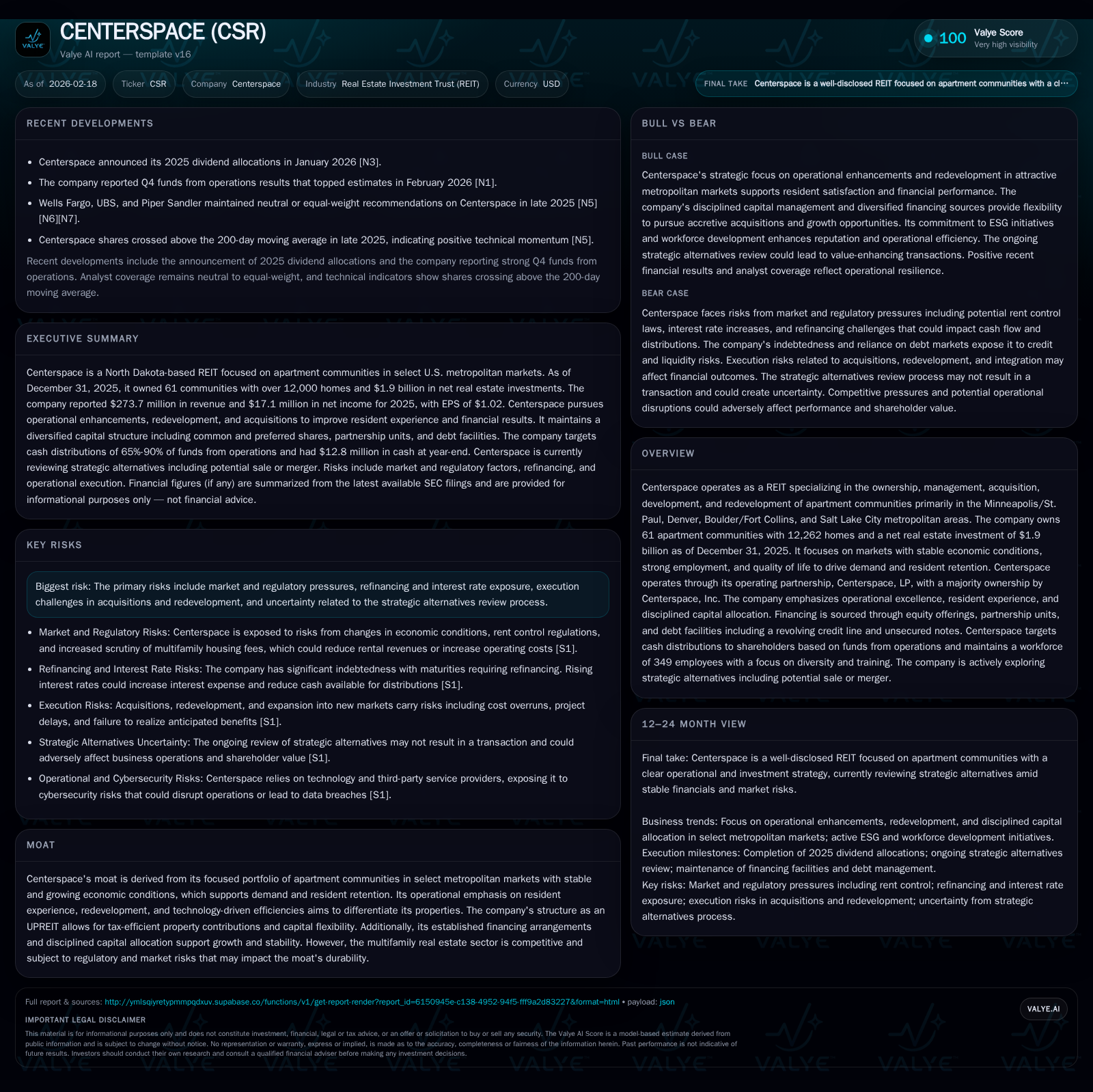

Centerspace’s Growth Plateau: Balancing Redevelopment and Strategic Alternatives Amid Market Risks

Centerspace leverages operational enhancements and focused market exposure to sustain growth while navigating strategic reviews and regulatory uncertainties.

Centerspace (CSR) operates a concentrated portfolio of 61 apartment communities primarily across the Midwest and Mountain West, driving steady revenue growth through operational refinements and redevelopment. Despite a strong rebound in operating income and net income in 2025 following a volatile prior year, the company faces pressures from rising interest rates, potential rent control regulations, and ongoing strategic alternatives review. Capital allocation prioritizes shareholder distributions supported by robust cash flows, though returns on equity remain subdued. Monitoring refinancing outcomes, execution on redevelopment projects, and regulatory developments will be key to understanding Centerspace’s future trajectory.

Company Overview

Centerspace (ticker CSR) is a real estate investment trust specializing exclusively in multifamily apartment communities within selected U.S. metropolitan markets noted for economic stability and employment growth — specifically the Minneapolis/St. Paul, Denver, Boulder/Fort Collins, and Salt Lake City regions.[S1][S15] As of December 31, 2025, the company owned 61 communities comprising over 12,000 homes with a net real estate investment base of approximately $1.9 billion.[S1] Operating as an UPREIT since 1997 enhances tax efficiency for contributors of property.[S28]

Their operating philosophy emphasizes delivering exceptional resident experiences via operational excellence while driving asset value through redevelopment tailored to evolving market demands.[S6] These efforts are complemented by leveraging technology initiatives including selective adoption of AI for internal workflow improvements albeit with acknowledged execution risks.[S14][S16]

Historical Financial Performance

Centerspace’s revenue demonstrated moderate expansion over recent years, growing consistently from $256.7 million in FY2022 to nearly $274 million in FY2025 — a compound annual growth rate just under 3%. Revenue increased by about 4.9% from $261 million in FY2024 to $274 million in FY2025.[F1]

Operating income experienced considerable volatility: after increasing sharply to $84.5 million in FY2023 from just $13.9 million in FY2022, it dipped significantly back down to about $20.5 million in FY2024 before rebounding strongly to $64.5 million in FY2025.[F1] This swing reflects cyclical operational factors including leasing renewals and rental pricing dynamics influenced by market conditions.

Net income mirrored this pattern — losses were recorded in both FY2022 (-$14.1 million) and FY2024 (-$11.3 million), interrupted by positive earnings of $41.3 million in FY2023 before settling at a positive but subdued $17.1 million in FY2025.[F1]

Operating cash flow has been more stable relative to earnings fluctuations, remaining near the high-$90 millions per annum range over the four-year span.[F1] Notably, capital expenditures reported were minimal or zero since FY2023 reflecting limited acquisition activity alongside ongoing redevelopment funded from operations.[F1]

The company’s equity base slightly fluctuated but remained approximately between $650 million to $720 million during this period.[F1]

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 274 | 17 | 98 | 65 | +4.9% | +251.0% |

| 2024 | 261 | -11 | 98 | 20 | -0.1% | -127.4% |

| 2023 | 261 | 41 | 90 | 84 | +1.8% | +392.9% |

| 2022 | 257 | -14 | 92 | 14 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 51 | 3 | |

| 2024 | 46 | 5 | |

| 2023 | 44 | 12 | 90 |

| 2022 | 44 | 29 | 92 |

Source: SEC companyfacts cache [F1].

Note: Capex omitted for years with insufficient data; YoY for Net Income omitted where calculation not applicable due to sign changes.

Growth Prospects

Centerspace’s growth strategy leans on several pillars:[S6][S28]

- Operational Enhancements: Ongoing focus on elevating resident experience via service quality improvements aims to improve retention rates.

- Redevelopment Projects: Strategic repositioning and upgrades of existing assets aim to capture rental premiums aligned with current market expectations.

- Targeted Acquisitions: While capital deployment into new properties has slowed recently (evidenced by low capex), the company signals continued interest within its established geographic footprint where economic indicators remain favorable.[S15]

- Technology Adoption: Leveraging AI internally may unlock cost efficiencies; however, execution risks including data limitations temper expectations.[S14]

However, these opportunities coexist with headwinds that could constrain growth:[S26][S11]

- Regulatory Environment: The possibility of rent control regulation or restrictions on fee structures introduces revenue uncertainty.

- Market Competition: The multifamily sector is competitive; changing tenant preferences or oversupply could pressure occupancy or rents.

- Interest Rate Sensitivity: Rising rates increase financing costs and may dampen property valuations.

- Strategic Alternatives Uncertainty: The ongoing strategic alternatives review injects uncertainty around future ownership or capital allocation priorities.[N1][S26]

Forecasts and Milestones

The company has not issued explicit forward guidance but highlights key milestones:[N1][N3][S6]

- Monitoring progress on redevelopment projects across core markets.

- Executing its distribution policy targeting approximately two-thirds to nine-tenths payout of funds from operations.

- Continuing capital structure optimization via refinancing efforts including utilization of expanded unsecured credit lines and mortgage facilities priced favorably under historical averages (~2.78% fixed).

- Completion of strategic alternatives review remains open-ended; no transaction commitments announced as of early 2026.[S26]

Important metrics to watch include occupancy rates post-redevelopment campaigns, leverage ratios relative to covenant thresholds (total debt/asset ratio was ~42% at end-2025), refinancing costs amid shifting interest rates, and regulatory developments on rent pricing frameworks.[S9][S13][S26]

Capital Allocation and Returns

Centerspace maintains a disciplined capital allocation framework prioritizing stable dividends balanced against reinvestment needs:[S12][F1]

- Dividend Distributions: Approximately $51 million paid out on common shares in FY2025 representing around two-thirds of funds from operations — consistent with prior years.

- Buybacks: Modest share repurchases occurred totaling roughly $3.45 million in FY2025 down from prior periods.

- Capital Investments: Limited acquisition activity recently shown by minimal capex spending; emphasis placed on internal redevelopment funded largely through cash flow rather than external capital raises.

Return metrics suggest subdued profitability relative to equity: calculated ROE based on net income ($17m) over equity ($719m) approximates a low double-digit percentage (2–3%), indicative of REIT characteristics with substantial non-cash depreciation expense components impacting GAAP earnings cognition.[F1]

Liquidity is supported by multiple debt facilities:

- Unsecured revolving credit facility expanded via accordion feature enabling up to $400 million borrowing capacity priced at ~SOFR + margin (approximate all-in rate ~5%).[S7]

- Mortgage debt secured by selected properties bearing fixed rates averaging near ~2.78% maturity extending up to mid-century dates providing duration softness against refinancing risk.[S4][S9]

- Private notes aggregating approximately $300 million across staggered maturities also diversify funding sources.[S4]

The balance sheet leverage stood at about 42% total indebtedness relative to assets supporting financial flexibility within typical REIT parameters but subject to compliance with covenants related to coverage ratios and secured debt limits.[S9][S19]

Industry Context & Sector Nuance (Analysis)

Multifamily REITs like Centerspace operate in an environment characterized by:

- Increasing building amenities expectations including energy-efficient systems impacting PUE-equivalent measures for residential buildings.

- Short-term leasing arrangements driving more frequent rent resets but also exposing revenue streams more rapidly to local economic shifts.

- Regulatory pressures mounting nationally around tenant protections including rent stabilization attempts which could compress achievable rents per unit.

- Rising cost environment given wage inflation among property management personnel contributing directly to margins. This complex backdrop necessitates nimble operational responses paired with conservative leverage management uncommon in earlier REIT eras when fixed-rate long-term mortgage debt was dominant.

Risks

Centerspace’s filings emphasize several material risk domains worth consideration:[S11][S26][S16]:

- Strategic Alternatives Process Risks: No assurance exists that strategic review will yield any beneficial transaction; potentially costly distractions or disruptions may ensue.

- Refinancing & Interest Rate Exposure: Substantial debt maturities require successful refinancing amid potentially tighter credit markets increasing cost.

- Regulatory Risks: Rent control or tenant protection laws could materially reduce revenue growth or operating flexibility; rent-related legal actions akin to those faced by industry giants pose reputational hazards even though Centerspace is not currently involved.

- Execution Risk on Redevelopment & Expansion: Delays or cost overruns could impair returns expected from repositioning their portfolio.

- Cybersecurity Threats: Previous ransomware episodes illustrate ongoing vulnerability despite no material impacts reported; increased cybersecurity budgets may pressure operating expenses further.

- Environmental Liability Risks: Potential unforeseen remediation costs tied to legacy property contamination possible though currently unmaterially identified. All such factors contribute potential volatility beyond fundamental operational performance.

Conclusion & What To Watch (Analysis)

Over the next quarters investors should closely observe:

- Updates on the strategic alternatives review process outcomes including potential M&A activity or independent strategy reaffirmation announcements;

- Performance metrics related to redeveloped properties including occupancy trends, rental rate increases or concessions granted;

- Refinancing terms for upcoming debt maturities especially any deviation from historically low fixed-rate notes;

- Regulatory developments at municipal/state levels affecting multifamily housing pricing models; and broader macroeconomic indicators influencing job stability within their key regional markets which underpin renter demand. While Centerspace exhibits improved financial results accompanied by structural strengths like geographic concentration in resilient metro areas and disciplined balance sheet management,[F1][S15] notable uncertainties remain that bear watching closely given their potential impact on future performance trajectories beyond current steady-state operations.

Disclaimer: This analysis is provided for informational purposes only without any recommendation regarding the buying or selling of security or stocks referenced herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments