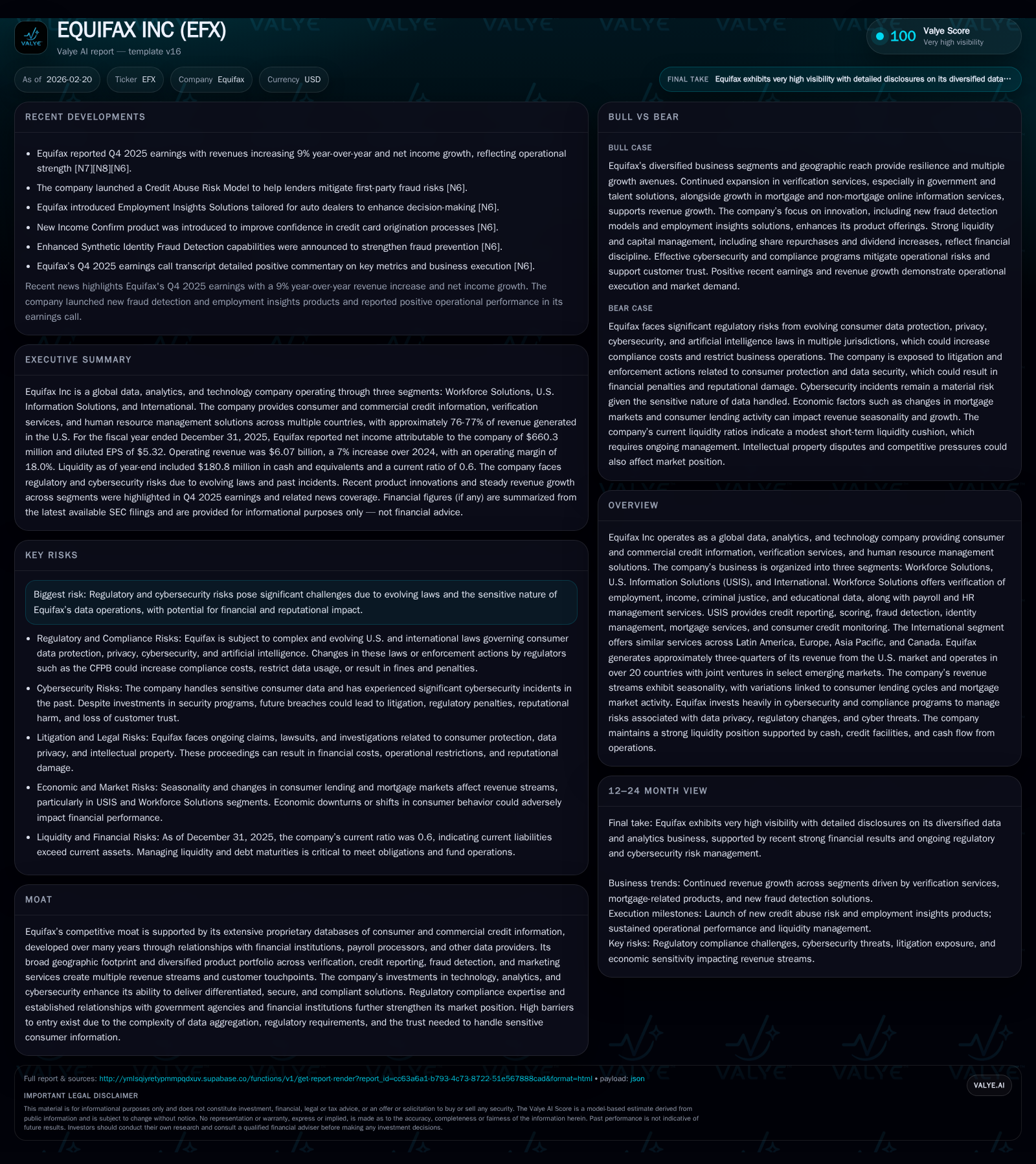

Equifax’s 2025 Earnings Reflect Steady Growth and Strategic Capital Allocation

Equifax posted moderate operating income growth, maintained robust cash flow, and navigated evolving regulatory risks in fiscal 2025.

In fiscal 2025, Equifax Inc. demonstrated steady financial performance characterized by a 5.1% year-over-year increase in operating income and a 9.3% rise in net income, supported by its dominant U.S.-centric portfolio across Workforce Solutions, U.S. Information Solutions, and International segments. Operating cash flow surged 22%, fueling considerable share repurchases after a period of dormancy and supporting a dividend increase. However, the company continues to face material regulatory headwinds from CFPB investigations and antitrust litigation in its Workforce Solutions business. Looking ahead, macroeconomic factors like interest rates and consumer lending trends, especially in mortgage markets, are critical to growth dynamics. Equifax’s strategic capital deployment and proprietary database assets underpin its competitive moat amidst these challenges.

Fiscal 2025 Financial Performance: Growth Patterns and Segment Contributions

Equifax recorded operating income of approximately $1.095 billion for the fiscal year ending December 31, 2025, reflecting a solid 5.1% increase over the prior year’s $1.042 billion [F1]. This marked an improvement following prior volatility with operating income dipping before rebounding in 2024 [F1]. Net income rose more robustly by 9.3% year-over-year to $660 million driven by margin expansion and effective cost control [F1]. Operating cash flow demonstrated particularly strong momentum, climbing by 22% to nearly $1.62 billion fueled by improved working capital management and profitable revenue streams [F1]. Meanwhile, capital expenditures were moderately trimmed by approximately 6%, signaling more optimized spending on technology infrastructure compared with previous years [F1]. The resulting free cash flow (operating cash flow less capex) reached roughly $1.13 billion in FY25 – providing ample liquidity for shareholder returns and reinvestment [F1].

Seasonal patterns remain notable within Equifax’s results: revenues from USIS Online Information solutions tend to be weakest in Q1 owing to cyclical softening in consumer lending activity while Workforce Solutions’ Employer Services revenue usually peaks early each year due to annual tax form processing like 1095-C filings [S1][S12]. Additionally, mortgage-related revenues commonly rise in Q2/Q3 coincident with elevated home buying activity during summer months impacting both USIS and Workforce Solutions segments [S1][S12]. This cadence requires nuanced interpretation on a quarterly basis but overall has not impeded annual upward trajectory.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 660 | 1616 | 1095 | 481 | +9.3% |

| 2024 | 604 | 1325 | 1042 | 512 | +10.8% |

| 2023 | 545 | 1117 | 934 | 601 | -21.7% |

| 2022 | 696 | 757 | 1056 | 625 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 233 | 928 | 1134 |

| 2024 | 193 | 813 | |

| 2023 | 192 | 0 | 516 |

| 2022 | 191 | 0 | 133 |

Source: SEC companyfacts cache [F1].

Note: Buybacks data not available for FY24; data sourced from [F1].

Platform of Proprietary Data Assets Driving US-Dominant Revenue Streams

Equifax’s business model leverages extensive proprietary consumer and commercial data repositories aggregated principally through longstanding partnerships with banks, payroll processors, tax authorities, and employers [F1][S16]. Approximately three-fourths of total revenues originate from the U.S., reinforcing the company’s leadership position domestically [S12]. Its business is divided into three segments:

- Workforce Solutions: Encompasses Verification Services (transaction- and subscription-based employment/income verification plus criminal justice and education data) together with Employer Services providing human resource outsourcing functions such as unemployment claims management, ACA compliance services, tax credit optimization, onboarding/I-9 services [S20].

- U.S Information Solutions (USIS): Primarily transaction-based Online Information products including credit reports/scoring/monitoring, fraud detection suites, identity verification solutions alongside subscription-oriented Financial Marketing Services used for risk management and customer acquisition analytics [S20].

- International: Spanning Latin America, Europe, Asia Pacific, Canada offering similar credit information products alongside debt collection technology support with regional customization reflecting local credit market differences [S24].

This segmentation allows balanced exposure between transaction-driven cyclical revenue (e.g., credit pulls tied to lending volumes) versus recurring subscription contracts (e.g., HR outsourcing or marketing analytics), diversifying cash flows and leveraging cross-segment synergies like fraud analytics layering into lending decisions [S20].

Regulatory and Legal Risks: CFPB Investigations and Antitrust Litigation Impact

Regulatory scrutiny presents an ongoing material risk vector for Equifax concentrated mainly around its Workforce Solutions unit’s compliance with the Fair Credit Reporting Act (FCRA) [S5][S10]. Since July 2023, the Consumer Financial Protection Bureau (CFPB) has issued multiple Civil Investigative Demands probing data accuracy practices and dispute handling procedures under FCRA rules [S5]. These investigations continue into early-2026 without resolution or penalty assessment so far but cloud future liability.

Concurrently since May 2024 there is pending class-action antitrust litigation alleging violations related to electronic income/employment verification services pricing within Workforce Solutions that could impose financial damages or operational constraints on this core product line if outcomes are unfavorable for Equifax [S5].

Broader litigation risks also stem from evolving privacy laws such as GDPR adaptations in Europe and multiple U.S state-level privacy statutes modeled after CCPA frameworks as well as anticipated artificial intelligence governance regimes potentially impacting algorithmic credit decisioning platforms deployed by Equifax [S10][S7]. These multijurisdictional complexities increase compliance costs meaningfully while simultaneously raising reputational exposure given the sensitivity of consumer financial data processed.

Future Growth Outlook Amid Economic and Sector-Specific Headwinds

Management commentary post FY25 earnings suggests optimism for improving quarterly results driven by sustained traction in credit monitoring growth within USIS Online Information despite macro uncertainty [N6][N7][N9]. Reported year-over-year revenue gains outside detailed here reached near or above high-single digits signaling resilience even against cautious consumer finance cycles exacerbated by inflationary pressure or rising interest rates [N7][N9].

However, ongoing challenges remain where mortgage-related revenue—significant for both USIS financial marketing services and portions of Workforce Solutions—is directly linked to fluctuating home purchase volumes sensitive to Federal Reserve interest rate policy moves causing higher borrowing costs [S12]. Given typical seasonality whereby home purchases spike in warmer quarters increasing transaction volumes seasonally even if slowing or plateauing over time creates oscillating revenue comparisons quarter-to-quarter necessitating judicious expectations from investors.

Monitoring shifts in consumer lending appetite broadly alongside regulatory developments impacting data use policies will be key indicators underpinning forward growth potential through FY26.

Capital Allocation Strategy: Dividends, Buybacks, and Investment Priorities

Capital deployment reflects a balance between steady shareholder returns through dividends along with opportunistic share repurchases aligned with free cash flow strength [F1][S6]. Dividends paid grew moderately from approximately $193 million in FY24 to nearly $233 million in FY25 representing an incremental payout consistent with modest EPS improvement supporting about a 14% ROE based on net income over equity at year-end ($4.6 billion) [F1].

Notably buyback activity resumed meaningfully after a hiatus; no repurchases occurred during calendar year FY24 contrasted against substantial buybacks approximating $928 million executed during FY25 – a reflection of enhanced liquidity from operating cash flows enabling valuation-driven discretionary repurchases without sacrificing investment capacity or balance sheet flexibility given low leverage profiles detailed below [F1][S6].

Capital expenditures declined approximately -6% year-over-year demonstrating ongoing efficiency optimization likely reflecting investments shifting towards software development and cloud infrastructure modernization supporting scalable solutions rather than large fixed asset outlays typical of older technology eras.

Operating Cash Flow Strength and Capex Optimizations

Operating cash flow has exhibited strong acceleration over recent years rising from $757 million in FY22 to nearly $1.62 billion in FY25—a compound annual growth rate exceeding ~27% illustrating operational leverage realized through scaling data services delivery combined with disciplined working capital management driving higher conversion of reported earnings into cash generation [F1].

Simultaneously capital expenditure reductions have contributed positively towards free cash flow generation expanding available funds for dividends or buybacks while retaining strategic IT reinvestment capacity essential for competitive differentiation through enhanced analytics capabilities and cybersecurity resilience critical given regulatory scrutiny.

The resulting free cash flow margin supports sustainable return of capital policies balancing external shareholder distributions against internal funding needs effectively.

Global Footprint and Emerging Markets Exposure

While the U.S is the largest market comprising circa ~77% of revenues equating roughly over three-fifths of consolidated operating income contribution given segment margins disparities between domestic versus international businesses the company maintains presence across Latin America (Argentina Brazil Chile Mexico Peru etc.), Europe (UK Ireland Spain Portugal), Asia Pacific (India Australia New Zealand Singapore Malaysia etc.) plus Canada which closely parallels USIS offerings adapted locally [S12][S24].

International operations feature both direct service offerings consistent with core USIS products such as credit reporting/scoring plus region-specific solutions supporting recovery management workflows particularly necessary in Latin America and parts of Asia Pacific emerging markets where credit infrastructures are less mature but growing rapidly via joint ventures or localized partnerships allowing calibrated risk exposure while leveraging cross-border data expertise.

Despite geographical diversification emphasis remains on heightening penetration in key growth regions while maintaining controlled investment levels aligned with local regulatory environments reducing operational complexity risks alongside domestic scale dominance.

Investor Considerations: Monitoring Key Upcoming Milestones

Investors should prioritize tracking developments regarding the unresolved CFPB investigation outcomes—the timing remains uncertain but any enforcement actions could materially impact operating profit margins or necessitate product changes particularly within Workforce Solutions which carries heavier regulatory oversight burdens [N9][N10][S5].

Additionally monitoring quarterly revenue patterns against seasonal expectations tied especially to mortgage cycle fluctuations will be essential given how housing market softness or strength cascades directly into certain product volumes impacting earnings volatility despite overall business diversification.

Broader regulatory shifts on data privacy legislation expansion across states/countries as well as any forthcoming AI oversight regulations modifying analytical tool usage represent forward-looking uncertainties potentially adding compliance costs or restricting product functionality requiring agile adaptation strategy evaluation.

Lastly capital allocation trends post heavy FY25 buybacks will be pivotal whether share repurchase cadence sustains contributing further shareholder value enhancement versus increased M&A activities remain unclear but worth observing given sizeable liquidity buffers retained currently.

Disclaimer: This analysis is based on publicly available financial statements dated through February 2026 ([F1],[S#]) alongside recent news transcripts ([N#]). It presents historical facts, contextual industry insights, identified risks, and forward-looking considerations without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments