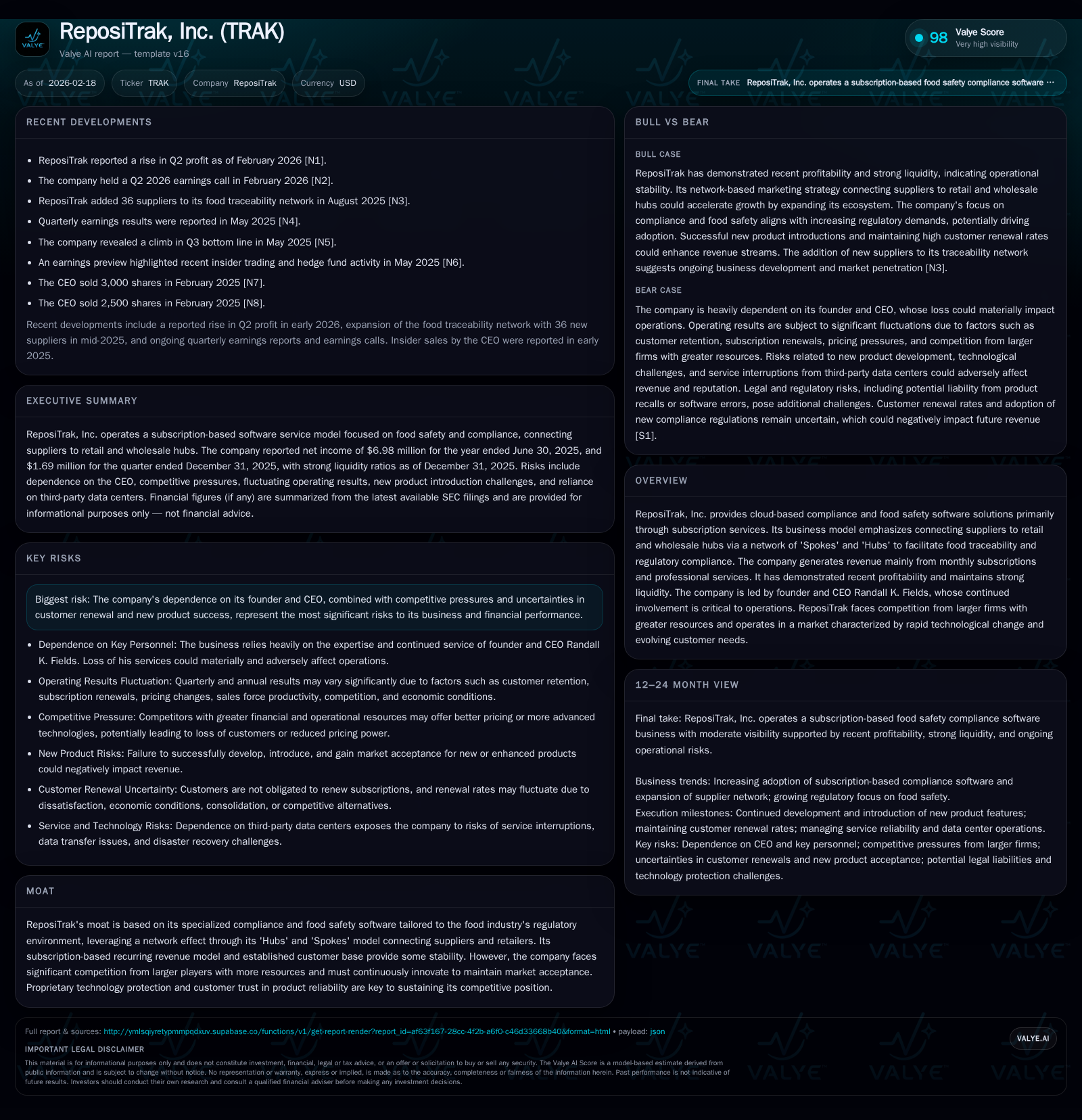

ReposiTrak's Growth Trajectory: Subscription Model, Network Effects, and Profitability

ReposiTrak advances profitability by leveraging its subscription-based hub-and-spoke network amid evolving food safety compliance demands.

ReposiTrak, Inc. has demonstrated steady revenue and profit growth driven by a subscription-based SaaS model integrated through a network of retail and wholesale ‘Hubs’ and connected suppliers (‘Spokes’). The company’s specialized food safety compliance platform captures sticky recurring revenues supported by regulatory-driven demand. While competitive pressures from larger firms and operational dependency on its founder CEO present risks, ReposiTrak’s strong cash flows, robust liquidity, and disciplined capital allocation underscore a solid financial position. Regulatory timing shifts such as the FSMA 204 deadline extension could moderate near-term adoption but also extend the opportunity runway. Investors should track renewal dynamics, network expansion, and technology innovation milestones as critical future growth indicators.

Evolution of Revenues and Profit Drivers: Analyzing Historical Performance

ReposiTrak has exhibited consistent year-over-year growth over the past several fiscal years marked by incremental revenue gains paired with notable expansions in operating profitability. Its fiscal year ends on June 30; data through FY2025 show total revenues stable around $21 million with a modest compound increase—specifically about 4.8% YoY growth comparing the latest annual period to prior reporting cycles [F1]. Despite relatively flat top-line variation triggered partly by macroeconomic conditions affecting customers' tech budgets, the firm's operating income nearly jumped by 24%, reaching over $6.2 million in fiscal ending June 2025 [F1],[S2]. This reflects improved operating leverage in its Software-as-a-Service (SaaS) delivery model.

Net income mirrored this performance with a gain of roughly 17.1% YoY to nearly $7 million for FY2025—the highest earnings point recorded in the relevant dataset—indicating effective cost management amid rising revenue contributions [F1]. The company’s ability to convert incremental sales into bottom-line profits underscores multiple margin expansion levers including scaling subscription volumes alongside fixed development costs.

Operating cash flow trends parallel earnings trajectory; CFO increased more than 20% year-over-year peaking close to $8.4 million most recently, supporting robust internal funding capabilities for infrastructure or shareholder returns [F1]. Although capital expenditures remain minimal—less than $16K in FY2025—the effort centers on platform maintenance rather than large-scale IT capital investment, consistent with SaaS sector norms.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 7 | 8 | 6 | 15965 | +17.1% |

| 2024 | 6 | 7 | 5 | 73317 | +6.6% |

| 2023 | 6 | 9 | 5 | 133944 | +39.6% |

| 2022 | 4 | 6 | 4 | 50823 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 1656377 | 0 | 8 |

| 2024 | 1721657 | 2 | 7 |

| 2023 | 1414912 | 1 | 9 |

| 2022 | 586444 | 6 | 6 |

Source: SEC companyfacts cache [F1].

Note: Complete revenue data for these years was not fully available from provided tags; percentages are calculated based on available operating income/net income figures primarily for FY2024-25 comparisons.

Subscription Model and Network Effects Drive Growth

ReposiTrak's core value proposition is anchored in its cloud-based food safety compliance software delivered primarily via monthly subscriptions supplemented by professional service fees during onboarding or upgrades [S10]. The company structures its ecosystem around “Hubs” (retail/wholesale centers) connecting multiple “Spokes” (suppliers), enabling seamless traceability across supply chains.

This hub-and-spoke architecture fosters strong network effects: as more Hubs join, supplier connectivity increases, enhancing switching costs and driving subscription renewals [S6]. Recurring monthly revenues form the backbone of financial stability but are subject to renewal rate variability influenced by customer satisfaction, pricing changes, competition, and broader economic conditions [S1],[S8].

Competitive Dynamics and Innovation Challenges

Operating within a competitive market featuring larger vendors with greater resources poses ongoing challenges to ReposiTrak’s growth trajectory [S12],[S1]. Protecting proprietary technology is critical yet complicated by low capital expenditure levels focused mainly on platform upkeep rather than expansion [F1].

Success depends on timely product enhancements aligned with evolving regulatory requirements and customer expectations for reliability—especially given the critical nature of food safety reporting during recalls or contamination events [S4],[S7]. Upselling professional services aids margin improvement but requires careful management of client experiences.

Regulatory Environment Impacts Adoption Timing

A key growth driver is regulatory compliance pressure under FDA’s Food Safety Modernization Act (FSMA), particularly Section 204(d), mandating electronic recordkeeping for covered foods [S9],[N2]. Originally effective January 20, 2026, this deadline was extended to July 20, 2028 due to industry readiness concerns.

This extension may delay immediate customer adoption but provides a longer runway for market penetration and technology integration investments among retail hubs and suppliers [S16],[N2]. Potential further delays or modifications could affect near-term revenue visibility.

Financial Position: Liquidity, Cash Flows, Dividends, and Buybacks

ReposiTrak maintains strong liquidity with current assets roughly five times current liabilities (current ratio approx. 5.45x), reflecting prudent working capital management [F1],[S17]. Operating cash flows have grown steadily with FY2025 generating about $8.42 million against minimal capex ($16K), yielding substantial free cash flow ($8.4 million).

Capital allocation balances shareholder returns via quarterly dividends totaling approximately $1.65 million in FY2025 with modest share repurchases near $200K annually after earlier larger buyback programs [F1],[S14],[S21]. Dividend policy remains discretionary based on earnings sustainability.

Equity stands at about $49.5 million with an approximate return on equity of 14%, consistent with profitable enterprise SaaS providers balancing growth and returns.

Key Risks: Leadership Dependency & Market Variables

The company identifies significant reliance on founder-CEO Randall K. Fields as a material operational risk; loss or reduced effectiveness could adversely impact strategic execution [S1],[S8].

Renewal rate fluctuations pose ongoing challenges amid competitive pricing pressures and potential customer dissatisfaction risks linked to product performance issues including software errors or integration difficulties [S7],[S13]. Security breaches represent another risk factor given the sensitive data handled within its cloud environment [S9],[S25].

Investor Considerations: Monitoring Milestones & Outlook

While specific future milestones or guidance are not disclosed in provided materials, investors should focus on metrics such as subscription renewal rates, expansion of retail/wholesale Hubs within the network, successful new product feature rollouts, and regulatory developments impacting adoption timelines.

Continued innovation aligned with food safety regulations combined with maintaining high service reliability will be central to sustaining competitive advantage.

Disclaimer: This analysis does not constitute investment advice but aims to provide informed insights based on publicly available information as of February 18, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments