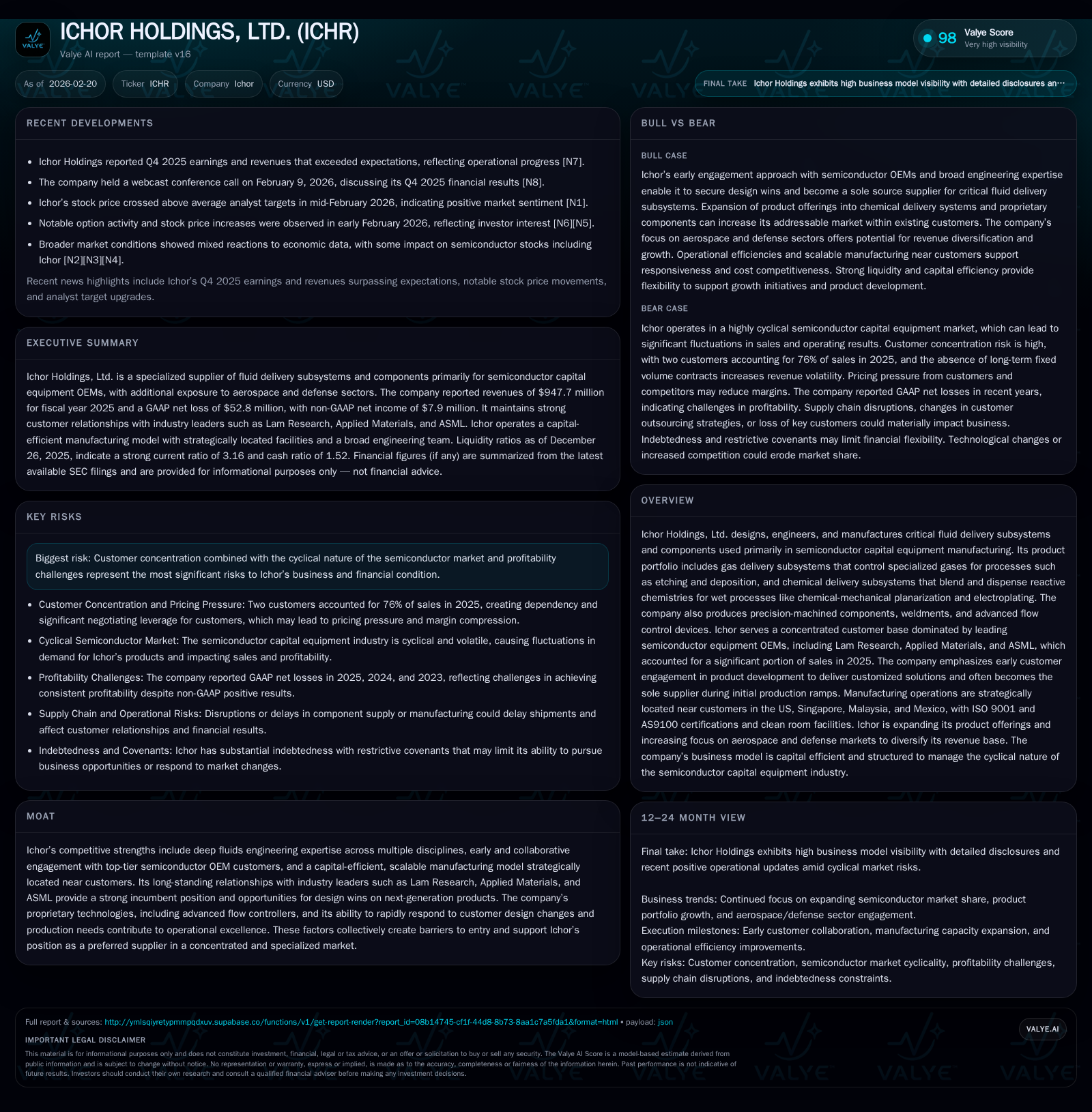

Ichor Holdings’ Profitability Pressures Amid Strong Semiconductor OEM Reliance

Market concentration and operational costs challenge Ichor’s drive to convert revenue growth into sustained profits.

Ichor Holdings, Ltd. designs and manufactures critical fluid delivery subsystems for semiconductor capital equipment OEMs, with a customer base heavily weighted toward industry giants such as Lam Research and Applied Materials. Despite steady revenue growth from approximately $811 million in 2023 to nearly $948 million in 2025, the company has reported consecutive net losses over the past three years, widening in 2025 due to elevated operating expenses and restructuring charges. Its capital-efficient manufacturing footprint near customer sites underpins operational agility, but dependency on a narrow customer set and cyclicality of semiconductor investment remain key constraints. Ichor aims to expand within existing customers by leveraging its engineering expertise and early design involvement but must contend with intense pricing pressure and the need for continued R&D investment, especially as AI integration gains relevance in semiconductor processing tools.

Company Profile and Market Position

Ichor Holdings, Ltd. specializes in designing and manufacturing critical fluid delivery subsystems essential for semiconductor manufacturing equipment. Its product portfolio includes gas delivery systems that precisely regulate specialized gases used in etching and deposition processes, chemical delivery systems managing reactive liquids for cleaning or electroplating, and precision-machined components including weldments with advanced joining technologies [S1][S21]. These offerings support complex production steps where fluid delivery precision directly impacts semiconductor yields.

The company’s customer base is highly concentrated among leading semiconductor OEMs—particularly Lam Research, Applied Materials, and ASML—which together represented over 76% of sales in 2025 [S4][S26]. While this concentration reinforces close collaborative relationships facilitating early-stage engineering engagements and service flexibility, it also exposes Ichor to cyclicality inherent in semiconductor capital expenditure patterns.

Historical Growth and Financial Performance

Although detailed revenue figures are not available via XBRL tags, narrative disclosures indicate revenue grew from approximately $811 million in 2023 to nearly $948 million by the end of 2025 [S21]. This growth reflects incremental design wins at existing customers alongside expanded content per tool.

Profitability metrics reveal significant challenges. Operating income deteriorated sharply from -$10.9 million in FY23 to -$7.6 million in FY24 then plunging further to -$39.3 million in FY25 [F1]. Net income losses deepened from -$43.0 million (FY23) to -$20.8 million (FY24) before expanding substantially to -$52.8 million (FY25) [F1]. This trend highlights cost pressures stemming from supply chain inflation, intensified pricing competition, restructuring charges during 2025, and possibly increased R&D investments.

Operating cash flow remained positive though compressed: from $57.6 million in FY23 down to $29.9 million in FY25 [F1]. Capital expenditures rose markedly from $15.5 million (FY23) to $36.2 million (FY25), consistent with investments in capacity expansion or technology upgrades [F1]. The resulting free cash flow was negative about $6.3 million in FY25.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -53 | 30 | -39 | 36 | -153.5% |

| 2024 | -21 | 28 | -8 | 18 | +51.6% |

| 2023 | -43 | 58 | -11 | 15 | -159.0% |

| 2022 | 73 | 31 | 86 | 29 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -6 | -8.0 |

| 2024 | 10 | -3.0 |

| 2023 | 42 | -7.6 |

| 2022 | 2 | 12.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not available from provided XBRL tags; dividends paid data is not available.

Business Model and Operations

Ichor operates a capital-efficient manufacturing model with facilities strategically located near major customers' production sites across the U.S., Singapore, Malaysia, and Mexico [S7][S15]. This proximity enables rapid responsiveness during new product introductions or configuration changes—a key competitive advantage.

The company maintains ISO 9001 certification across manufacturing sites plus AS9100 certification relevant for aerospace products [S7]. Cleanroom environments meeting Class 100/10,000 standards at key locations ensure contamination control crucial for gas and chemical delivery systems.

Early engagement at the design phase fosters strong customer relationships; account managers collaborate closely within customer design vaults ensuring alignment with evolving technical requirements [S16]. This approach often secures sole-source supplier status while shortening lead times—sometimes as fast as 20–30 days for certain gas delivery systems.

Industry Dynamics and Competitive Environment

The semiconductor capital equipment market is highly concentrated: five OEMs generate over 70% of wafer fabrication equipment revenues [S4]. Within fluid delivery subsystems, Ichor competes against firms like Ultra Clean Technology alongside fragmented suppliers targeting weldments or precision machining niches [S17]. Furthermore, OEMs themselves pose latent competitive threats should they choose to insource subsystem production.

Pricing pressure is significant due to buyer leverage; major customers routinely negotiate price reductions or impose elevated liability risks through indemnification clauses [S19]. New products typically carry lower margins initially until scale economies materialize.

Emerging industry demands include AI/ML integration enabling real-time process optimization through enhanced flow control analytics [S13]. Incorporating software intelligence heightens product complexity; failure to keep pace risks loss of market share or pricing power.

Growth Outlook and Strategic Priorities

Per filings and recent earnings commentary [N1][N2], Ichor plans organic growth by:

- Expanding share within existing semiconductor customers by broadening product scope beyond core fluid delivery systems into proprietary chemical modules and precision components [S18].

- Leveraging early collaborative development cycles to secure sole-source positions on next-generation tools involving EUV lithography requiring ultra-clean gas control.

- Growing addressable markets outside semiconductors—particularly aerospace & defense machining segments currently composing less than 10% of sales but offering margin expansion potential [S4][S18].

- Continuing investments aimed at manufacturing efficiency improvements balancing lean operations with capacity additions aligned with customer demand.

Growth constraints include vulnerability to semiconductor capex volatility exacerbated by lack of minimum volume contracts creating order timing unpredictability [S25][S27]. Supply chain uncertainties may further compress margins despite negotiation efforts.

Potential intellectual property litigation risk remains notable given patent overlaps common among component suppliers; Ichor holds over 100 granted patents but relies largely on trade secrets for competitive protection [S9][S17].

Returns Profile and Capital Allocation

Ichor's approximate return on equity was negative about -8% for FY25 based on net loss relative to shareholder equity near $664 million year-end [F1]. Operating losses underline profitability challenges despite robust revenue trends.

Operating cash flows remain positive but diminished compared to prior years indicating effective working capital management yet highlighting reinvestment demands exceeding operating surplus after capex spending.

Data on dividends paid or share repurchases post-2019 is not available from provided tags; historical buybacks appear limited and outdated [F1]. The company carries approximately $125 million term loan debt subject to restrictive covenants that could constrain discretionary capital returns [S6][S8].

Risks Summary

Key risks identified include:

- High customer concentration exposing revenue volatility if key OEMs reduce outsourcing or insource production.

- Cyclical downturns inherent in semiconductor markets affecting capital expenditures impacting demand for subsystems [S24][S27].

- Pricing pressures driven by powerful buyers risking margin erosion.

- Operational complexity including supply chain disruption risks heightened by geopolitical instability or material scarcity.

- Intellectual property litigation exposure potentially imposing legal costs or sales interruptions.

- Need for ongoing investment into AI-enabled technologies critical for maintaining competitive edge.

- Compliance burdens related to environmental regulations, export controls, data privacy laws adding cost layers [S20][S23].

- Indebtedness level limiting financial flexibility under restrictive covenants raising refinancing risks if performance deteriorates further [S24].

What To Watch Going Forward (Analysis)

Investors should monitor:

- Semiconductor capex trends among top global OEMs signaling demand vitality.

- Progression of AI integration within fluid control offerings including partnerships or technology breakthroughs enhancing subsystem intelligence.

- Customer diversification efforts particularly aerospace & defense vertical penetration where scale is nascent but margins may improve.

- Margins trajectory post-restructuring initiatives assessing operational leverage paired with pricing power dynamics.

- Free cash flow conversion trends indicating sustainable self-financing capacity supporting long-term innovation without excessive external funding reliance.

- Supply chain health impacting lead times or cost inflation threatening gross margin stability.

- Regulatory developments around ESG disclosures influencing market access or brand reputation within tight supplier qualification windows practiced by major OEMs.

Conclusion

Ichor Holdings operates at a critical juncture where fluid delivery precision materially influences semiconductor device yields amid escalating process complexities driven by EUV lithography advances. Its entrenched relationships with leading OEMs combined with engineering acumen support medium-term revenue growth opportunities. However, persistent losses evidenced by wide operating deficits highlight structural profitability challenges amidst intense pricing competition coupled with cyclical semiconductor capex swings. The company’s scalable yet geographically distributed manufacturing footprint offers operational flexibility though reliance on a small customer cluster remains the largest concentration risk threatening revenue visibility absent broader diversification or AI-enabled technology differentiation gains embedded within next-generation fluids management solutions.

This analysis is based solely on publicly disclosed financial data and regulatory filings up to early 2026 without providing any investment recommendation or market advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments