Crisp Momentum’s Growth Held Back by Capital and Profitability Challenges in Nascent Microdrama Market

Early western microdrama platform with diversified monetization but limited capital and recurring losses constrain scale.

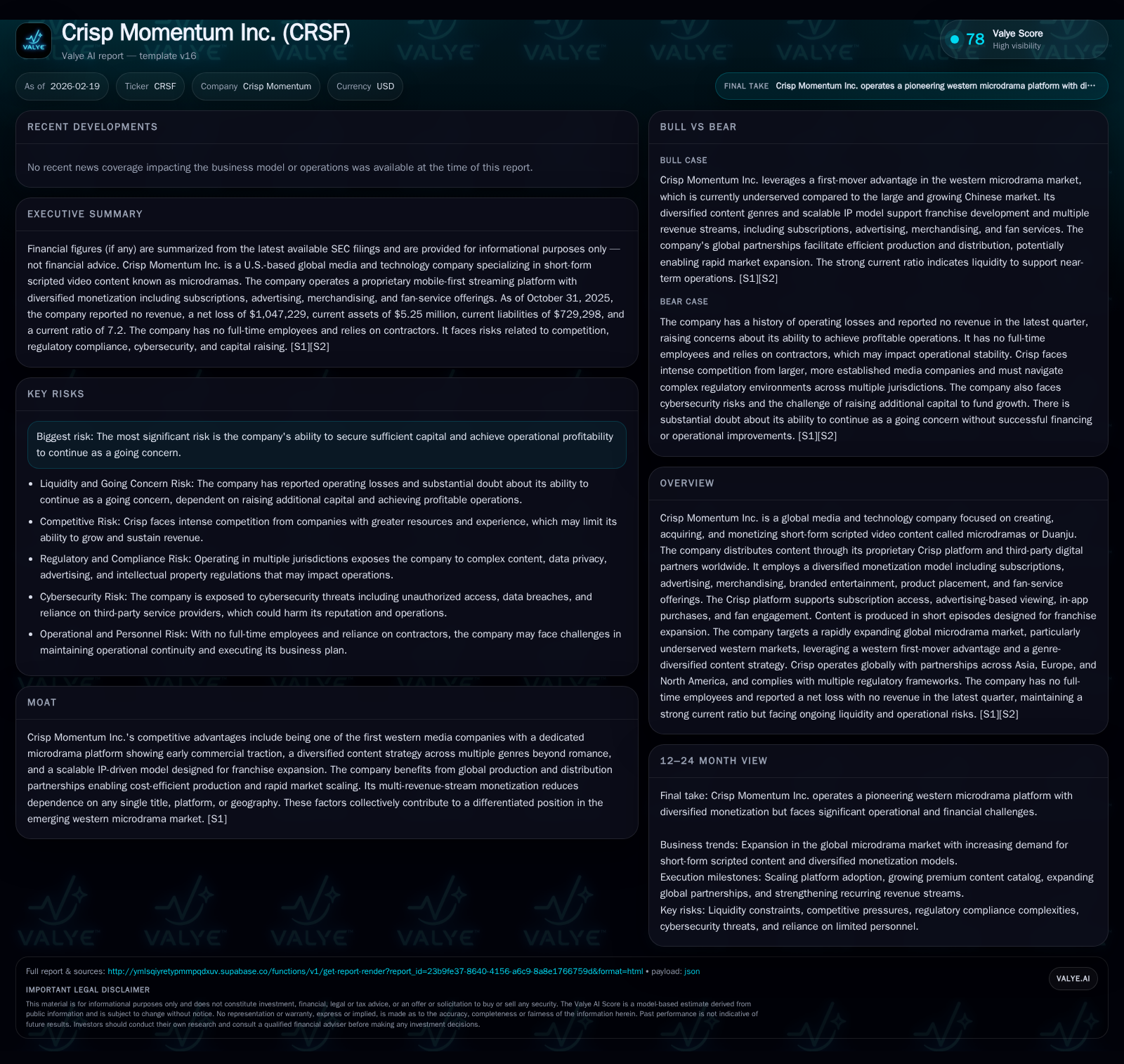

Crisp Momentum Inc. (CRSF) is pioneering the western market for short-form scripted video content known as microdramas, leveraging a proprietary streaming platform and multi-genre content strategy. Historically, the company has operated at escalating losses and negative operating cash flows, reflecting its early-stage status and heavy investments in content acquisition and platform expansion. Its growth prospects hinge on scaling user engagement, expanding proprietary content franchises, and broadening global partnerships. However, achieving profitability remains a critical hurdle alongside securing sufficient capital to sustain operations. Monitoring cash flow trends, capital raises, and user base metrics will be key to evaluating progress in this emerging entertainment segment.

Company Background and Business Model

Crisp Momentum Inc., trading under CRSF since its August 2025 rebranding post-acquisition transaction [S4][S13], has refocused its business model around an emerging entertainment format known as microdramas or "Duanju." These are ultra-short scripted video series typically consisting of 1-2 minute episodes released in multi-episode arcs optimized for mobile consumption.

The company's historical operations prior to the Pivot spanned industrial technology sectors before turning to blockchain-related businesses starting in 2021. The current core strategy began with acquiring Crisp Momentum Inc.'s assets in mid-2025 [S13]. Since then, Crisp has positioned itself as an early Western entrant in the rapidly expanding global microdrama market — a sector notably dominated by Chinese production hubs — with a goal to capture underserved Western audiences through a genre-diversified content library beyond traditional romance themes to include thriller, sci-fi, horror, comedy, animation, and documentary styles [S5][S6].

Platform and Monetization

Crisp operates its proprietary Crisp platform delivering mobile-first streaming of short-form scripted content worldwide. The platform supports multiple viewing modes — subscription access, advertising-supported free viewing, in-app purchases, as well as premium fan-service engagement such as collectibles or ancillary content sales [S5][S6].

Monetization is multifaceted:

- Subscriptions generate recurring revenue from paying users.

- Advertising revenue derives from ads integrated within free-to-view content tiers.

- Brand Integrations include product placement and sponsored storytelling elements.

- Merchandising offers physical collectibles related to popular series.

- Fan Services encompass premium interactions driving user engagement and incremental revenue.

This diversified model aims to de-risk revenue dependence by balancing direct consumer payments with advertiser and brand partnership income streams spanning multiple geographies [S5][S6].

Historical Financial Performance

Despite strategic positioning and emerging traction on the content front, Crisp Momentum's financial track record evidences sustained investment-phase losses alongside negative operating cash flows reflecting ongoing scale-up expenses for content production/acquisition and platform development.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -8 | -422410 | -8 | -939.0% |

| 2024 | -1 | -340769 | -1 | +89.5% |

| 2023 | -7 | -978976 | -3 | -190.4% |

| 2022 | -3 | -286527 | -2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 4071.6 |

| 2024 | 168.1 |

| 2023 | 7602.6 |

| 2022 | -44.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not reported due to early-stage operational profile without significant earned revenue [F1]. Capex is only reported for FY22 & FY21 at $9.5K each—minimal relative to operating expenses. Losses grew substantially in FY25 relative to prior years indicating accelerated investment or operating challenges.

Operating cash flows remain negative across all periods shown; however the FY25 decline is moderate compared with prior years suggesting possible stabilization attempts [F1]. Negative equity balance by FY25 points toward accumulated deficits exceeding shareholder capital.

Capital Structure and Liquidity

As of the latest filing dates:

- Cash & equivalents stood low at approximately $53K as per last publicly available point (FY21) but current assets versus current liabilities suggest strong near-term liquidity with a current ratio above 7x by late FY25 end [F1].

- The company completed significant equity transactions involving conversion of Series A Preferred Stock to common shares transitioning out preferred obligations by early 2025 [S14][S15].

- No dividends issued historically nor planned given reinvestment needs [S16].

- Absence of share buyback programs indicates capital conservation stance amid growth push [S14].

Funding remains a material risk factor given substantial historical losses and ongoing operational cash needs. The company acknowledges the risk of insufficient capital availability could necessitate business curtailment or restructuring efforts including asset sales or dilution through equity issuance [S8][S12].

Growth Prospects

Crisp aims to capitalize on several tailwinds:

- Significant growth forecast for the global microdrama market projected from $2B in 2024 to $10B by 2028 with Western markets notably underserved relative to Asia-centric incumbents [S6].

- Expansion opportunities via organic content development designed for franchise scalability enabling sequels/spin-offs/merchandising/licensing deals which can enhance lifetime value of intellectual property [S5][S6].

- Leveraging multi-region partnerships spanning Asia-Europe-North America facilitates cost-efficient production scaling and diversified distribution channels including third-party OTT providers alongside its own platform [S5][S6][S9].

- Diverse genre portfolio provides differentiation supporting broader audience reach than competitors focused narrowly on romance genres [S5].

However growth potential is tempered by several challenges:

- The nascent nature of the Western microdrama market creates uncertainties around user adoption rates and willingness to pay leading to difficulty forecasting revenues reliably [S1][S18].

- Dependence on continuous content pipeline renewal means failure to match fast evolving viewer tastes could reduce engagement jeopardizing monetization efficacy [S1][S25].

- Reliance on third-party digital distribution partners introduces risk exposure that could impact reach or effective monetization if agreements change unfavorably or platforms alter policies unexpectedly [S1][S25].

- Competitive pressure from larger global streaming platforms that have entrenched user bases may limit swift market penetration or impose higher marketing costs for customer acquisition [S27].

Returns and Capital Allocation Considerations

The company has no history of generating positive returns or free cash flow thus far; ROE calculations based on recent net loss over negative book equity yield skewed high negative values signaling deep ongoing deficit absorption rather than returns generation [F1]. Capital expenditures remain minimal suggesting no large infrastructure investments but rather focus on content licensing/acquisition which appears expensed as operating costs.

Management explicitly signals intention to retain earnings (once positive) for reinvestment into business growth rather than pay dividends or repurchase shares near-term [S16]. This aligns with standard media tech startup economics where scale attainment precedes profitability.

Risks Summary

Key perils include:

- Ability to raise additional funding timely on acceptable terms crucial for sustaining operations and executing growth plans amidst ongoing losses [S1][S8][S12].

- Protecting intellectual property against infringement claims essential due to reliance on proprietary IP franchises linked directly with monetization potential [S22].

- Attracting/retaining specialized management talent pivotal given nascent industry knowledge requirements and competitive labor markets for tech/media professionals without employment agreements currently limiting retention guarantees [S27].

- Navigating rapid shifts in user preferences demands agile content innovation capabilities coupled with robust data analytics infrastructure; failure here can quickly erode competitive position [S25].

- Exposure to regulatory complexity across multiple international jurisdictions covering online video licensing rules, age rating controls, data privacy laws including GDPR compliance adds compliance cost layers and operational risk factors that must be managed vigilantly [S10][S17].

What To Watch Next (Analysis)

Absent explicit guidance from management on near-term financial milestones due to early phase operations [N#], stakeholders should monitor:

- Quarterly updates on user base growth metrics — active users by geography and payment tier conversions.

- Progression of proprietary content catalogue expansions including new IP launches or franchising deals.

- Improvement trends in operating loss narrowing or positive EBITDA inflection points.

- Liquidity events such as equity raises or strategic partnerships unlocking funding.

- Updates on product development roadmap demonstrating enhancements in recommendation algorithms underpinning user engagement.

Conclusion

Crisp Momentum represents an ambitious attempt at leading Western expansion into a high-growth segment traditionally dominated by Asian incumbents. Its multi-modal revenue approach combined with IP-centric franchise strategies positions it uniquely yet also exposes it to substantial operational execution risks inherent in any early-stage media technology venture.

Success will depend heavily on securing stable funding sources while proving scalable user engagement amidst shifting consumer preferences. Meaningful commercial traction beyond initial adoption remains a prerequisite before margin expansion becomes realistic.

Disclaimer: This analysis is based exclusively on public filings including SEC reports ([F1],[S#]) through February 2026; it does not constitute investment advice but aims solely to provide grounded insights into the company's financial condition and industry positioning.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments