AMTD IDEA Group Strains for Stability Amid Slumping Revenue and Hotel Acquisitions

AMTD IDEA Group wrestles with a nearly 40% revenue decline while expanding its hospitality portfolio and growing its digital segment aggressively.

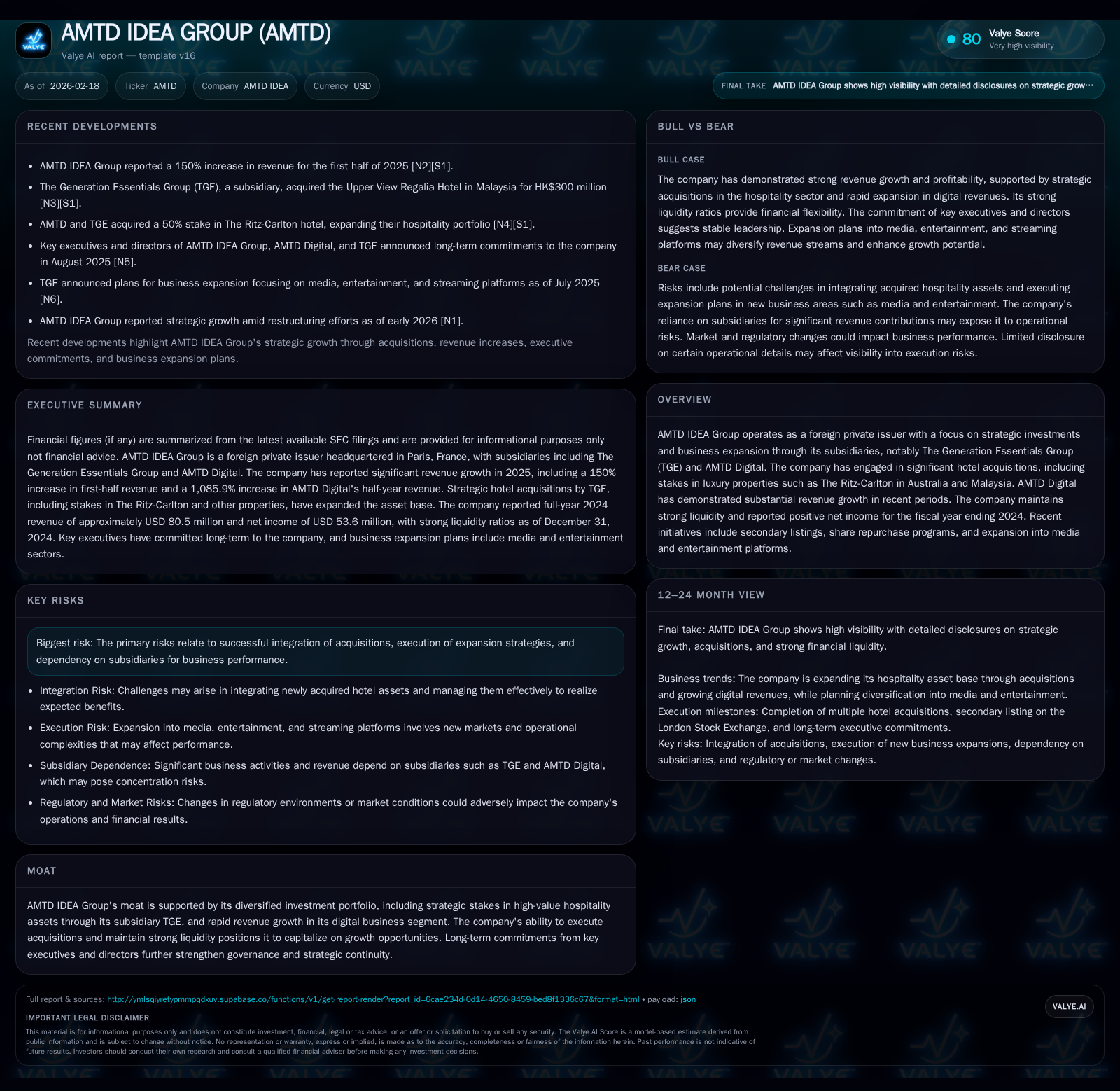

AMTD IDEA Group's fiscal 2024 results reveal a sharp contraction in revenue, down almost 39% year-over-year, contrasting with a positive net income driven by cost management and digital business expansion. Strategic acquisitions via its subsidiary, The Generation Essentials Group (TGE), notably large-scale luxury hotel purchases including stakes in Ritz-Carlton properties across Australia and Malaysia, aim to diversify earnings but introduce integration challenges. Additionally, AMTD Digital’s explosive revenue growth—surging over 10-fold in early 2025—provides potential upside amid corporate restructuring. The company maintains robust liquidity with a strong current ratio yet faces capital allocation tensions as it balances asset-heavy hospitality investments against the asset-light scalable digital platform. Going forward, successful integration of its acquisitions, digital expansion scalability, and the outcomes of secondary listings and buybacks will be critical milestones to watch.

Recent Financial Trajectory and YoY Drivers: A Tale of Divergence

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2024 | 80 | 54 | 8000 | -38.5% | -65.1% |

| 2023 | 131 | 153 | 72000 | ||

| 2022 | |||||

| 2021 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): CFO, OpInc, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2024 | 3.9 | |

| 2023 | 14.6 | |

| 2022 | 124 | |

| 2021 | 124 |

Source: SEC companyfacts cache [F1].

AMTD IDEA Group’s recent financial disclosures underscore a striking divergence between overall corporate results and the performance of its digital segment. Fiscal year 2024 revenues contracted sharply to $80.5 million from $130.9 million in FY 2023—a steep decline of approximately 38.5% [F1]. Net income also softened considerably, falling by over 65% to $53.6 million in FY 2024 from $153.4 million the prior year [F1]. However, this profitability retained a positive frame during revenue pressure largely due to disciplined cost management and improving margins in newer business lines.

Operating cash flow stagnated at around $5.16 million, overshadowed by minimal capital expenditures of merely $8,000—a near ninefold decrease from $72,000 in FY 2023 [F1]. This capex pattern suggests a deliberate holdback on investments while assimilating recent acquisitions and scaling organic initiatives carefully.

While the consolidated figures portray revenue setbacks typical in transitional phases marked by heavy acquisition activity, AMTD Digital—the company’s fast-growing tech-driven arm—reported a staggering increase of over 1,085% in revenue for the first half of 2025 [S6]. This asset-light digital platform contrasts markedly with AMTD’s asset-heavy expansions in hospitality through The Generation Essentials Group (TGE), highlighting an evolving dual-growth engine strategy balancing scalability against foundational asset accumulation.

Strategic Asset Acquisitions Bolstering Future Growth Potential

The Generation Essentials Group stands at the core of AMTD IDEA Group’s strategic pivot towards luxury hospitality assets. In late 2025 alone, TGE executed multiple Sale and Purchase Agreements (SPAs) adding roughly USD 300 million worth of premier hotel properties post-De-SPAC conversion [S3][S10]. Among these are significant stakes in The Ritz-Carlton Perth in Australia acquired for approximately A$280 million and the Upper View Regalia Hotel in Kuala Lumpur, Malaysia [S9]. Additionally, the New York Tribeca Hotel was brought under TGE’s umbrella within the same timeframe [S10].

These targeted acquisitions enhance AMTD's portfolio risk diversification by incorporating high-value real estate assets known for resilient cash flows within upscale segments less sensitive to cyclical downturns—a common valuation moat feature in luxury hospitality investment strategy.

The addition of these hotels diversifies AMTD’s earnings base beyond its rapidly growing but volatile digital operations. However, embedding such sizable hospitality assets introduces operational challenges including capital lock-up duration mismatches relative to digital ventures and necessitates sophisticated synergy extraction from property management efficiencies typical for institutional real estate portfolios.

Assessing Liquidity, Capital Structure, and Shareholder Returns

Liquidity metrics remain notably strong with total current assets surpassing current liabilities by over tenfold at fiscal year-end 2024—an exceptionally high current ratio near 10.6 [F1]. This outsized buffer affords financial flexibility during intense acquisition phases yet raises questions about optimal capital deployment efficiency given relatively low returns.

AMTD IDEA Group's stockholders' equity grew significantly year-over-year to $1.36 billion from $1.05 billion alongside flattening net income resulting in modest return on equity (ROE) approximating just under 4% for FY 2024 [F1]. This subdued ROE reflects early-cycle hallmarks common among companies reorienting their capital structures alongside integrating large physical assets that depreciate gradually.

Dividends paid historically have featured consistently through FYs 2020-22 denominated in HKD though no dividends or repurchase volumes were reported for FYs 2023-24 within available data [F1]. Notably, TGE announced a share repurchase program during late 2025 signaling management intent to enhance shareholder value strategically if liquidity permits [S5].

Balancing large-scale capital outlays toward hospitality assets against emerging digital ventures will test AMTD’s capital allocation acumen particularly given constrained free cash flow after acquisitions (~$5M CFO minus capex) [F1]. From a buy-side perspective, maintaining liquidity buffers aids defensive positioning but excess idle funds could dilute returns if reinvestment does not yield commensurate growth.

Digital Segment Surge: Scaling Amidst Corporate Flux

AMTD Digital has emerged as a pivotal driver amid corporate flux fueled by legacy revenue declines and heavy acquisition undertakings elsewhere within the group. Its reported half-year revenue jump exceeding an extraordinary scale—more than tenfold compared to prior comparable periods—signals strong monetization traction likely leveraging technology platforms emphasizing recurring revenue streams or rapid user base expansion strategies [S6][N1].

This technological division operates with asset-light characteristics enabling superior scalability relative to core hospitality businesses which demand extensive capital commitment and longer payback horizons.

While precise details on AMTD Digital’s product mix or monetization models are limited, the explosive top-line growth provides operational leverage that partially offsets the cyclical softness seen elsewhere on AMTD's consolidated books. From an industry native standpoint, such digital acceleration represents elemental hedging against external market volatility enveloping asset-heavy investments within physical accommodations.

Integration Risks and Execution Constraints on Expansion Strategy

Despite promising growth vectors both digitally and via high-value real estate purchases, risks loom surrounding AMTD IDEA Group's ability to effectively integrate its varied acquisitions into a cohesive operating model.

The company's own risk disclosures emphasize dependencies on subsidiaries’ performances combined with challenges commonly linked to post-merger integration (PMI), including cultural alignments, harmonizing operating cadences across diverse geographies (Australia, Malaysia, USA), regulatory compliance variances, and managing increased organizational complexity [S6].

Hospitality asset integration particularly demands meticulous coordination across property management standards to extract portfolio synergies without diluting brand prestige—a task compounded when conducted alongside simultaneously scaling nascent digital ventures.

Any delays or inefficiencies here could exacerbate financial pressures arising from reduced legacy revenues and heighten uncertainty regarding timing for full realization of acquisition-driven value accretion.

Forward-Looking Signals: Milestones to Monitor in 2026

Absent explicit earnings guidance or milestone projections beyond press releases as per latest filings [N1][S5], investors should track several key indicators during the forthcoming year:

- Completion pace and subsequent operational ramp-up of remaining announced TGE hotel acquisitions continuing post-De-SPAC restructuring.

- Performance trends stemming from secondary listing activities executed on London Stock Exchange showcasing enhanced access to international equity capital markets via TGE platforms [S8][S11].

- Continued trajectory of AMTD Digital’s rapid top-line growth supporting margin expansion and eventual contribution toward consolidated free cash flow improvement.

- Capital allocation updates reflecting realization or expansion of announced repurchase programs alongside rationalized reinvestment plans balancing asset-heavy versus asset-light businesses.

- Evolutions in cash flow robustness post-acquisition as CapEx commitments stabilize allowing operating cash flows greater reinvestment freedom.

In combination these signals will illuminate whether AMTD IDEA Group can normalize growth trajectories while resolving current tension points between divergent business segments.

Disclaimer: This analysis is based strictly on information available through public company filings as cited; it does not constitute investment advice or recommendations regarding securities ownership or transactions. Readers should conduct comprehensive due diligence tailored to their specific circumstances before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments