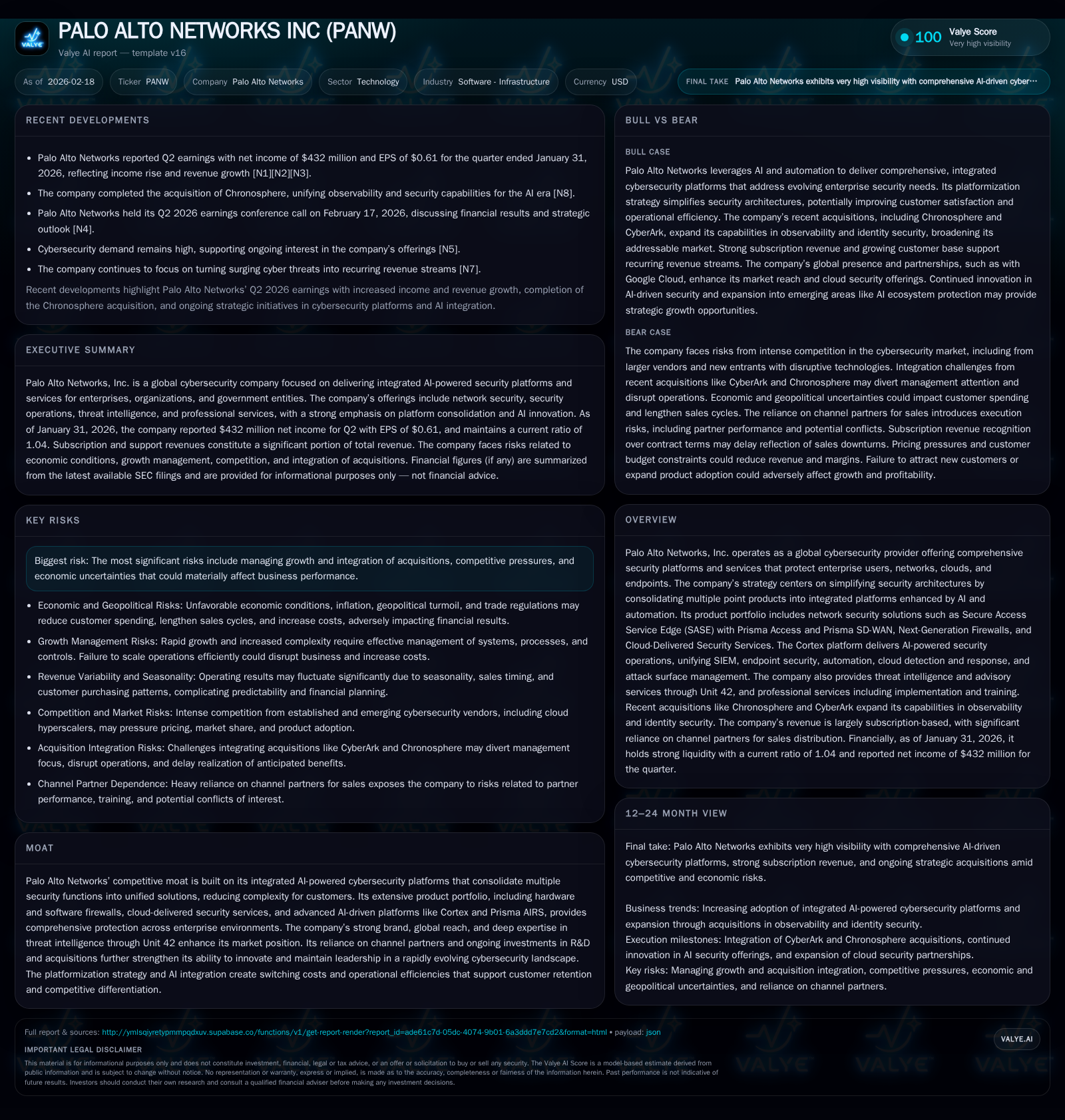

Palo Alto Networks Balances AI-Driven Platform Expansion Against Integration and Competition Risks

The cybersecurity leader pursues growth through AI-platform innovation and acquisitions, while managing operational scaling and intense market rivalry.

Palo Alto Networks (PANW) has built strong momentum over recent years by expanding its integrated cybersecurity platforms centered on AI and automation. The company’s historical growth, reflected in a nearly 30% revenue increase in FY2025, has been driven by consolidation of product offerings into unified solutions like Cortex and Prisma, along with strategic acquisitions including recent additions such as Chronosphere and CyberArk. The firm faces a complex tradeoff between accelerating innovation and managing integration risks amid intensifying competition from diversified tech giants and specialized niche players. While operating profitability and cash flow remained robust in FY2025, volatility in net income and pressures on pricing highlight ongoing execution challenges. Moving forward, Palo Alto’s prospects hinge on its ability to sustain platform coherence, harness AI effectively, navigate economic uncertainties, and realize acquisition synergies.

Historical Growth and Financial Performance

Palo Alto Networks has demonstrated impressive expansion over the last several fiscal years culminating in significant scale gains by FY2025. Revenue grew from approximately $0.93 billion in FY2015 to $11.4 billion by FY2025, capturing a compound annual growth rate (CAGR) of roughly 10% over the decade with an acceleration in more recent years. Year-over-year revenue jumped 29% between FY2024 ($8.8B) and FY2025 ($11.4B) reflecting broad-based strength across its integrated cybersecurity platforms leveraging AI and cloud delivery.[F1]

Operating income surged 81.7% YoY to $1.24 billion in FY2025 from $684 million in FY2024, indicating effective operating leverage despite continued investment into R&D and global sales expansion.[F1] However, net income declined sharply by 56% YoY to $1.13 billion primarily due to acquisition-related expenses including integration costs tied to the CyberArk transaction along with upfront investments for Chronosphere.[F1] This suggests near-term margin pressures amid aggressive inorganic growth efforts.

Cash generation remains robust: operating cash flow increased 14% YoY to approximately $3.72 billion for FY2025 while capital expenditures remain modest relative to cash flows (latest quarterly capex at ~$37 million). This yields estimated free cash flow of about $3.68 billion supporting financial flexibility for further investments or acquisitions.[F1]

Return on equity is estimated at approximately 14.5% for FY2025 based on net income relative to shareholder equity—indicative of solid capital efficiency within the technology infrastructure sector.[F1]

No dividends have been paid historically according to available data; share repurchases tapered off completely in FY2025 following moderate buyback activity of $567 million in FY2024 and prior years.[F1]

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 1.1 | 3.7 | 1243 | -56.0% |

| 2024 | 2.6 | 3.3 | 684 | +486.2% |

| 2023 | 0.4 | 2.8 | 387 | +264.7% |

| 2022 | -0.3 | 2.0 | -189 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 14.5 |

| 2024 | 567 | 49.9 |

| 2023 | 273 | 25.1 |

| 2022 | 892 | -127.1 |

Source: SEC companyfacts cache [F1].

Note: Dividends are not available from provided tags; buybacks ceased in latest fiscal year.

Product Portfolio and Platform Strategy

Palo Alto’s growth is anchored by a platformization strategy integrating disparate security functions under AI-powered unified frameworks.[S4] Core pillars include:

- Network Security: Zero Trust architecture supported by Secure Access Service Edge (SASE) via Prisma Access combined with Prisma SD-WAN securing remote workforce and branch offices.

- Next-Generation Firewalls (NGFWs): Hardware NGFWs protect on-premises data centers; software NGFWs secure cloud networks.

- Cloud-Delivered Security Services (CDSS): Advanced threat prevention including malware detection (WildFire®), intrusion prevention, URL filtering, DNS security, IoT/OT monitoring.

- Prisma AIRS: A comprehensive AI security platform protecting customers’ entire AI ecosystem through model scanning to runtime defenses.[N1][S4]

- Strata Cloud Manager: Centralized network security management with embedded AI assistance enabling proactive vulnerability identification.

- Cortex Platform: AI-powered security operations consolidating SIEM, endpoint detection & response (EDR), SOAR automation, attack surface management.

This integrated approach reduces complexity for customers by eliminating multiple vendors, driving cost efficiencies and renewal stickiness.[S14]

Recent Acquisitions Supporting Expansion

In January 2026 Palo Alto completed the Chronosphere acquisition unifying observability data with security contexts—a strategic move addressing hybrid cloud complexity enhancing Cortex capabilities.[N1]

The pending CyberArk acquisition will add identity security solutions specializing in privileged access management—broadening Palo Alto’s addressable market beyond network security.[S25]

These acquisitions illustrate a dual strategy expanding horizontally across cybersecurity categories while deepening capabilities into emerging areas like AI ecosystem defense.[N12][N2]

Industry Context: Competition & Differentiation Challenges

The cybersecurity market is intensely competitive:[S9][S12][S13] Large tech incumbents such as Microsoft, Cisco, Alphabet embed security into broader platforms often offering bundled lower-cost solutions.

Specialized pure-play vendors like Check Point, Fortinet, CrowdStrike focus on niche or vertical segments with rapid innovation cycles.

Startups target emerging threats while cloud hyperscalers invest heavily embedding native multi-cloud security posing challenges to standalone vendors.[N2][S11]

Palo Alto leverages scale through tightly integrated AI-driven platforms combining network firewall hardware/software with cloud services plus endpoint protections supported by threat intelligence from Unit42 consulting services—creating switching costs but requiring flawless integration across product lines.[S20][S22]

Operational Execution & Risk Factors

Rapid headcount growth (+6% over six months reaching ~17,000 employees) imposes pressure on management systems necessitating improvements in IT infrastructure and internal controls or risking operational disruptions.[S27]

Supply chain risks persist due to reliance on international hardware component sourcing; shortages or regulatory changes could delay shipments causing lost sales.[S18]

Legal/regulatory risks are elevated given evolving cybersecurity standards plus emerging legislation governing AI embedded in products imposing compliance costs and liability exposure if data misuse or algorithmic bias occurs.[S7][S8]

Economic uncertainty affects corporate IT spending potentially causing seasonal revenue fluctuations since subscription revenues are recognized ratably over contract terms lagging immediate sales results.[S7]

Security incidents affecting Palo Alto’s own network could damage brand trust critical for customer relationships.[S10]

Forward-Looking Considerations & Milestones to Watch

Key milestones include:

- Successful integration of CyberArk impacting margins and positioning within identity/security convergence.

- Adoption of new AI-specific platforms like Prisma AIRS reassuring customers against emerging generative/ML threats.

- Uptake of Prisma Access Browser extending Zero Trust directly onto endpoints amid hybrid work trends.

- Renewal rates on multi-year subscriptions as indicators of recurring revenue health.

- Competitive pricing pressures from hyperscalers bundling alternatives possibly compressing margins.

- Advances in Cortex XSIAM automation reducing operational overhead enhancing platform stickiness.

These factors will test Palo Alto’s capacity to balance rapid innovation with disciplined execution amid complex integration challenges.

Returns & Capital Allocation Analysis

Based on latest fiscal data:[F1] approximate return on equity is about 14.5%, consistent with technology infrastructure benchmarks though reflecting partial dilution impacts from recent acquisitions.

Free cash flow approximates $3.68 billion derived from operating cash flows less modest capex enabling reinvestment without external financing dependency.[F1]

Stock repurchases halted post-FY2024 with zero buybacks reported for FY2025; dividends have not been declared historically indicating prioritization of growth reinvestment over shareholder returns.[F1]

Conclusion

Palo Alto Networks stands at an inflection point leveraging its reputation as an AI-integrated unified cybersecurity platform provider while scaling acquisitions such as Chronosphere and CyberArk that extend functionality amid heightened competition. Historical double-digit revenue growth coupled with strong operating leverage underscores operational strength.

However, short-term net income volatility linked to acquisition costs alongside complex integration demands require disciplined execution as product complexity grows amid volatile macroeconomic conditions.

The company’s future success depends on effective platform consolidation including expanded identity offerings, sustained innovation around critical themes like generative AI protection, resilient supply chain management for hardware consistency, and adept navigation of evolving regulatory landscapes shaping global cybersecurity norms.

This analysis is based solely on publicly available information as of February 18, 2026 including SEC filings [F1][S#] and news releases [N#], without any investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments