Winning Catering Group’s Strategic Transformation and Path to Growth

The company transitions from land development to a shell status, preparing for a pivotal merger to redefine its strategic direction.

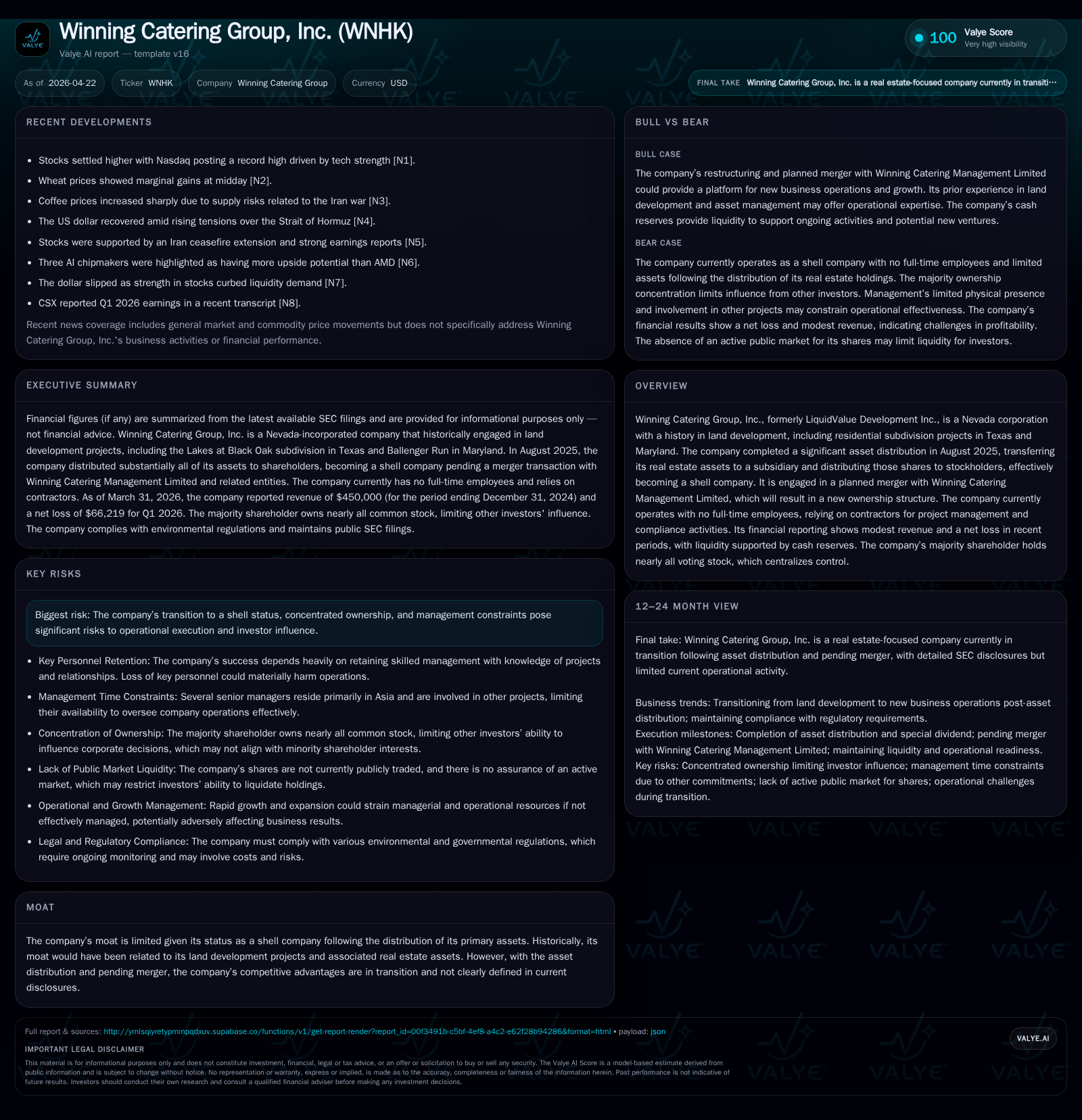

Winning Catering Group, Inc. has effectively transformed itself following a significant asset distribution in August 2025 that offloaded its core real estate holdings, rendering the company a shell poised for change. The latest quarterly filing as of April 22, 2026, reveals minimal operating activity and revenue, reliance on contractors rather than full-time staff, and concentrated ownership—factors that frame the company's near-term operational posture. Central to the firm's outlook is a planned merger with Winning Catering Management Limited, which will usher in an entirely new ownership structure with Winning Holdings Limited expected to control approximately 80% post-merger. This strategic pivot introduces both growth prospects through market repositioning and heightened execution risks rooted in management bandwidth and governance constraints.

Latest Quarterly Update: Implications of Shell Status and Operational Pause

In its most recent quarterly report filed April 22, 2026 ([S2]), Winning Catering Group disclosed its operational status after completing a defining corporate event: the August 18, 2025 special dividend distribution of all shares in its principal subsidiary owning underlying real estate assets (Alset Real Estate Holdings Inc.) to existing shareholders ([S1]). This event removed substantially all net asset value from the parent entity — approximately $34.8 million as of the distribution date — leaving Winning Catering as a regulatory "shell company" under definitions per Rule 405 of the Securities Act.

Post-distribution operations show nominal revenue generation juxtaposed against continued net losses. The company now operates without full-time staff, engaging contractors solely for project management and compliance obligations chiefly tied to governance during the transition. Such an arrangement indicates an operational pause consistent with holding patterns prior to transformative corporate events.

Ownership remains highly concentrated: the majority stakeholder currently commands nearly all voting shares. While dilution is expected post-merger due to new share issuances granting Winning Holdings Limited around 80% ownership ([S1]), present control dynamics constrain other investors’ influence over corporate decisions.

Business Model Shift: From Land Development Assets to Contractor-Driven Operations

Historically, Winning Catering’s business model was anchored in land development via subsidiaries managing residential subdivision projects notably in Texas (Lakes at Black Oak) and Maryland (Ballenger Run) ([S1], [S28]). Revenue streams derived from lot sales coupled with income streams such as model home leases—a niche but relevant revenue-generating contract exemplified by agreements with Davidson Homes LLC starting mid-2023 ([S1]). These activities required extensive capital allocation for land acquisition, development costs including construction reimbursements (notably $220k paid on January 4, 2024), environmental compliance studies (~$71k prior to distribution), and local regulatory navigation.

The August 2025 asset spin-off has stripped the company of these physical assets and operational projects. Today’s corporate structure evidences no full-time employees and reliance on third-party contractors for necessary administrative functions and regulatory compliance ([S1], [S22]). This marks a clear strategic pivot away from asset-heavy development toward a leaner holding framework awaiting reactivation through an anticipated merger.

Key operational dependencies now rest on few individuals—particularly Asian-resident Co-CEOs maintaining multiple external commitments—which inherently limits direct managerial oversight on U.S.-based real estate activities ([S19], [S21]). This decentralized control coupled with non-resident board members raises notable governance transparency issues.

Industry Context: Competitive Dynamics in Real Estate Development and Merger Strategy

Prior to its transformation into a shell entity, Winning Catering operated within the typical contours of suburban residential land development—a sector characterized by long project life cycles tied to master-planned community certifications, phased lot sales, model homes as marketing assets, and complex multilayered regulatory hurdles involving federal/state/local jurisdictions ([S1], [S28]). Capital requirements are substantial; returns are nonlinear across multi-year timelines due to upfront acquisition costs followed by incremental sales revenue realization.

Geographically concentrated efforts—in Montgomery County Texas and Frederick County Maryland—expose Winning Catering historically to localized cycle risks including community demand changes or zoning amendments that could materially impact project economics ([S28]). Current fragmentation among small-to-mid sized developers fosters competitive tension but also creates room for market repositioning if scale or diversification is attained.

With conversion into a shell company pending merger, Winning Catering steps out of this capital-intensive real estate arena into a holding pattern that will soon be tested by planned integration with Winning Catering Management Limited ([S1]). This merger embodies a strategic inflection point intended to pivot business focus potentially onto less asset-constrained segments or new operational verticals enabled by new ownership alignment.

Growth Drivers: Merger Execution and Potential Market Repositioning

At the heart of Winning Catering’s near-term growth thesis is closure of the May 30, 2025 Acquisition Agreement involving SeD Intelligent Home Inc., LVD Merger Corp., Winning Catering Management Limited ("Winning Group"), Winning Holdings Limited, and Pure Talent Group Limited ([S1]). Post-merger structure anticipates significant dilution whereby current shareholders retain only about 15% equity interest while Winning Holdings emerges controlling roughly 80%.

This transaction is designed not merely as financial restructuring but as an operational reboot—consolidating new management capacity, capital access, and likely targeting expansion or diversification outside traditional land development models. Though specifics remain undisclosed regarding new business lines or market focus post-merger, the shift signals opportunity from being sidelined as a shell company into potential active market player under revamped leadership.

Despite presently limited revenues stemming largely from legacy contracts finalized before distribution (e.g., lot sales closed through early 2024), issuance of new equity tied to merger activity could unlock necessary capital infusion unlocking fresh operational initiatives or acquisitions aligned with evolving corporate strategy ([S1]).

Headwinds and Risks: Concentrated Ownership, Management Bandwidth, and Execution Challenges

Winning Catering confronts pronounced risks deeply embedded in its structural transition phase ([S1], [F1]):

- Ownership Concentration: Nearly total control consolidated in one stakeholder pre-merger constrains minority investor influence on corporate decisions including compensation policies or transaction approvals. While dilution will occur post-merger ownership remains highly skewed toward Winning Holdings which may pursue interests not fully aligned with prior holders.

- Management Limitations: Co-Chief Executive Officers reside primarily in Asia overseeing multiple unrelated projects limiting frequent hands-on engagement across geographically dispersed properties in U.S markets. Such stretched focus risks delayed decision-making or overlooked compliance details critical during this governance-intensive transition period ([S19]).

- Regulatory & Legal Complexity: Non-U.S.-resident directors complicate enforcement of shareholder remedies under U.S securities laws potentially undermining minority holder protections ([S19], [S21]). Oversight challenges amplify amid cross-border coordination needs inherent in merger integration.

- Financially Constrained Operating Environment: Recent financial disclosures illustrate ongoing net losses and negative operating cash flow consistent with an inactive or minimally active company awaiting transformational catalysts ([F1], [S2]). Prolonged inactivity risks impairing stakeholder confidence absent near-term progress updates.

Upcoming Catalysts: Merger Closing, Governance Changes, and Operational Milestones

Investors will keenly monitor completion timing of the pending Acquisition Agreement-triggered merger which defines immediate corporate trajectory ([S1]). Milestones potentially bearing material informational value include:

- Definitive shareholder approvals or regulatory clearances enabling formal reconstitution of corporate governance with new independent board members reflective of shifted ownership base.

- Initial public announcements pertaining to business plans post-merger including hiring initiatives marking end of contractor-dependent operating model.

- Financial guidance updates clarifying capitalization pathway beyond existing cash reserves towards supporting anticipated business relaunches.

- Progress towards listing compliance if public trading aspirations accompany equity restructuring efforts given expanded share authorization approved August 2025 ([S24]).

These events collectively comprise vital execution checkpoints validating transition momentum from dormant shell status into renewed operating entity primed for growth.

Financial Overview: Cash Position, Recent Losses, and Liquidity Before Transformation

A synthesis of recent historical financials clarifies resource posture underpinning transition efforts ([F1]):

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1 | -1 | -1 | 1650 | -114.6% |

| 2024 | 7 | 14 | 6 | 1650 | +7.8% |

| 2023 | 6 | 13 | 6 | 3083 | +347.2% |

| 2022 | -3 | -10 | -1 | 3083 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1 | -16477.2 |

| 2024 | 14 | 18.7 |

| 2023 | 13 | 21.5 |

| 2022 | -10 | -11.2 |

Source: SEC companyfacts cache [F1].

FY2025 figures reflect transformation effects starting mid-year culminating in substantial decline in equity value post-distribution alongside net losses attributable largely to operating inactivity ([F1], [S2]). Remaining liquidity suffices only for minimal administrative tasks presently while awaiting external capital infusion connected to merger closure.

This financial snapshot supports qualitative analysis emphasizing transitional nature marked by paused income streams but preserving foundational resources pending conversion into new enterprise form.

Disclaimer: This analysis is based exclusively on publicly available information as of April 22, 2026. It does not constitute investment advice or recommendations regarding securities issued by Winning Catering Group, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments