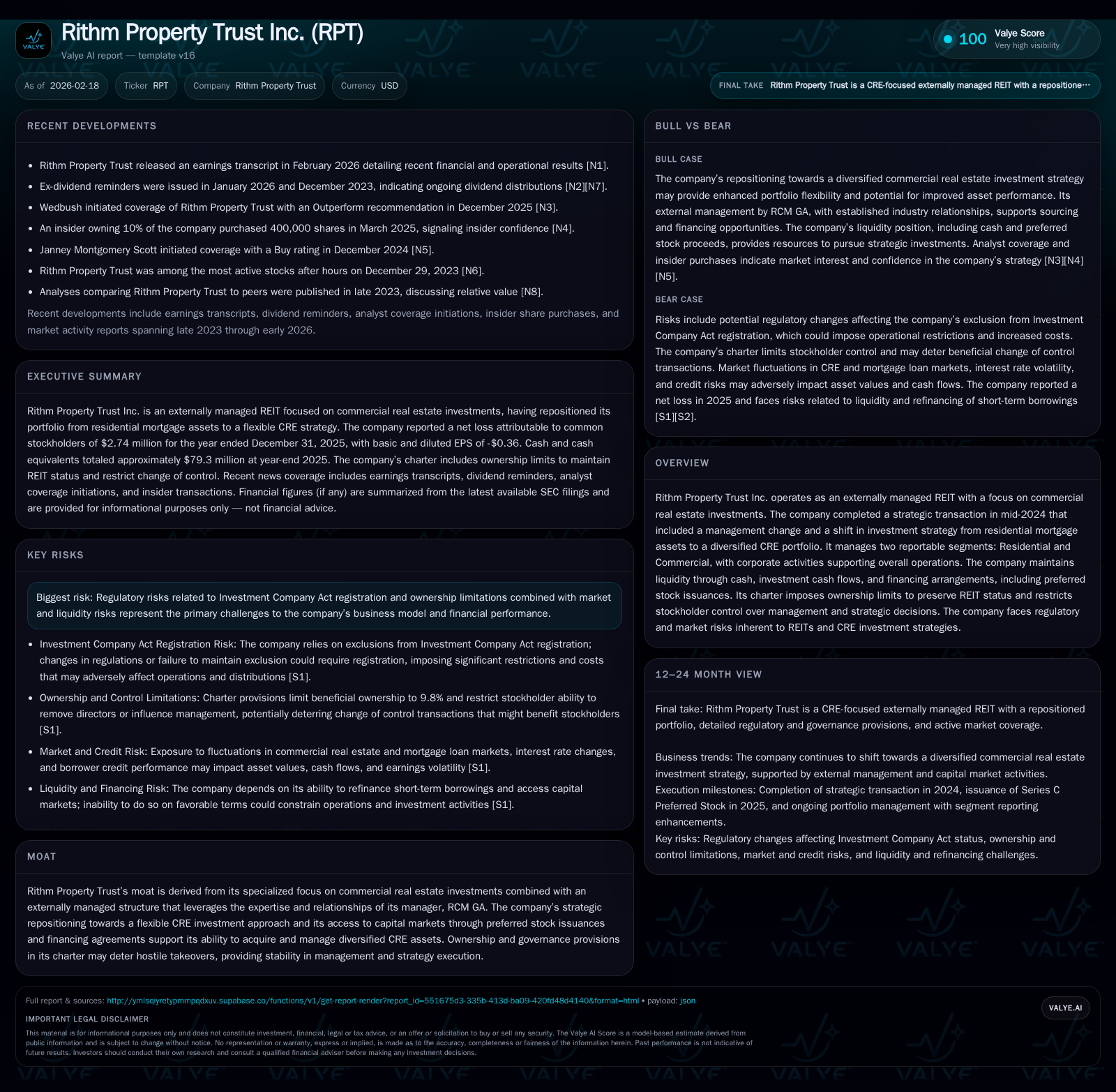

Rithm Property Trust’s Strategic Reset Spurs Mixed Financial Results

Rithm Property Trust’s mid-2024 strategic pivot towards diversified commercial real estate triggered a net income turnaround, juxtaposed with cash flow stress and regulatory challenges.

After several years of losses rooted in its residential mortgage focus, Rithm Property Trust executed a transformative strategic transaction in mid-2024 which replaced management and shifted investment emphasis to a diversified commercial real estate portfolio managed by RCM GA. This repositioning yielded a positive net income of $1.47 million in FY2025, an over 100% improvement year-over-year, signifying a tentative financial turnaround. However, the company faced deteriorating operating cash flows and negative free cash flow, spotlighting liquidity pressures amid the business model shift. Its capital structure remains complex, featuring secured bonds payable, repurchase financing agreements tied to short maturities and SOFR-linked rates, and recently issued Series C preferred stock raising $50.8 million. Governance provisions limiting ownership concentration underpin its REIT status but constrain strategic flexibility. Going forward, successful refinancing of short-term debt and execution on CRE acquisition opportunities amid funding cost headwinds will be pivotal milestones to watch.

Evolution From Residential Mortgages to Diversified Commercial Real Estate

Rithm Property Trust's defining moment arrived with the June 11, 2024 strategic transaction that effectively rewrote its investment playbook and leadership architecture [S1]. This transaction introduced RCM GA as the external manager under a new Management Agreement, replacing prior management arrangements tied closely to residential mortgage asset strategies. The company concurrently shifted from its historical emphasis on acquiring re-performing loans (RPLs) and non-performing loans (NPLs) secured by residential properties toward a flexible commercial real estate (CRE) investment strategy encompassing originating, acquiring, and managing a diversified array of CRE-related assets [S1][F1].

Operationally, this pivot included transitioning loan servicing responsibilities from Gregory Funding LLC to Newrez LLC—an affiliate of Rithm and its manager—on June 1, 2024 under new servicing agreements maintaining comparable terms [S1][S26]. The Residential segment remained responsible for legacy mortgage portfolios undergoing run-off or asset sales, while the fledgling Commercial segment undertook managing CMBS portfolios, commercial mortgage loans, equity JV interests, and more actively sought CRE acquisition opportunities including high-profile investments such as an indirect minority interest via affiliated aggregator vehicles in the PGRE Portfolio consisting of marquee office properties across New York City and San Francisco [S24][S25].

This strategic metamorphosis sets the foundational platform for future growth by capitalizing on market dislocations within CRE financing markets as traditional lenders exhibit retrenchment amid higher interest rate environments [N1].

Historical Financial Performance: A Turnaround Narrative

Financially, Rithm’s transformation is most palpably reflected by its profit-and-loss trajectory over the past four years (Table 1). The company recorded persistent net losses each year from FY2022 through FY2024 — notably -$15.0 million in FY2022 increasing sharply to -$47.1 million in FY2023 before reaching an all-time low of -$91.8 million in FY2024—all tied primarily to exposures within its residential mortgage assets during increasingly challenging interest rate climates coupled with impaired servicing outcomes [F1].

The pivotal FY2025 witnessed a positive inflection point: net income swung into positive territory at $1.47 million — representing an astonishing 101.6% year-over-year improvement relative to the steep loss in FY2024 [F1]. This profitability uptick is attributable largely to earnings contributions from the nascent Commercial segment alongside lower operating expenses post-restructuring and favorable accounting recognition related to portfolio repositioning [S18][N1].

However, while net income improved markedly, return on equity remains subdued at approximately 0.5% given the still-large equity base of roughly $291.6 million at end-FY2025 [F1]. This reflects a nascent stage turnaround where profit generation is emerging but not yet robust enough to meaningfully lift returns.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 1 | -8 | +101.6% | |

| 2024 | -92 | 0 | -95.1% | |

| 2023 | -47 | -46 | 0 | -213.6% |

| 2022 | -15 | 1 | 27000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0.5 | ||

| 2024 | -37.2 | ||

| 2023 | 0 | -46 | -15.2 |

| 2022 | 5 | 1 | -4.5 |

Source: SEC companyfacts cache [F1].

Note: Capex data insufficient for multi-year reporting; Revenue & OpInc not disclosed; CFO = Operating Cash Flow; ROE approximated as Net Income / Equity.

Analyzing Cash Flow Volatility Amid Business Model Shift

The flip side of improving profitability is manifested starkly in cash flow dynamics where FY2025 saw operating cash flows plunge into negative $8.3 million—a deterioration from modest positive $0.29 million generated in FY2024 despite improved net income results [F1][S6]. This discordance underscores timing mismatches inherent in moving away from residential mortgage portfolios toward an actively managed commercial loan investment stance.

The company's operating cash outflows likely stem from increased working capital demands related to new acquisitions such as unfunded portions of commercial loans (~$4.2 million available for draw), investments into joint ventures like PGOP with associated capital calls (up to $7.5 million contingent), and temporary timing gaps between recognizing revenue under accrual accounting versus actual cash receipts [S5][S16]. These pressures are exacerbated by margin call risks under short-term repurchase financing agreements that require posting additional collateral if asset values decline with market volatility [S8][S14].

Negative free cash flow follows logically due to cash consumed above operating incomes and minimal capex beyond acquisition activities [F1][S6]. Such liquidity strain makes renewable access to short-term borrowings critical for operations—a known risk given potential credit tightening conditions affecting rollover capabilities going forward.

Capital Structure, Financing Tactics, and Preferred Equity Role

Rithm operates a multi-layered capital structure blending secured bonds payable predominantly linked to securitized mortgage loans with repurchase financing agreements bearing variable interest tied typically to one-month SOFR spreads subject to floors around 75–90% advance rates per asset collateral values [S4][S8]. These repurchase facilities are effectively collateralized borrowings callably refinanced often on short durations (90 days), imposing constant rollover risks compounded by margin call exposures when underlying collateral fair value declines materially [S6][S16].

In August 2022 prior senior notes (the "2027 Notes") totaling $110 million carry a fixed coupon initially at 8.875%, later adjusted upwards by 100 bps due to rating downgrade triggered clause—now yielding ~9.875%, paid semi-annually until maturity September 2027 [S9]. This elevated cost reflects broader credit pressure on borrowers and funding markets faced by mortgage REITs currently.

A significant liquidity bolster came through issuance of approximately 2 million shares of Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock during early 2025 raising net proceeds near $50.8 million after underwriting deductions; about one-fifth purchased by manager affiliates reinforcing close alignment [S3][S5]. No recent common stock offerings or buybacks occurred implying prioritization of supporting balance sheet resilience over shareholder distributions beyond dividend obligations.

Leverage covenants imposed require maintaining tangible net worth above $240 million alongside minimum liquidity ($30 million+) levels while keeping consolidated recourse indebtedness relative to equity capped at max around four times excluding secured bonds payable instruments—which structurally limits excessive gearing but allows continued tactical borrowings for asset deals [S4][S6].

Governance, Regulatory Parameters, and Ownership Constraints

Governance is tightly controlled via charter provisions curbing any one stockholder's ownership share below thresholds needed for exclusive control coups—effectively shielding managerial continuity aligned with RCM GA's expertise [S1][N1]. These ownership ceilings also facilitate preservation of REIT status critical for tax efficiency.

Rithm relies heavily on Investment Company Act exemptions—specifically Sections 3(c)(5)(C) or (6)—dictating that qualifying real estate assets must constitute at least 55–80%+ of unconsolidated subsidiary assets limiting portfolio composition flexibility and influencing dispositional timing so as not to trigger registration demands that bring restrictive investment constraints such as limits on unsecured borrowing or affiliate transactions [S1].

Such regulatory tightropes form both moat elements by deterring hostile takeovers due to anti-concentration byzantine rules combined with an externally managed structure where RCM GA acts as investment decision engine insulated from stockholder micromanagement.

Investment Outlook: Growth Drivers and Headwinds in CRE Markets

The recalibrated 'flexible CRE investment strategy' positions Rithm squarely within evolving market opportunities created by tightening traditional CRE lender credit boxes sparking widespread refinancing dislocations where non-bank capital can step in for risk-adjusted returns unavailable elsewhere [N1][S1]. Origination pipelines including mezzanine lending layers or preferred equity investments capture upstream yield premiums offsetting elevated funding costs.

Nonetheless, challenging macro conditions persist including rising interest rates increasing securitization debt costs via floating-rate resets impacting margins plus borrower credit deterioration signals especially in stressed CMBS tranches necessitating active credit management vigilance—a reality underscored by lingering elevated delinquency metrics across certain CMBS vintage cohorts [N1][S27] (industry context).

Market disruptions coupled with continuous funding cost inflation could restrain deal volumes or prompt tighter underwriting parameters constraining rapid portfolio growth velocity despite abundance of demand for creative capital solutions.

What to Watch: Upcoming Milestones and Market-Driven Variables

Explicit company forecasts remain limited; consequently key markers will center on successful refinancing or rollovers of short-maturity repurchase facilities without onerous covenant easements or expensive spreads that could constrict acquisition firepower [N1][S6]. Monitoring scheduled repayments of secured bonds payable maturing through late-2026/early-2027 will also be telling for capital adequacy.

Other signals include deployment pace into CRE asset classes within commercial loans/JV interests indicating execution discipline repairing investor confidence—as well as returns trending toward sustainable positive operating cash flows balancing growth ambitions against liquidity demands.[N1]

Further capital raises or equity issuance beyond existing preferred stock will be scrutinized for dilution impact versus necessity stemming from borrowing restrictions or market dislocation fallout.

Balancing Stability and Flexibility in Capital Deployment

Capital allocation decisions demonstrate prudence: absence of recent common stock buybacks or elevated dividend payouts corresponds with modest approximate ROE near half percent given emergent profits but substantial legacy equity base [F1][S29]. Dividends declared approximated $11 million on common shares alongside accrued preferred dividends emphasizing mandatory REIT distribution compliance without aggressive yield signaling [S11][S29].

Equity raised via Series C preferred issuance enhances dry powder availability cushioning refinancing risks but maintains financial discipline amidst volatile CRE sector fundamentals fraught with inflationary pressures and cyclical uncertainties.

In aggregate, Rithm appears focused on preserving balance sheet flexibility while gradually building out its commercial real estate exposure framework awaiting more stable macro tailwinds before ramping shareholder returns aggressively.

Disclaimer: This report provides descriptive analysis based on publicly available filings including SEC reports [S#], news transcripts [N#], and quantitative data from XBRL companyfacts cache [F1] as of February 18, 2026 without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments