United Rentals Drives Growth Through Operational Efficiency and Scale Advantage

Latest quarterly results reveal United Rentals’ effective use of scale and operational initiatives to drive momentum despite cyclical headwinds.

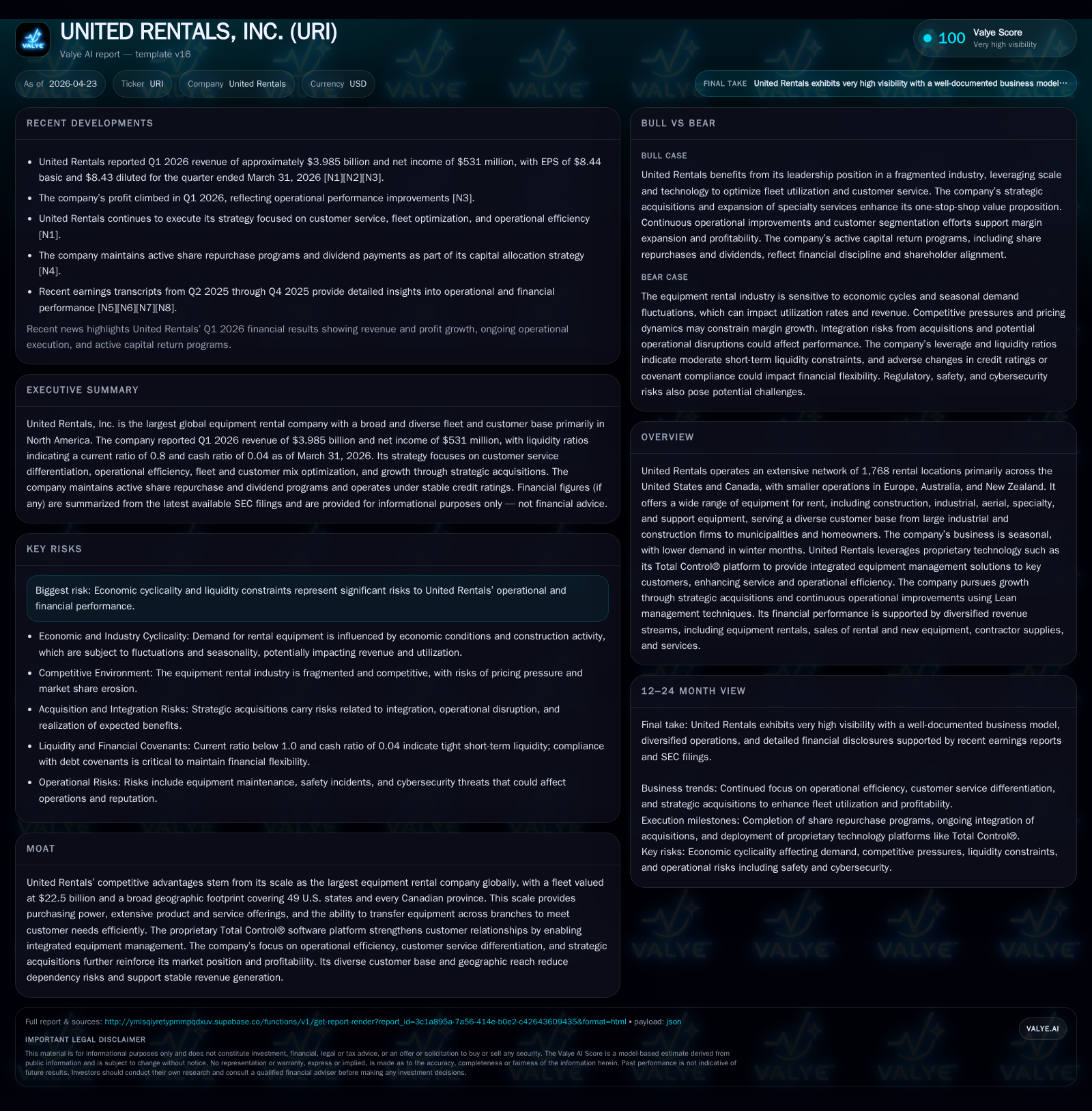

United Rentals reported better-than-expected Q1 2026 revenue growth supported by strong fleet utilization and disciplined rate management, signaling operational resilience early in the year’s seasonally slower quarter. The company leverages a multi-faceted business model anchored by a vast $22.5 billion fleet and North American branch network, combined with proprietary Total Control® software and adjacent specialty services that deepen customer engagement. Its scale advantage delivers purchasing power, service consistency, and optimization flexibility, setting it apart in a fragmented equipment rental market. Growth is driven by technology-enabled service differentiation, targeted customer segmentation, and specialty acquisitions, while macroeconomic cyclicality and stringent debt covenants weigh on liquidity and capital flexibility. Financials validate strategic execution with steady operating income and robust cash flows, underpinning growth investments and shareholder returns.

Q1 2026 Operating Highlights Illuminate Momentum

United Rentals’ latest quarterly filing (10-Q dated April 22, 2026) reveals that the company navigated seasonally lower winter demand to deliver a revenue performance that beat consensus expectations [S2][N2][N12]. This early-year strength is notable given the inherent cyclicality in equipment rentals tied to construction and industrial activity. The company reports continued solid fleet utilization rates alongside effective rate management which helped maintain operating income stability despite typical Q1 softness. The proprietary digital platform Total Control® has been instrumental in enabling streamlined customer interactions and integrated equipment management during this period, reinforcing operational efficiency.

Management commentary highlights ongoing Lean management deployment to accelerate equipment turnaround times and enhance delivery logistics – crucial in balancing fleet availability against fluctuating rental demand. While no major guidance shifts were disclosed, the results affirm momentum entering the traditionally stronger second half of the fiscal year [S2][N1]. These outcomes support confidence that United Rentals’ operational discipline remains intact amid broader economic headwinds.

United Rentals’ Multi-Pronged Business Model: Rental Scale Meets Service Differentiation

At its core, United Rentals operates the largest global equipment rental fleet valued at approximately $22.5 billion Original Equipment Cost (OEC), spread across an extensive branch network of 1,768 locations primarily throughout the United States and Canada serving nearly every major metropolitan area [S1][F1]. This geographic breadth ensures proximity to customers spanning large industrial firms, municipalities, construction companies, utilities, manufacturers, homeowners, and government entities.

The company’s revenues dominantly stem from equipment rentals (~86% in 2025), supplemented by sales of rental equipment, new equipment sales, contractor supplies, service revenues, and ancillary offerings which diversify income streams [S1]. Key to maintaining competitive differentiation is United Rentals’ proprietary Total Control® platform—a unique software application providing large customers with unified visibility into their equipment usage across locations. This integration facilitates not just convenience but also deeper account penetration through cross-selling opportunities across geographies.

Lean enterprise principles underpin continuous improvement efforts focused on cycle time reductions for prepping rental units, efficient scheduling of logistical operations (deliveries/pickups), maintenance workflow enhancements, and customer service best practice adherence [S1]. These kaizen initiatives enable not only cost containment but also enhanced asset utilization critical to sustaining return on invested capital.

The company further complements its core offering through strategic expansion into adjacent specialty services—such as trench safety products—and mobile storage solutions bolstered by acquisitions like Yak Access in March 2024 [S1]. These services offer differentiated jobsite solutions attractive to infrastructure-focused clients where bundled offerings increase customer stickiness.

Industry Landscape: Fragmented Market Reconciled by Scale Leadership

The broader North American equipment rental industry remains highly fragmented with many smaller regional providers coexisting alongside large national players [S6][S10]. In this environment, United Rentals' commanding scale confers distinct competitive advantages: substantial purchasing leverage reduces acquisition costs for fleet assets; extensive geographic presence facilitates intra-branch equipment repositioning optimizing asset turns; standardized maintenance protocols improve reliability—a key driver of customer preference; and broad product/service selection addresses complex client needs from one-stop solutions.

Scale also provides insulation against some typical market risks such as regional construction downturns by virtue of portfolio diversification across end markets (residential/commercial/infrastructure) and geography [S24][S26]. Regulatory factors affecting operations remain stable but compliance with safety programs forms part of risk mitigation strategy given asset-intensive nature.

Smaller competitors face challenges replicating United Rentals’ blend of technological integration (Total Control®), operational refinement (Lean processes), and financial firepower to sustain innovation or pursue sizable acquisitions. Industry barriers thus include capital intensity of fleets (multi-billion-dollar investments) plus expertise embedded in fleet management technologies.

Growth Drivers: Technology, Customer Segmentation, and Specialty Services Expansion

United Rentals drives growth through multiple synergistic channels anchored by technological advancement. Adoption of Total Control® continues expanding among top-tier accounts enhancing integrated fleet visibility that translates into higher retention rates and incremental share-of-wallet gains [S1]. This SaaS-enabled platform supports digitized transaction workflows including contactless rentals—a growing customer preference post-pandemic.

Customer mix optimization focuses on increasing exposure to high-return segments such as large industrial projects while managing cyclical local contractor exposures [S1]. Equally important is tailoring fleet composition responsive to demand trends among specialized sectors like infrastructure where demand for trench safety products or HVAC equipment rises alongside public spending initiatives.

Strategic bolt-on acquisitions have supplemented internal growth with complementary capabilities—Yak Access acquisition exemplifies targeted entry into surface protection mats space adding a previously untapped revenue stream [S1][N2]. Ongoing Lean process improvements bolster margin expansion potential by systematically removing operational waste thereby elevating profitability leverage as revenues grow.

Seasonality imposes a predictable constraint with Q1 being soft; however, secular demand drivers such as increasing infrastructure investment plans in North America provide structural tailwinds offsetting shorter-term volatility [S1].

Challenges Ahead: Economic Cyclicality and Liquidity Dynamics

Despite operational strengths, United Rentals' performance remains sensitive to capital expenditure cycles within construction and industrial sectors [S1][S2]. Economic downturns reduce asset utilization rates leading to margin compression due to fixed cost absorption challenges.

Liquidity considerations are paramount given the company's sizeable debt profile totaling over $14 billion with multiple instruments including revolving ABL facilities ($4.5 billion), term loans ($1 billion), senior notes maturing across 2027–2034 horizon [F1]. Credit agreement covenants currently include a fixed charge coverage ratio applicable only under stressed borrowing availability conditions—currently inactive—but impose restrictions around incurring additional indebtedness or making dividends/share repurchases beyond thresholds [S7][S13][S27].

Refinancing risks exist as maturities approach though existing negotiating positions allow staggered amortization schedules mitigating lumpiness risk. The company carefully monitors covenant compliance with available liquidity buffers evidenced by ~$156 million cash on hand as of March 31, 2026 against ~$4.13 billion current liabilities yielding a current ratio below unity implying working capital pressures yet manageable due to access to secured asset-based lending facilities [F1].

Subdued credit ratings at Ba1/BB+ level underscore caution among rating agencies though outlooks remain stable currently [S14]. The ability to deploy capital flexibly will remain hingeing on navigating cyclical downturns without covenant breach events.

Financial Analysis: Metrics Validate Strategic Execution

United Rentals’ financial performance over recent years supports its growth narrative through steady top-line expansion coupled with disciplined margin management generating robust cash flow conversion into free cash flow for reinvestment:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 4.2 | 653 | 5.2 | 1052 | +2.8% | -5.2% |

| 2024 | 4.1 | 689 | 4.5 | 1087 | +9.8% | +1.5% |

| 2023 | 3.7 | 679 | 4.7 | 1063 | +13.1% | +6.3% |

| 2022 | 3.3 | 639 | 4.4 | 1024 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 464 | 1969 | 7.3 |

| 2024 | 434 | 1571 | 8.0 |

| 2023 | 406 | 1070 | 8.4 |

| 2022 | 1068 | 9.0 |

Source: SEC companyfacts cache [F1].

Data sourced from recent SEC filings representing annual results through FY2025; Capex details limited historically but show disciplined reinvestment trends aligned with Lean optimizations ([F1]).

Operating income declined slightly year-over-year amid inflationary pressures offset partially by rate increases reflecting judicious price setting ability supported by scale advantages detailed earlier. Strong operating cash generation drove free cash flow approximating $5 billion due to controlled capital spending that enables ongoing fleet modernization without over-extension.

Capital allocation remains shareholder-friendly with dividends showing consistent increases since program inception in early 2023 alongside substantial share repurchase activity accelerating into early 2026 following completion of prior $2 billion authorization programs [S11][F1]. Such balance reflects healthy confidence in underlying business fundamentals grounded in operational excellence.

This analysis synthesizes the most current public disclosures from United Rentals through April 22, 2026 filings combined with secondary market commentary to present an integrated view of how scale advantages paired with technological innovation fuel sustained growth amidst cyclical volatility inherent in the heavy equipment rental industry sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments