility on renewal rates and transaction volume trends [N14].

Capital Allocation Excellence: Share Buybacks, R&D Investment, and Debt Management

Tyler Technologies demonstrates exemplary capital allocation discipline balancing aggressive shareholder return strategies with sustained investments in innovation ecosystems requisite for maintaining leadership within highly specialized public sector markets.

In FY25 alone, share repurchases accounted for approximately $175 million supported by a refreshed Board authorization totaling $1 billion approved February ’26—of which about $885 million remains available as of mid-February indicating commitment to opportunistic buybacks amid market volatility [F1][S5]. The company finances repurchases principally via existing cash balances exceeding $1 billion supported by relatively modest outstanding debt of about $600 million which primarily comprises convertible senior notes due next year—underscoring conservative leverage posture enhancing financial flexibility going forward [F1][S6].

Simultaneously, research & development expenses rose sharply (+73%) reaching ~$205 million driven mostly by higher personnel costs including share-based compensation linked to expanded engineering teams focused on product enhancements fostering long-term competitive advantage through proprietary IP development [F1][S13].[N1]

Operating Metrics and Financial Health: Margins, ROE, and Cash Flow Analysis

Margin expansion remains central to TYL’s value creation story contrasted against sector peers where recurring revenue mix shifts usually dilute near-term profitability due to upfront acquisition costs or onboarding expenses. Gross margins improved materially from sub-44% levels toward nearly mid-46%, credited largely to SaaS subscription dominance offering incremental margin contributions via lower direct cost absorption compared with traditional license sales which continue their secular decline delivering less predictable revenue streams [F1][S25].[S4]

Return on equity approximates a solid ~8.5%, underscoring efficient equity utilization driven partly by buyback-induced equity base contraction coupled with net income advances supporting attractive profitability metrics for a technology provider focused uniquely on public sector administration IT automation platforms [F1].[N1]

Operating cash flow growth (+4.6%) signals underlying robustness amid ongoing investments validating business model scalability—with free cash flows comfortably north of $600 million affording ample reinvestment capacity alongside shareholder remuneration programs without undue financing stress or liquidity constraints as confirmed by current ratio near parity ~1.05x demonstrating balanced working capital management versus liabilities due short-term [F1][S16].[N14]

Risks from Cybersecurity, AI Adoption, and Acquisition Integration

While Tyler’s moat benefits from regulatory complexity barriers deterring new entrants combined with low attrition rates among public sector clients possessing mission-critical dependencies on customized software solutions maintained over long durations—the firm nonetheless confronts salient risks.

Cybersecurity forms one primary vulnerability vector given escalating cyber threats targeting government infrastructures requiring relentless investment in security protocols; any breaches could impose reputational damage translating into lost contracts or litigation exposures [S1][S10]. Simultaneously shifting AI regulatory frameworks designed to govern ethical usage may impact product launch schedules or inflate compliance cost structures imposing variability on expected return profiles particularly as AI modules become increasingly integral components embedded within TYL’s platform technologies portfolio.

Furthermore integration risks remain top-of-mind following several acquisitions completed recently; assimilating disparate company cultures or harmonizing overlapping technological stacks could disrupt operational momentum or elevate short-term expense levels counterbalancing organic SaaS growth contributions affecting consolidated margin trajectories if not managed prudently over ensuing quarters [N2][N14].[S10]

This analysis bases all referenced data strictly on publicly available SEC filings ([F1], ) and reputable market news sources ([N#]). Projections or expectations discussed herein do not constitute investment advice or recommendations but provide structured insights into Tyler Technologies' financial position and strategic outlook as of early calendar year 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments