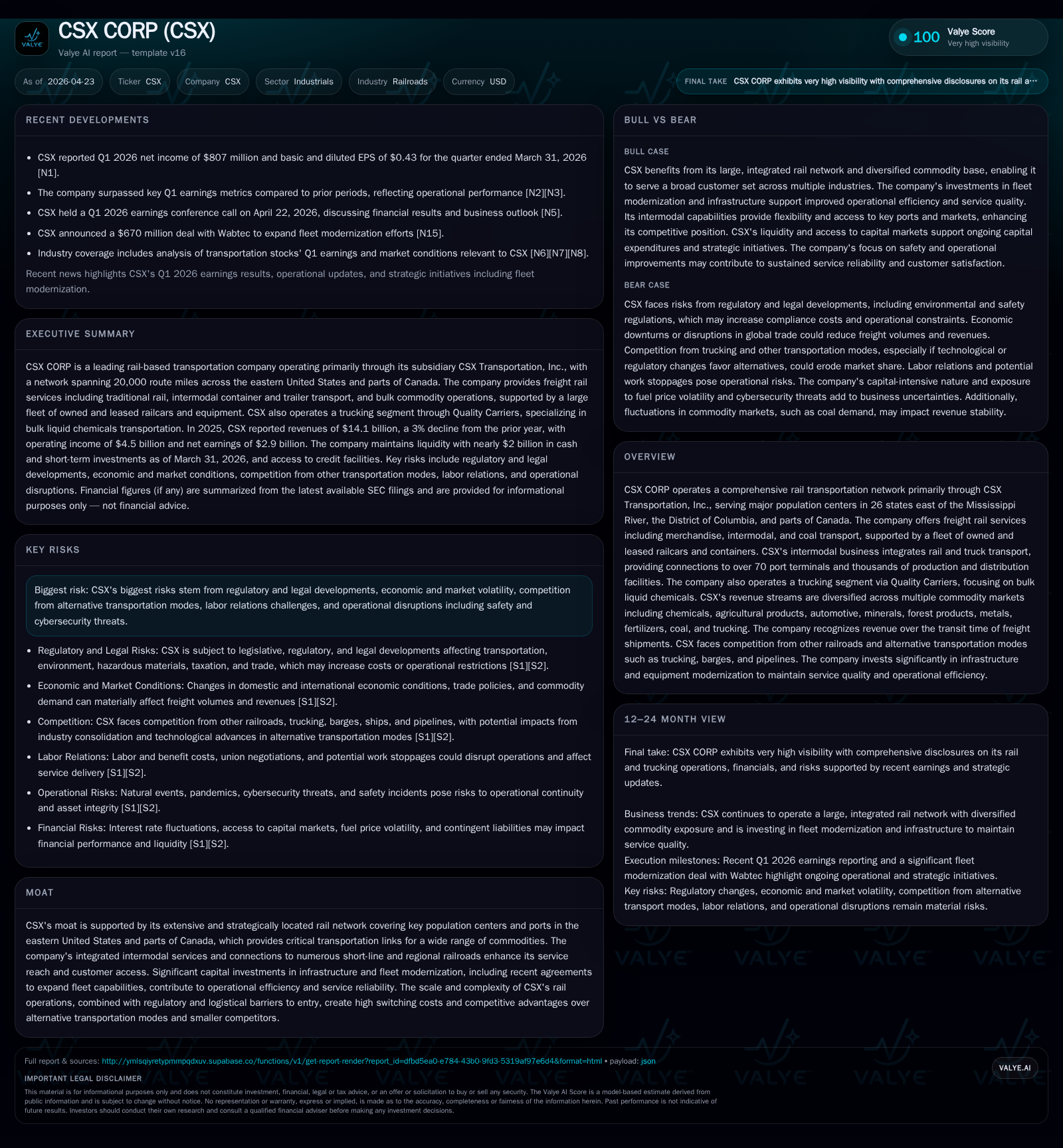

CSX CORP Strengthens Core Rail Operations Amid Evolving Market Dynamics

CSX's Q1 2026 results reflect resilience in freight volumes and strategic investments while managing cost pressures and regulatory risks.

In Q1 2026, CSX CORP delivered solid operational performance with modest volume growth in key segments and proactive cost management despite inflationary headwinds, according to its latest 10-Q. The company’s integrated rail and intermodal business remains well-positioned, leveraging a broad eastern U.S. network and fleet upgrades to sustain competitive differentiation. Key challenges include navigating rising regulatory compliance costs, labor dynamics, and safety mandates. Continued capital expenditure on infrastructure and fleet modernization underpins growth potential alongside trucking operations integration.

Q1 2026 Operational Update: Results and Implications

CSX's first quarter of 2026 showcased a resilient operating profile during continuing inflationary pressures and regulatory cost challenges. As detailed in the April 22, 2026 Form 10-Q [S2], CSX reported stronger-than-expected earnings driven primarily by a 4% increase in intermodal volumes compared to the prior year quarter. Intermodal revenue rose modestly despite a slight decline in revenue per unit. Merchandise volumes saw a marginal contraction of 2%, reflecting mixed economic factors across commodity sectors [N1][N3]. The company effectively managed expenses amidst rising fuel prices and wage inflation through disciplined cost controls.

Operational KPIs showed velocity improvements of approximately 1% year-over-year with stable dwell times indicating steady network fluidity. Carload trip plan adherence decreased slightly by 1%, offset by steady intermodal trip plan metrics. These signals suggest improving service reliability which is critical for customer retention during competition [S2]. Concurrently, safety metrics expanded positively with a significant improvement in personal injury frequency indices and reduced train accident rates over the prior year period [S18].

The recent news reports confirmed that CSX surpassed Wall Street earnings forecasts for this quarter [N3], highlighting effective execution of operational initiatives including productivity improvements tied to integrated intermodal offerings.

Business Model Blueprint: Integrated Rail and Intermodal Services

CSX operates primarily through its subsidiary CSX Transportation Inc., providing rail freight services across approximately 20,000 route miles in the eastern U.S., reaching key population centers covering 26 states east of the Mississippi River plus parts of Canada [S1][S9]. Its core revenue streams are divided among merchandise freight (chemicals, metals, agricultural goods), intermodal container/trailer transport connecting rail with truck operations at more than 70 port terminals, coal shipments, and trucking services via Quality Carriers specializing in bulk liquid chemicals.

This multi-modal approach allows CSX to generate revenues under contracts that encompass full supply chain solutions linking rail-to-truck transitions efficiently. Fleet ownership combined with leased rolling stock ensures capacity flexibility vital for meeting seasonal demand variances [S9]. The integration of complimentary trucking capabilities enhances last-mile delivery options, bolstering CSX's value proposition over pure rail providers.

Service reliability—linked to infrastructure robustness—and comprehensive terminal networks remain critical for customer retention against alternative freight modes such as long-haul trucking. This model delivers scalable offerings across diversified commodities mitigating concentration risks inherent to any single sector [S9][S15].

Competitive Moat and Industry Positioning in Eastern US Freight Rail

CSX holds one of the largest Class I rail footprints focused on the eastern U.S., servicing major corridors such as I-90 connecting Midwest to Northeast ports and I-95 along the eastern seaboard [S12]. These routes benefit from favorable engineering attributes like double track segments facilitating enhanced velocity and handling of high-speed intermodal traffic.

The company's moat derives from vast asset bases—rail lines requiring significant capital to build or upgrade—and regulatory constraints that limit viable new entrants. Switching costs arise from integrated logistics solutions blending rail connectivity with trucking access to thousands of production/distribution points and hundreds of short-line rail connections [S26].

Regulatory mandates including the common carrier obligation for hazardous materials transportation further entrench incumbents due to compliance complexities. However, competition persists chiefly from trucking which benefits from infrastructural public roadways but faces increasing size/weight regulations that may shift freight mix dynamics [S26].

Technological risk is notable; dependence on advanced IT systems for safe operations introduces cybersecurity vulnerabilities obliging continuous investment in security controls [S19]. Overall, CSX maintains scale advantages and regulatory barriers that underpin strong competitive positioning within its regional domain.

Growth Vectors: Infrastructure Investment, Fleet Expansion, and Intermodal Connectivity

CSX's capital spending remains substantial—a $2.9 billion outlay on property additions noted in FY2025 filings—with heavy emphasis on track replacement projects encompassing labor-intensive self-construction processes such as rail welding, ballast laying, tie replacement, gauging standardization etc. [S11]. These efforts aim to enhance network capacity, operational safety, velocity improvements and service reliability over time.

Fleet expansion encompasses not just locomotives but also freight cars supporting diversified product flows particularly intermodal containers/trailers aligned with port activities serving global trade lanes [S11][S2]. The company’s investments extend to technology upgrades facilitating better shipment tracking and network optimization.

Additionally, Quality Carriers integration presents synergy opportunities by expanding bulk liquid chemical logistics beyond rail into dedicated ground transportation enhancing end-to-end service coherence [S9][S2].

Capital allocation balances aggressive infrastructure investment with shareholder cash returns evidenced by continued dividends (recent increases maintaining a consecutive annual growth streak) coupled with robust share repurchases albeit moderated compared to previous years amid market conditions [S5][F1][S14].

Challenges Ahead: Regulatory Landscape, Cost Pressures, and Labor Dynamics

CSX operates under complex regulatory oversight involving STB, FRA, PHMSA among others impacting hazardous materials transport rules enforcing strict safety/security standards with significant noncompliance penalties [S1][S19]. Emerging legislation or executive actions could impose tightened price controls or restrict route access impacting operational flexibility.

Legal exposures remain material relating to ongoing litigation around fuel surcharge practices besides environmental remediation liabilities which could incur unpredictable financial impacts despite existing reserves [S6][S19]. Cybersecurity threats target both internal IT systems critical for train control/safety and third-party vendors adding operational risk dimensions [S19].

Labor relations represent another pivotal constraint; over three-quarters of CSX’s unionized workforce is covered by national agreements though some negotiations remain unsettled introducing uncertainty around wage/cost structures alongside potential disruption risks [S4][N3]. Employee retention amid competitive labor markets also poses longer-term human capital challenges.

Cost pressures stemming from elevated fuel prices directly affect operating expenses even as efficiency initiatives moderate inflation pass-through effects partially [S15][N3]. Rising environmental compliance demands coupled with safety investment needs further amplify overall cost burdens necessitating careful balancing against revenue growth levers.

Key Milestones and Indicators to Monitor in Coming Quarters

Market observers should focus on sequential trends in volume metrics segmented by commodity groups—particularly rebound pace in merchandise categories versus sustained gains in intermodal shipments—as early indicators of demand strength or weakness post-pandemic recovery phases [S2][N4].

Service quality measurements such as velocity improvements or trip plan adherence will signal execution efficiency crucial for retaining premium customers amidst modal competition. Developments around labor contract ratification schedules merit attention given potential impact on cost structures or disruption risks.

Regulatory updates related to hazardous materials routing restrictions or environmental legislation changes could materially influence network utilization strategies. Monitoring cybersecurity risk exposure disclosures will provide insight into operational resilience preparedness.

Earnings guidance updates signaled during quarterly earnings calls will contextualize management’s outlook on macroeconomic headwinds versus internal productivity gains driving profitability next phases [N1][S2].

Financial Profile: Capital Allocation, Cash Flow, and Profitability Metrics

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($bn) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2.9 | 4.6 | 4.5 | 2.9 | -16.7% |

| 2024 | 3.5 | 5.2 | 5.2 | 2.5 | -6.6% |

| 2023 | 3.7 | 5.5 | 5.6 | 2.3 | -10.8% |

| 2022 | 4.2 | 5.6 | 6.0 | 2.1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($bn) | FCF ($bn) |

|---|---|---|

| 2025 | 1.4 | 1.7 |

| 2024 | 2.2 | 2.7 |

| 2023 | 3.5 | 3.3 |

| 2022 | 4.7 | 3.5 |

Source: SEC companyfacts cache [F1].

Supporting the above operational narrative are robust financial trends underscoring CSX's strong cash flow generation albeit with some moderation in Q1/2026 relative to prior periods. Per FY2025 reported figures [F1], net income declined approximately 17% year-over-year to $2.89 billion while operating income fell nearly 14% reflecting cost inflation impacts balanced against volume/mix shifts.

Operating cash flow totaled about $4.6 billion with capital expenditures rising close to $2.9 billion (+14.7% YoY), reflecting ongoing infrastructure modernization commitments exceeding depreciation expense levels signaling capacity expansion investments rather than mere maintenance [F1][S11]. Free cash flow remained positive at roughly $1.7 billion supporting liquidity needs.

Dividend distributions continued their upward trajectory consistent with policy—marking the twenty-first consecutive annual raise—while share repurchase activity amounted to $1.4 billion during FY2025 though down from prior years' heavier buyback cadence due to preservation of financial flexibility amid uncertain external conditions [F1][S14].

Balance sheet liquidity remains solid with approximately $675 million cash alongside undrawn revolving credit facilities providing ample short-term funding buffers despite working capital deficits typical for capital-intensive railroad operations (current ratio ~0.97) [F1][S13]. Capital structure prudently managed maintaining investment-grade debt ratings vital for market access at attractive terms.[F1]

Overall profitability metrics indicate strong return on equity (~34%) evidencing efficient use of invested capital especially given scale of fixed assets implying durable economic moat returns rather than cyclical margin spikes uncorrelated with underlying asset base quality [F1].

This analysis synthesizes publicly available filings up to Q1 2026 without speculative forecasts beyond documented management commentary or quantitative disclosures. It aims solely at delivering an informed industry perspective on CSX's recent operational execution and strategic posture within the regulated freight transportation sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments