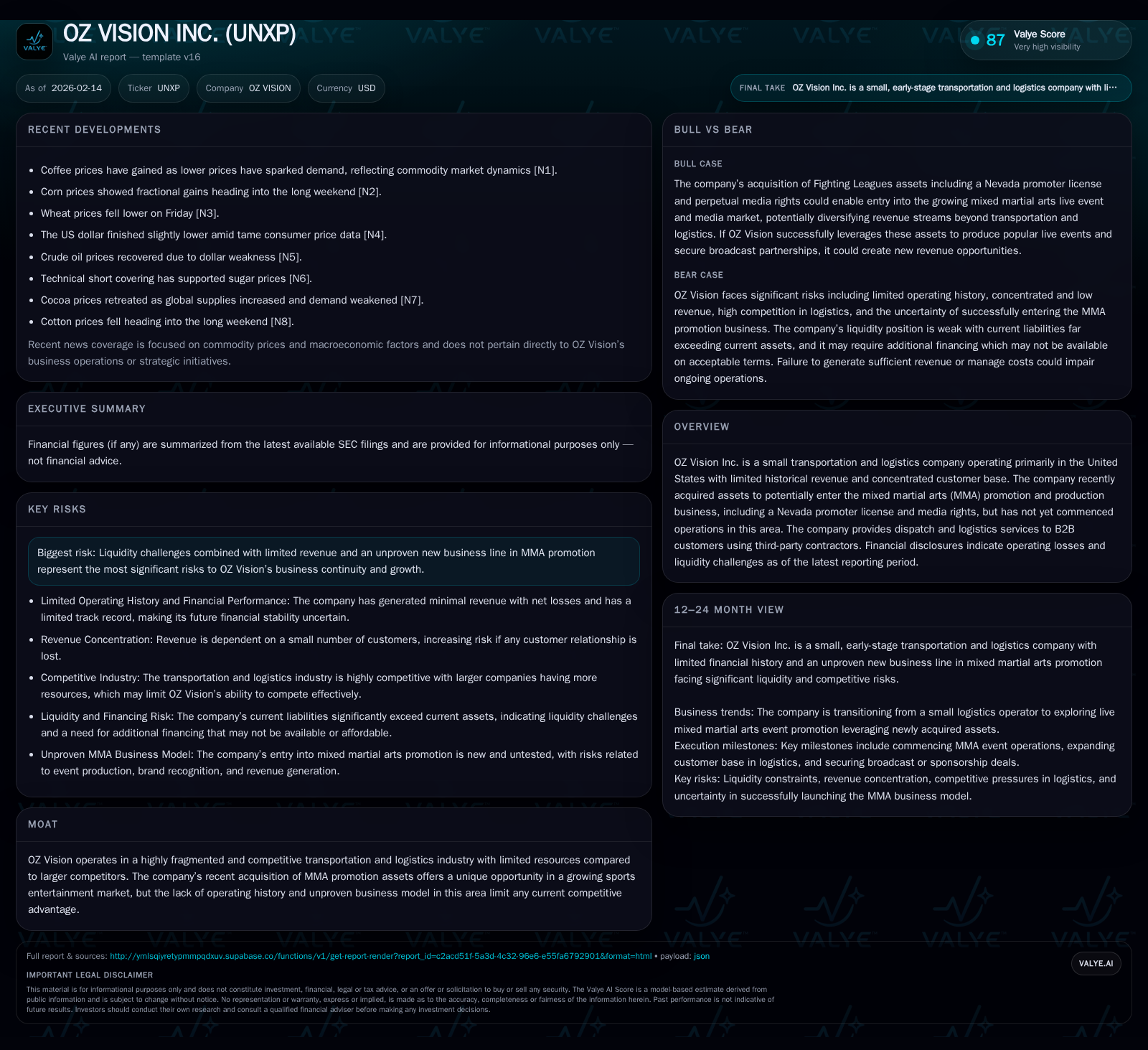

OZ Vision Inc.'s Bold Shift from Struggling Logistics to MMA Ambitions Amid Cash Crunch

Exploring how OZ Vision's pivot to sports entertainment clashes with its precarious financial footing in a cutthroat logistics landscape.

OZ Vision Inc. operates a tiny logistics business marked by minimal revenue and deep operating losses, while recently acquiring substantial mixed martial arts (MMA) assets offering high-growth potential. The company’s dual identity—fragile freight dispatcher and hopeful combat sports promoter—frames a tale of both strategic aspiration and existential risk. Severe liquidity shortages, customer concentration, and unproven MMA operations highlight formidable challenges ahead. The path forward depends largely on successful capital raising and the ability to turn latent MMA rights into real revenue streams.

A Dual-Identity Business: From Logistics to Combat Sports

OZ Vision Inc. stands at a crossroads, operating an essentially embryonic transportation and logistics business while freshly stepping into the provocative arena of mixed martial arts (MMA) promotion. Historically, OZ Vision—formerly United Express Inc.—delivers merchandise primarily as a dispatch service using third-party contractors rather than owning vehicles [S1]. Revenues have been painfully modest: just over $54,000 annually for fiscal 2025, driven by fewer than five customers, reflecting precarious revenue concentration and limited market penetration [S1][F1].

Against this backdrop of constrained logistics activity, the company’s September 2023 acquisition of Fighting Leagues LV assets marks a dramatic strategic pivot. These assets encompass a Nevada State Athletic Commission Professional Promoter license, granting rights to produce live Kickboxing, Boxing, and MMA shows in Nevada; perpetual worldwide broadcast TV rights for forty historic events; and production-stage equipment [S1]. However, as of early 2026, OZ Vision has yet to generate revenues or launch operations leveraging these MMA licenses and tangible assets [S1]. This stark juxtaposition crafts a dual-identity corporate narrative: a struggling freight dispatcher alongside a nascent combat sports promoter waiting in the wings.

Financial Fragility: Navigating Revenues, Losses, and Liquidity Woes

The small-scale logistics enterprise generates insufficient revenues to cover operating costs. For the twelve months ending June 30, 2025, OZ Vision reported $54,232 in revenue but incurred costs of goods sold slightly exceeding this figure ($54,692), resulting in a gross loss [S1]. Operating expenses outpaced revenues further at $65,141, culminating in a net loss exceeding $65,600 for that year [S1]. The more recent half-year through December 31, 2025 reveals continued erosion: revenues plunged to approximately $2,100 with a net loss near $37,266 during that six-month interval [F1].

Cash reserves provide scant buffer; as of December 31, 2025, cash and equivalents totaled roughly $3,442 against current liabilities surpassing $1.17 million—a current ratio effectively zero [F1]. Such severe working capital imbalance exposes OZ Vision to imminent solvency risk without immediate capital inflow. Prior filings explicitly warn shareholders about "high degree of risk," emphasizing potential inability to sustain operations absent successful fundraisings [S1]. CFO discussions reveal intent to seek additional equity offerings though acknowledge these may fail or impose dilutive terms unfavorable to existing investors [S1].

Together these data paint bleak short-term financial health marked by near-zero operating margins and terminal liquidity stress.

An Industry Jigsaw: Positioning OZ Vision in Fragmented Transportation

The US transportation and logistics industry is notably fragmented—with three broad segments: private fleets operated by shippers themselves; truckload carriers moving full shipments; and less-than-load providers consolidating multiple smaller shipments [S1]. OZ Vision occupies the latter niche through third-party contractor dispatch but lacks owned fleet capacity or scale economies common among larger competitors. This dependence limits pricing control and operational flexibility.

Competitors typically have deeper financial war chests enabling brand building and fleet investment. As described in regulatory disclosures, "many competitors have significantly greater financial... marketing... resources" potentially overshadowing OZ Vision's offerings [S1]. Fuel fluctuations plus driver compensation unpredictabilities compound cost challenges for small operators who must keep prices competitive yet sustainable—a delicate balance OZ Vision acknowledges carries risk of customer attrition [S1].

In essence, the company faces an uphill battle for share gain amid entrenched rivals benefiting from size advantages within a highly competitive industry.

The MMA Gambit: Asset Acquisition and Untapped Potential

The purchase of Fighting Leagues LV assets represents a bold foray outside OZ Vision's core competencies. The professional promoter license issued by Nevada regulators uniquely authorizes production of live MMA-related events in this key jurisdiction—one synonymous with combat sports prominence [S1]. Alongside media rights covering forty prior shows indefinitely worldwide via broadcast TV channels plus ownership of production equipment assets, OZ Vision arguably secured an intellectual property stronghold enabling multimedia event development.

Yet this gambit remains speculative. To date there are no recorded operational activities utilizing these licenses or assets [S1]. No fights staged nor broadcast agreements activated suggest that management is at an early exploration phase rather than executing full-scale operations.

From an industry perspective (analysis), mixed martial arts continues growing globally as audiences enlarge across digital platforms while lucrative sponsorship deals amplify revenue pools. Successful promotion can deliver multiples higher margin streams than traditional logistics fees but demand considerable upfront investment in talent acquisition, marketing budgets, regulatory compliance costs, venue contracts, and media partnerships (analysis).

In sum, the MMA gambit offers a tantalizing avenue for future growth but carries heightened executional risk given absent track record.

Risks and Rewards: Evaluating the Company's Viability and Growth Prospects

The company's disclosures explicitly spotlight several intertwined risks—liquidity crunches requiring urgent financing; unstable customer base underpinning fragile revenues; intense competition compressing margins; plus unproven new business lines bearing uncertain scalability [S1][valye_report_excerpt].

On the flip side lies the proposed upside if management successfully deploys its MMA arsenal. Connecting with major television broadcasters or entertainment enterprises could multiply income sources well beyond limited logistics fees—generating higher operating leverage once events achieve market traction [S1]. Strategic alliances might unlock promotional expertise otherwise missing internally.

Nevertheless, timing is critical; delayed capital raises could stymy fight card launches while continued drain from logistics cash flows depletes reserves further. Early-stage volatility is unavoidable given transition complexity compounded by resource scarcity—a gamble poised between phoenix-like reinvention versus protracted operational stagnation.

Competitive Landscape: Limitations vs. Established Giants

Within both divisions—the legacy freight dispatch business and emerging combat sports venture—OZ Vision confronts asymmetric competition hurdles. Its size disadvantage manifests sharply against large national carriers commanding expansive vehicle fleets providing optimized routing capabilities plus established client relationships [S1]. These entrenched firms can undercut prices strategically if pressured while sustaining profitability through scale efficiencies.

Similarly in the sports realm (analysis), heavyweight promotion companies benefit from robust brands recognized worldwide plus deep connections within athlete networks and media conglomerates difficult for newcomers to replicate swiftly. Brand recognition affects ticket sales drive participation interest impacting long-term event economics profoundly.

For OZ Vision therefore maintaining customers requires relentless price vigilance alongside measurable service differentiators within freight operations while concurrently navigating dicey brand-building efforts from ground zero in MMA promotion.

The Road Ahead: Strategic Imperatives and Scenarios

Looking forward entails navigating daunting opacity around capital access coupled with rapidly shrinking liquidity buffers. Should OZ Vision raise fresh equity or forge alliance agreements expeditiously—particularly ones activating the Fighting Leagues assets—it may catalyze transformation into a hybrid enterprise blending sports entertainment with freight logistics services.

Absent such success scenarios shrink toward either forced downscaling of logistics activities or restructuring moves including asset sales or mergers aimed at survival. Diversifying the customer base within transportation while ramping event production capabilities stand as dual imperatives intertwined with financing milestones.

Continued regulatory filings must be monitored closely for guidance on financing outcomes plus initial MMA event deployment progress which will elucidate whether this high-risk pivot merits optimism or cautionary stance going forward.

This analysis synthesizes publicly filed SEC documents together with company disclosures as of early 2026 without speculative projections beyond sourced facts. Readers should consider inherent volatility typical among emerging growth companies undertaking strategic transformations under challenging financial circumstances.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments