MetLife’s New Frontier Strategy Boosts Asset Management Amid Profitability Pressures

MetLife transitions its segment structure to emphasize asset management growth while managing regulatory and market headwinds.

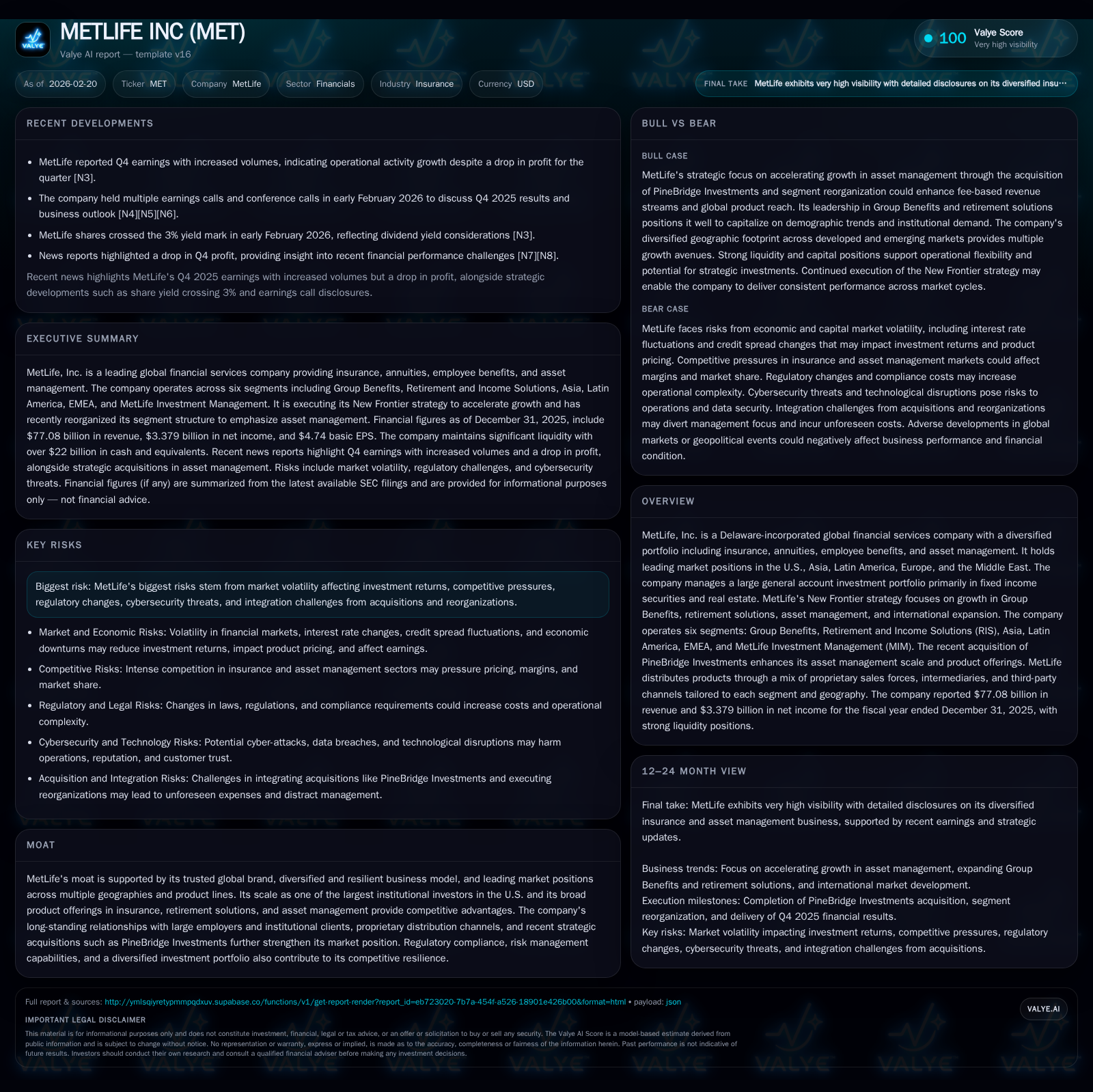

MetLife Inc. has reported steady revenue growth driven by its diversified insurance and asset management operations. The company’s 2025 reorganization elevated MetLife Investment Management (MIM) as a key growth pillar, supported by the acquisition of PineBridge Investments. Despite an 8.6% revenue increase year-over-year, net income declined due to profitability pressures and market volatility. MetLife’s strategic emphasis on Group Benefits, retirement solutions, and international expansion reflects its efforts to maintain resilience amid competitive and regulatory challenges. Capital allocation remains disciplined with continued dividends and share repurchases, underpinning a roughly 12% return on equity.

Company Overview and Strategic Focus

MetLife Inc., incorporated in Delaware in 1999, is a leading global financial services firm with a core footprint spanning the United States, Asia, Latin America, Europe, the Middle East, and Africa [S1][S18]. Its comprehensive portfolio includes insurance products (life, accident & health), annuities, employee benefits programs, retirement solutions, and institutional asset management.

The company’s recent strategic pivot under its "New Frontier" strategy builds on previous initiatives aimed at simplification and differentiation. This framework prioritizes accelerating growth through four focused areas: extending leadership in Group Benefits; leveraging its unique retirement platform; expanding asset management capabilities; and deepening presence in high-growth international markets [S1].

In late 2025, MetLife enacted a significant segment reorganization which established MetLife Investment Management (MIM) as a standalone reportable segment—previously embedded within Corporate & Other—to underscore the strategic priority of asset management growth [S1][S18][S25]. Concurrently, the formerly reported MetLife Holdings segment was removed from reporting prominence with certain products shifted into Group Benefits or Retirement and Income Solutions (RIS).

The acquisition of PineBridge Investments at the end of 2025 marks a critical milestone in bolstering MIM's scale globally as well as enhancing its product diversity spanning fixed income, real estate debt/equity strategies, alternatives like private equity and middle market lending, multi-asset class solutions, and insurance-tailored advisory services [S25].

Historical Financial Performance

Over the past four years ending FY2025, MetLife demonstrated steady revenue growth punctuated by strategic adjustments in business mix:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 77.1 | 3.4 | 17.1 | 6.1 | +8.6% | -23.7% |

| 2024 | 71.0 | 4.4 | 14.6 | 6.0 | +273.1% | +629.2% |

| 2023 | 19.0 | 0.6 | 13.7 | -72.8% | -76.1% | |

| 2022 | 69.9 | 2.5 | 13.2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 1509 | 2.9 | 11.9 |

| 2024 | 1527 | 3.2 | 16.1 |

| 2023 | 1566 | 3.1 | 2.0 |

| 2022 | 1598 | 3.3 | 9.4 |

Source: SEC companyfacts cache [F1].

^Note: The sharp drop in reported revenues for FY2023 likely reflects a change in segment reporting or restatement that should be interpreted cautiously.

The most recent fiscal year recorded an increase in operating cash flows of approximately +17%, strengthening liquidity for ongoing capital deployment [F1]. Dividends have been maintained around $1.5 billion annually with share repurchase activity remaining robust near $3 billion per year over recent periods [F1]. Notably, net income contracted substantially (-23.7% YoY) despite rising operating income—likely due to increased investment volatility or non-operating charges detailed in quarterly disclosures [N3][N14].

Business Segments and Growth Drivers

Group Benefits

This U.S.-based unit enjoys leadership in group insurance through longstanding relationships with large employers offering life insurance, dental coverage, disability benefits (short- and long-term), paid family/medical leave programs, accidental death & dismemberment insurance alongside individual disability policies [S18].

Retirement and Income Solutions (RIS)

RIS concentrates on retirement savings vehicles including fixed annuities and pension products designed primarily for defined contribution plans as well as corporate plan sponsors seeking pension risk transfer opportunities [S18].

International Operations

MetLife operates across Asia—with Japan as its largest market—Latin America (Mexico and Chile prominent), alongside Europe/Middle East/Africa (EMEA). Distribution mixes vary: Japan leans strongly on career/general agencies; other Asian territories utilize a blend of bancassurance plus broker networks; Latin America employs selective captive agencies combined with direct digital marketing; EMEA combines bespoke channels aligning with local market intricacies [S18][S23].

MetLife Investment Management (MIM)

Following the acquisition of PineBridge Investments in December ’25, MIM's scale and product breadth notably expanded servicing institutional clients such as pension funds, insurers, sovereign wealth entities with capabilities across public/private fixed income strategies; real estate debt/equity; global equities; alternatives including private equity/middle market credit; multi-asset solutions; plus insurance-focused portfolio advisory services [S25].

This segment’s elevation signals acceleration of asset management as a key engine for profit diversification beyond traditional insurance underwriting.

Forward-Looking Growth Prospects

MetLife aims for organic expansion through four primary pillars aligned with New Frontier:

- Group Benefits: Continued focus on deepening employer relationships coupled with innovative employee benefit solutions.

- Retirement Solutions: Leveraging pension risk transfer trends especially amidst evolving U.S./Chile pension reforms that could shift demand profiles over next several years [S9].

- Asset Management: Integration synergies from PineBridge support fee-based revenue acceleration amid strong demand for private credit and sustainable investing strategies.

- International Markets: Growth emphasis on high-potential regions especially Asia excluding Japan given demographic expansions.

However, these prospects face headwinds including competitive pricing pressures across group insurance sectors; fee compression risks within institutional asset management due to increasing passive products competition; regulatory uncertainties such as pension reform implementation timing; cybersecurity concerns affecting digital distribution platforms; and integration complexities post-acquisitions [S7][S26].

Key milestones identified involve quarterly earnings performance tracking volumes in Group Benefits and RIS segments alongside client asset inflows at MIM post-PineBridge acquisition [N3][N4][N11]. Close monitoring of regulatory developments impacting pension funding rules or health insurance reforms will be essential over the medium term.

Capital Allocation and Returns Analysis

Capital deployment has been characterized by consistent dividends alongside sizeable buybacks contributing to shareholder returns:

- Dividends paid approximated $1.51 billion in FY25 following similar levels over recent years [F1][S6].

- Stock repurchases totaled $2.88 billion last year down slightly from pre-pandemic levels yet sustaining substantial capital return activity [F1][S27].

- Operating cash flow reached ≈$17 billion in FY25 providing ample internal liquidity for continued shareholder return alongside growth investments.

Estimating return on equity based on latest annual net income against shareholders’ equity yields an ROE near ~11.9%, reflecting disciplined earnings generation despite margin pressures partially attributable to market movements impacting investment portfolios or claims reserves [F1]. This level aligns reasonably within industry standards given MetLife’s sizable investment exposure coupled with diversified underwriting lines.

Competitive Positioning and Moat Considerations

MetLife’s moat derives from brand reputation cultivated over decades globally paired with a broad portfolio spanning core insurance lines plus differentiated asset management capabilities that leverage scale advantages [S4][S13]. The company maintains proprietary distribution channels augmented by intermediaries enabling reach across various customer bases while sustaining resilient client relationships especially among large corporate employers.

Its status as one of the largest U.S.-based institutional investors affords meaningful influence over fixed income markets underpinning general account portfolio strategies balanced between corporate bonds, structured products, real estate investments complemented by alternative assets managed through MIM [S1][S25]. Regulatory compliance readiness alongside advanced risk management helps preserve credit ratings critical to competitive positioning.

Challenges include persistent fee compression across asset manager peers due to competitive landscape intensifying adoption of low-cost passive funds alongside pressure to innovate digitally driven product offerings responsive to shifting consumer preferences including AI-enabled underwriting enhancements [S24][S26][S22]. Consolidation trends among brokers/distributors also complicate access dynamics necessitating constant adjustment of partnership models.

Risks Highlighted by Regulatory Filings

Principal risks encompass:

- Market Risk: Volatility influencing investment returns tied heavily to fixed income assets involves potential rating downgrades affecting capital adequacy requirements [S8][S29].

- Regulatory Risk: Changes impacting pension systems (notably Chilean reforms), health care legislation raising costs unpredictably along with emerging fiduciary duty frameworks under ERISA alter product attractiveness or distribution economics [S9][S10][S21].

- Cybersecurity Threats: Heightened scrutiny requires substantial IT security investments under complex jurisdictional mandates elevating operating expenses while leaving residual breach risk exposure [S28].

- Operational Risks of Acquisitions: Integration challenges post-PineBridge acquisition coupled with legacy run-off blocks add uncertainty around cost synergies realization or unanticipated liabilities [S15][S19].

- Competition: Pressure arises not only from traditional insurers but also banks, broker-dealers and fintech entrants exploiting embedded insurance opportunities within digital ecosystems disrupting sales models [S4][S26].

These factors collectively require vigilant governance complemented by robust scenario testing underpinning reserve assumptions ensuring resilience through economic cycles [S7][S16].

Conclusion: Key Metrics To Monitor Going Forward

While explicit future guidance was not detailed beyond known strategic imperatives ([N3],[N11],[N13]), observers should watch:

- Quarterly volume trends across Group Benefits & RIS reflecting employer spending patterns.

- Asset inflows/outflows details from MIM indicating progress post-PineBridge integration.

- Regulatory developments regarding pensions particularly Chilean phased reforms beginning rollout circa ’27.

- Earnings quality relative to investment income volatility especially given current macro uncertainties.

- Capital generation capacity sustaining dividend/share repurchase programs without impairing statutory surplus buffers.

Maintaining balance between leveraging global scale advantages while managing complexity inherent in multi-jurisdictional operations will define how effectively MetLife converts its strategic vision into durable financial performance.

Disclaimer: This analysis is intended solely for informational purposes based on available data as of February 20, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments