Orion Bliss Corp.'s Quest for Scale in Natural Hair Care Products

Exploring Orion Bliss’s early financial hurdles and strategy to grow its natural ingredient-based Milk_Shake hair care brand.

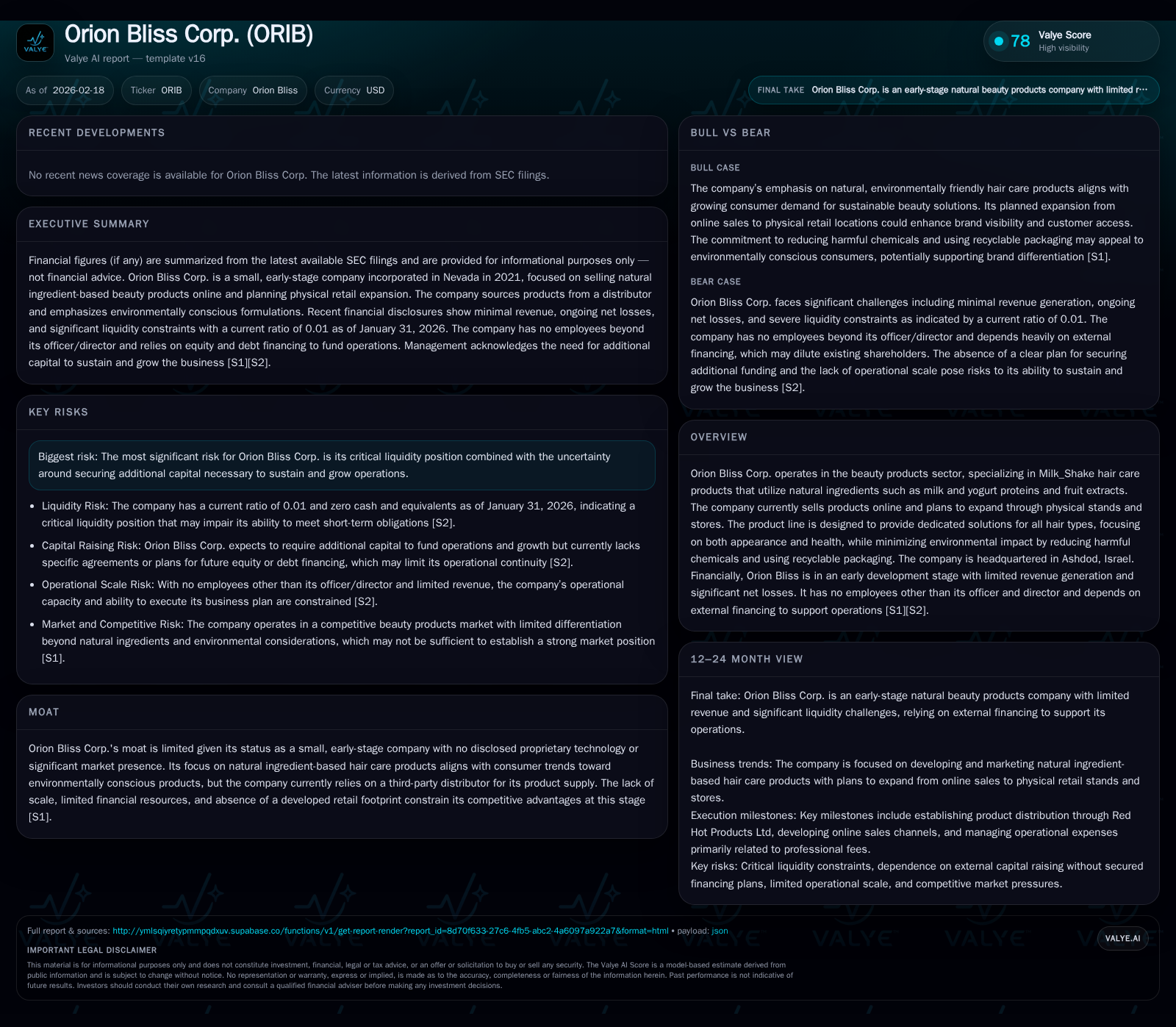

Orion Bliss Corp. is a nascent player focusing on natural hair care products under the Milk_Shake label, emphasizing formulations with milk and yogurt proteins and fruit extracts. Despite a significant revenue surge in 2025, the company remains heavily unprofitable with acute liquidity concerns, operating without employees other than its officer/director. Growth hinges on expanding from online sales into physical retail stands and stores, yet the absence of proprietary technology and scale dampens competitive advantages. The firm relies on external capital infusion, facing dilution risks amid uncertain financing plans. Stakeholders should monitor funding access, revenue trends, and operational expansion execution as critical near-term developments.

From Inception to Early Revenue Growth: Tracking Historical Performance

Orion Bliss Corp., incorporated in Nevada in 2021, has positioned itself within the beauty products sector through the niche of natural ingredient-focused hair care products under the Milk_Shake brand. Historically, revenue was negligible from inception through FY2023, with modest upticks seen briefly (e.g., $600 in FY2023). However, FY2024 saw a sharp dip back to $500 before a striking surge to approximately $26,000 in FY2025—representing a staggering 5103% year-over-year growth [F1]. This spike may correlate with initial scaling efforts or broader market acceptance.

Yet this top-line improvement masks persistent negative profitability trends. Operating losses narrowed significantly from -$52,356 in FY2024 to -$14,703 in FY2025 (a 71.9% improvement), indicating better cost management or higher gross margins as volume increased [F1]. Net income followed similar patterns, reflecting sustained developmental spending typical for an early-stage enterprise.

Cash flows reflect the same story: operating activities consumed cash continuously (-$52K in FY2024 to -$10K in FY2025) with no positive free cash flow generation evident. Stockholders’ equity deteriorated from -$36K down to about -$104K over four years, underscoring accumulated losses exceeding capital injections [F1].

Notably, the latest reported quarter ending January 31, 2026 displays zero revenue generation while continuing to incur net losses around $18K and operating cash outflows of roughly $20K during the nine months ended January 31, 2026—a sign of volatility or disruption possibly linked to operational transitions or market shifts [S2][F1].

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 26015 | -14703 | -10153 | -14703 | +5103.0% | +71.9% |

| 2024 | 500 | -52356 | -52356 | -52356 | -16.7% | -79.4% |

| 2023 | 600 | -29182 | -29182 | -9.3% | ||

| 2022 | 0 | -26690 | -26824 | -26690 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 14.2 |

| 2024 | 58.7 |

| 2023 | 79.2 |

| 2022 | 93.9 |

Source: SEC companyfacts cache [F1].

Note: Data drawn from SEC filed XBRL reports; CapEx and dividends data unavailable.

Milk_Shake Product Focus and Market Positioning

The company’s product strategy centers on Milk_Shake hair care lines that emphasize natural constituents such as milk proteins, yogurt proteins, and fruit extracts designed to both enhance hair aesthetics and health sustainably [S1][S22]. These formulations intentionally reduce harmful chemicals like sulfates and parabens while avoiding sodium chloride—with packaging designed for recyclability reflecting a commitment to environmental stewardship.

This kind of formulation aligns well with contemporary 'clean beauty' consumer trends demanding transparency and eco-friendly ingredients. However, formulating within these constraints introduces challenges including sourcing quality raw materials that meet efficacy without synthetic additives—a notable barrier for small players lacking R&D scale.

Orion Bliss does not manufacture directly but sources products through Red Hot Products Ltd as its exclusive distributor [S1]. This third-party relationship limits control over production quality improvements or formulation innovation that could otherwise foster proprietary competitive moats.

Market access currently leans heavily on online sales channels—a common go-to-market approach for emerging brands seeking broad reach at lower upfront costs [S22]. The company intends to broaden penetration via physical stands and standalone stores but this pivot will require substantial investment in retail infrastructure, inventory management capabilities, and a deeper brand marketing spend while navigating competitive shelving spaces dominated by entrenched incumbents.

Financial Health and Liquidity Constraints Amid Operational Losses

Financially Orion Bliss remains fragile. As of January 31, 2026 total assets were just over $36K largely comprising intangible assets like their mobile application ($45K gross value less accumulated amortization) plus minimal cash ($2.4K) [S2][F1]. Current liabilities stood at approximately $177K driven by accounts payable related-party advances ($58K), director loans ($68K), notes payable ($45.5K), plus accrued interest obligations ($5.7K), producing a dangerously low current ratio near 0.01 signaling immediate liquidity stress.

Operating expenses are dominated by professional fees rather than employee payroll due to the absence of any staff beyond executive directors—a cost-minimization tactic reflective of startup constraints but also limiting operational bandwidth [S2].

Repeated 'going concern' disclaimers across quarterly reports point clearly to management’s acknowledgement that continuation depends on new inflows of capital or revenue ramp-ups not yet materialized [S2]. The lack of bank credit facilities exacerbates reliance on informal financing such as director loans without formal agreements or secured lines.

Capital Raising Strategies and Risks of Dilution

Historically Orion Bliss has financed operations via private placements involving equity sales intertwined with convertible debt instruments providing flexible short-term funding while offering investors equity upside potential [S4][S5][S6]. Director loans supplement these capital sources but remain insufficient standing alone.

No definitive commitment exists at present regarding impending financing rounds though management anticipates future equity issuance to bolster runway [S2][S4][S21]. This introduces high dilution risk for existing shareholders especially against a backdrop of negative working capital where urgent funding is mandatory just for sustaining day-to-day operations.

Terms accompanying convertible notes may carry preferential rights over common stock further complicating shareholder equity position post-financing events. Absence of disclosed financing partners or syndicates leaves open whether the company can secure adequate funding on economically reasonable terms or must accept highly dilutive arrangements or less favorable covenants.

Operational Outlook: Opportunities and Constraints for Growth

Strategic ambitions include transitioning from primarily online sales into physical retail via dedicated stands and standalone stores aimed at creating experiential brand encounters—often key in personal care categories which benefit from tactile customer engagement [S1]. Alongside this shift come expectations of marketing expense escalations required for brand building in saturated hair care markets.

Incremental inventory purchases will strain working capital further as Orion Bliss steps up supply commitments needed for retail presence—underscoring reliance once again on timely capital raises. Bridging the gap between early traction online sales and meaningful retail penetration frequently demands operational competencies scarce within single-person management setups absent broader teams specialized in distribution logistics or category merchandising.

Additionally the company lacks disclosed proprietary formulations or patents meaning competitive differentiation rests primarily on branding narrative around natural ingredients rather than technological innovation—limiting defensive moats versus larger brands able to deploy robust R&D budgets.

Returns Metrics: ROE & Cash Flows Context

Based on available data from SEC filings via XBRL tags [F1], Orion Bliss posted an approximate return on equity (ROE) of +14.2% for FY2025 calculated as net income (-$14,703) divided by stockholders’ equity (-$103,896). While positive in ratio terms due to negative equity base (accumulated losses), this does not imply sustainable profitability but rather reflects accounting dynamics amid early-stage losses.

Operating cash flows remain negative consistently with no reported free cash flow generation or dividend payments throughout reported periods; data on share repurchases or buybacks is not available from provided tags nor mentioned explicitly in filings. Capital expenditures (CapEx) figures are also not disclosed within available data sets restricting assessment of investment intensity.

What Investors Should Monitor Next

Given scant concrete guidance provided by management beyond ongoing funding needs these elements become critical watchpoints:

- Capital Access: Whether Orion Bliss secures fresh equity/investor backing or convertible debt under acceptable terms within coming quarters;

- Revenue Trajectory: Signs revenue can return above zero levels post-January 2026 quarter represent key validation of either customer retention or effective expansion;

- Retail Rollout: Tangible progress establishing physical locations or partnerships demonstrating scalable go-to-market evolution;

- Cost Structure Development: Any shifts toward hiring beyond sole officer/director potentially enhancing operational capacity but increasing fixed costs;

- Balance Sheet Movements: Changes in liabilities or working capital ratios indicating improved liquidity vs further deterioration.

Forward-looking statements carry typical uncertainty caveats outlined by management highlighting inherent risks; readers should interpret future projections conservatively considering company stage and external market volatility.

Disclaimer: This analysis is based solely on information available as of February 18th, 2026 from public SEC filings and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments