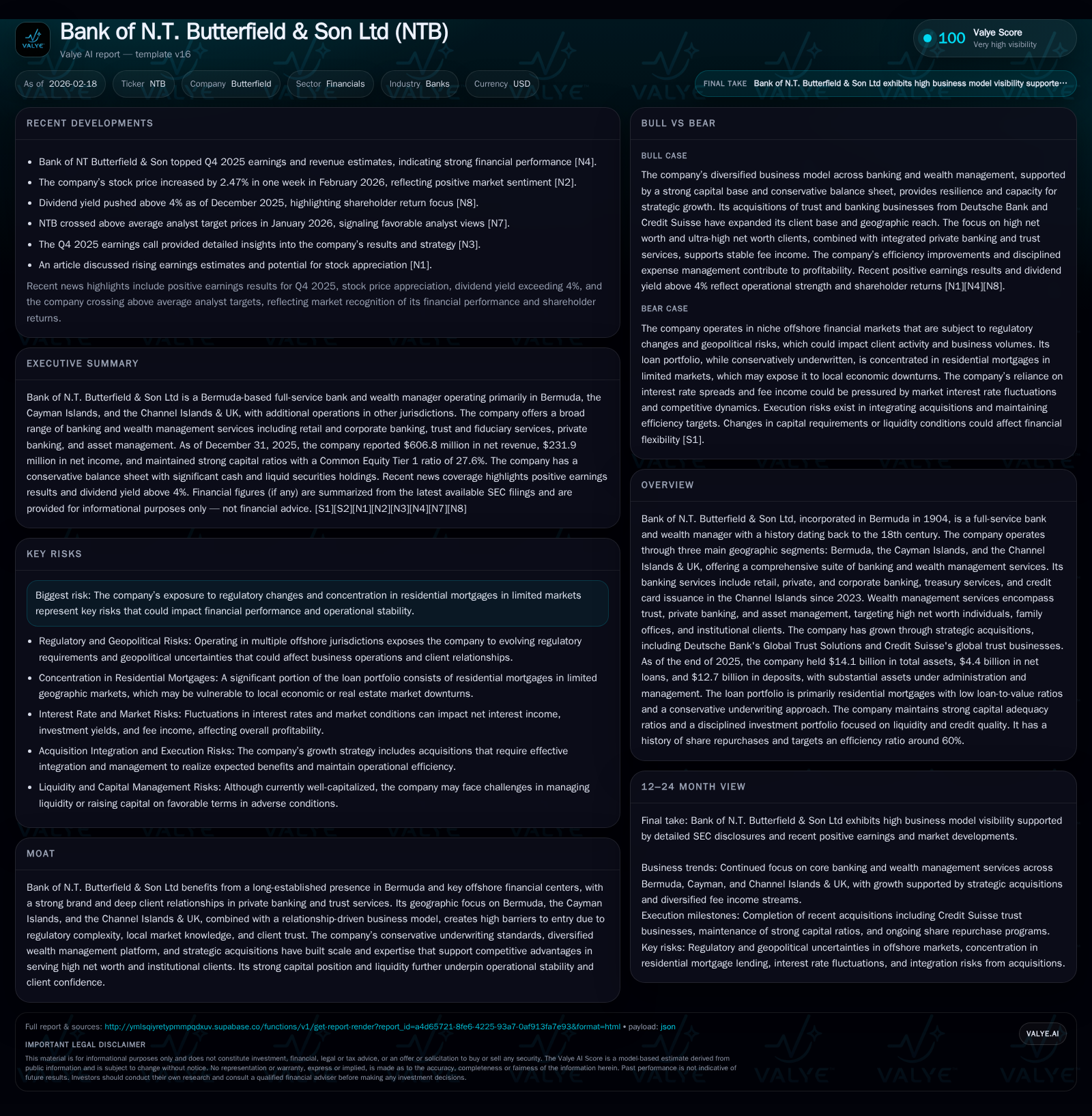

How Bank of N.T. Butterfield & Son Ltd Leverages Geography and Acquisitions for Wealth Management Scale

Bank of N.T. Butterfield & Son Ltd expands its wealth management footprint in key offshore markets through targeted acquisitions and geographic specialization.

Bank of N.T. Butterfield & Son Ltd has demonstrated consistent earnings growth supported by strategic acquisitions across Bermuda, the Cayman Islands, and the Channel Islands & UK. The company’s long-standing regional presence and relationship-focused approach underpin a wealth management platform that benefits from high barriers to entry. Strong capital ratios and disciplined underwriting support operational resilience amid evolving regulatory requirements. Looking forward, continued M&A activity, digital banking enhancements, and a measured capital allocation strategy are critical to sustaining growth in its niche private banking and trust services.

Historic Financial Performance and Profitability Drivers Through 2025

Bank of N.T. Butterfield & Son Ltd posted steady growth over the past four fiscal years leading to calendar year 2025. Total revenues increased to approximately $607 million in 2025, marking a +4.6% year-over-year improvement from $580 million in 2024 and reversing prior flat revenue trends from 2023 to 2024 [F1]. Net income rose more sharply by +7.2% reaching $232 million in 2025, up from $216 million in the prior year [F1]. This net income growth outpaced revenue gains due to effective cost control measures alongside favorable mix shifts.

The bank's return on equity (ROE) remains robust at about 20.3%, based on trailing net income against equity of $1.14 billion as of FY2025 end, underscoring sustained profitability [F1]. Operational cash flow also rose modestly by +5.3% to $280 million in 2025, highlighting healthy cash generation capability despite relatively modest capital expenditure levels stable around $19 million annually (capex data limited for recent years) [F1].

A key driver is the rising fee income ratio which climbed above 40%, signaling the increasing weight of stable, recurring fee-based revenues largely sourced from wealth management including trust administration and asset management services [S1]. This diversification away from purely interest income stabilizes earnings volatility typically associated with loan portfolios.

Meanwhile, credit performance indicators reflect prudent underwriting standards with non-performing loans improving to lower levels and minimal net charge-offs recorded in recent years [S1, S8]. The residential mortgage portfolio dominates lending exposure (~70%), benefiting from low loan-to-value metrics (nearly 79% below 70% LTV) within small offshore markets exhibiting structural barriers to entry.

Historical Financial Summary

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 607 | 232 | 280 | +4.6% | +7.2% |

| 2024 | 580 | 216 | 265 | +0.2% | -4.1% |

| 2023 | 579 | 225 | 300 | +5.3% | +5.4% |

| 2022 | 549 | 214 | 219 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 78 | 147 | 20.3 |

| 2024 | 80 | 155 | 21.2 |

| 2023 | 86 | 89 | 22.5 |

| 2022 | 87 | 4 | 24.7 |

Source: SEC companyfacts cache [F1].

Acquisition-Fueled Expansion in Core Offshore Markets

Butterfield’s strategic growth leverages its deep expertise in private banking and trust services across Bermuda, Cayman Islands, Channel Islands, and UK corridors through targeted acquisitions enhancing scale and market share.

Notable acquisitions include Deutsche Bank’s Global Trust Solutions (GTS) acquired in early 2018 which added approximately 1,000 trust structures servicing some 900 private clients across Guernsey, Switzerland, Cayman Islands, and Singapore — a move that bolstered service capabilities on trust administration platforms and expanded assets under administration significantly [S5, S16]. Another pivotal transaction was the purchase of Deutsche Bank’s banking and custody operations in Cayman and Channel Islands completed by mid-2019.

The acquisition of ABN AMRO Channel Islands business in mid-2019 further widened investor offerings encompassing banking, investment management, custody products for trusts and funds operating within Jersey and Guernsey jurisdictions. The December 2023 completion of Credit Suisse global trust businesses acquisition across Singapore, Guernsey, and the Bahamas adds another layer to Butterfield’s international footprint with premium client segments.

These transactions contribute not only new accounts but operational synergies through scalable relationship-driven client retention strategies common in offshore wealth circles where service continuity is paramount.

Navigating Regulatory Demands and Capital Adequacy

Operating within multiple complex offshore regulatory regimes mandates rigorous capital management frameworks compliant with evolving Basel III/IV standards as enforced by local regulators including Bermuda Monetary Authority (BMA). Butterfield is classified as a domestic systemically important bank (D-SIB), incurring an additional CET1 capital surcharge of approximately 3%, reflecting systemic economic roles including deposit-taking relevance.

As of December 31, 2025 reporting, the bank holds a formidable Common Equity Tier 1 (CET1) ratio of 27.6%, substantially above minimum regulatory thresholds inclusive of capital conservation buffers awaiting full Basel IV output floor implementation through January 2028 [S1,S21]. The Tier 1 capital ratio matches CET1 at the same level while total capital ratio stands slightly higher at around 27.8%, signaling ample loss-absorbing capacity.

Leverage ratio approximates a strong cushion at about 7.6% versus required minimums near 5%, demonstrating conservative balance sheet structuring relative to risk-weighted assets (RWA). Liquid asset holdings remain significant including nearly $1.7 billion cash equivalents ensuring liquidity buffers amid cyclical pressures [S4,S7].

This robust capital positioning allows flexibility for organic growth initiatives or potential bolt-on acquisitions without compromising regulatory compliance or credit ratings.

Operating Efficiency and Margin Trends: Assessing Underlying Business Resilience

Efficiency improvements reflect successful streamlining following post-crisis restructuring efforts specific to this offshore banking niche characterized by smaller scale relative to global universal banks but enhanced customer intimacy.

The core efficiency ratio improved steadily to about 58.5% in FY2025 down from near 60% earlier years indicating better cost control relative to revenue generation on core operations excluding non-recurring items [S1]. Concurrently, net interest margin (NIM) held reasonably steady at approximately 2.69%, reflecting mix effects where higher yielding investments partially offset compressed loan yields triggered by rate cuts during the year [S1,F1].

Fee income growth offsets some margin pressures derived from decreasing loan volumes tied primarily to residential mortgage maturities exceeding originations amid limited addressable market expansion opportunities [S10,S11]. The blended banking plus wealth services model provides margin stability uncommon among regional banks heavily reliant on traditional spread-based lending.

Capital Allocation Focus: Dividends, Share Repurchases, and Balance Sheet Strength

Butterfield maintains a disciplined capital return policy aligned with earnings performance and excess capital generation capacity leveraging its robust balance sheet.

In FY2025 it paid out stable dividends totaling approximately $77.7 million while deploying close to $146.7 million towards common share repurchases — a program actively renewed through late December authorization indicating board confidence in sustainable cash flows [F1,S9,S3]. This buyback scale notably exceeds prior years demonstrating heightened emphasis on shareholder returns alongside organic business investments.

Equity increased meaningfully year-over-year reaching $1.14 billion by end-2025 reinforcing internal capitalization strength supporting leverage constraints balancing acquisition funding needs versus organic growth [F1,S4]. Cash balances remained substantial above $1.7 billion providing liquidity cushions.

This measured allocation prudently balances growth reinvestment with shareholder value creation reflective of private banking industry norms favoring stable returns coupled with capital base longevity.

Growth Catalysts and Near-Term Milestones

Looking ahead, Butterfield aims to sustain its expansion trajectory driven chiefly through:

- Continued M&A activity focused on complementary private trust business lines enhancing AUA performed within core geography or adjacent offshore hubs,

- Product innovation evidenced by introducing credit card offerings since establishing Channel Islands footprint in 2023 helping diversify deposit mix,

- Digital banking upgrades targeting enhanced customer experience amidst competitive pressures for tech-enabled wealth solutions [N2],

- Sustained strong asset inflows reflecting high net worth client loyalty fostered through relationship-driven servicing models.

Constraints persist primarily around concentrated residential mortgage exposure within few small jurisdictions prone to regulatory changes or housing market volatility limiting aggressive loan book growth [S8]. Regulatory tightening phases like Basel IV implementation continue mandating elevated capital thresholds potentially constraining leverage-based expansion absent proportional equity injections.

Additionally, competitive dynamics in global offshore finance necessitate ongoing investment in compliance capabilities especially amid worldwide anti-money laundering scrutiny intensifying operational costs.

Recent market commentary highlights optimism as NTB stock has risen alongside upward analyst earnings estimate revisions corroborated by successive quarterly beats reported early February 2026 Q4 call notes [N3,N6,N7]. Key milestones going forward include:

- Monitoring quarterly revenue composition shifts between lending net interest margins versus wealth service fees,

- Observing successful integration progress on recent acquisitions particularly Credit Suisse global trusts overlay,

- Tracking deposit base behavior amid potential rate volatility impacting funding costs,

- Regulatory developments regarding output floor phases implementing deeper Basel IV adjustments anticipated by end-decade timeline,

- Capital deployment decisions balancing buyback appetite against growth-focused reinvestments.

From the Valye perspective these indicators will shape how effectively Butterfield aligns its entrenched regional brand strengths with evolving offshore wealth management demands translating into sustainable risk-adjusted returns.

Disclaimer: This analysis is based solely on publicly available data including SEC filings [S#], recent news articles [N#], and company XBRL financial statements [F1] as of February 18th, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments