Intuitive Surgical’s Accelerating Procedure Growth Fuels Q1 Upside

Strong Q1 results paired with a recent distribution acquisition underscore Intuitive Surgical’s path to broaden market penetration and sustain recurring revenue growth.

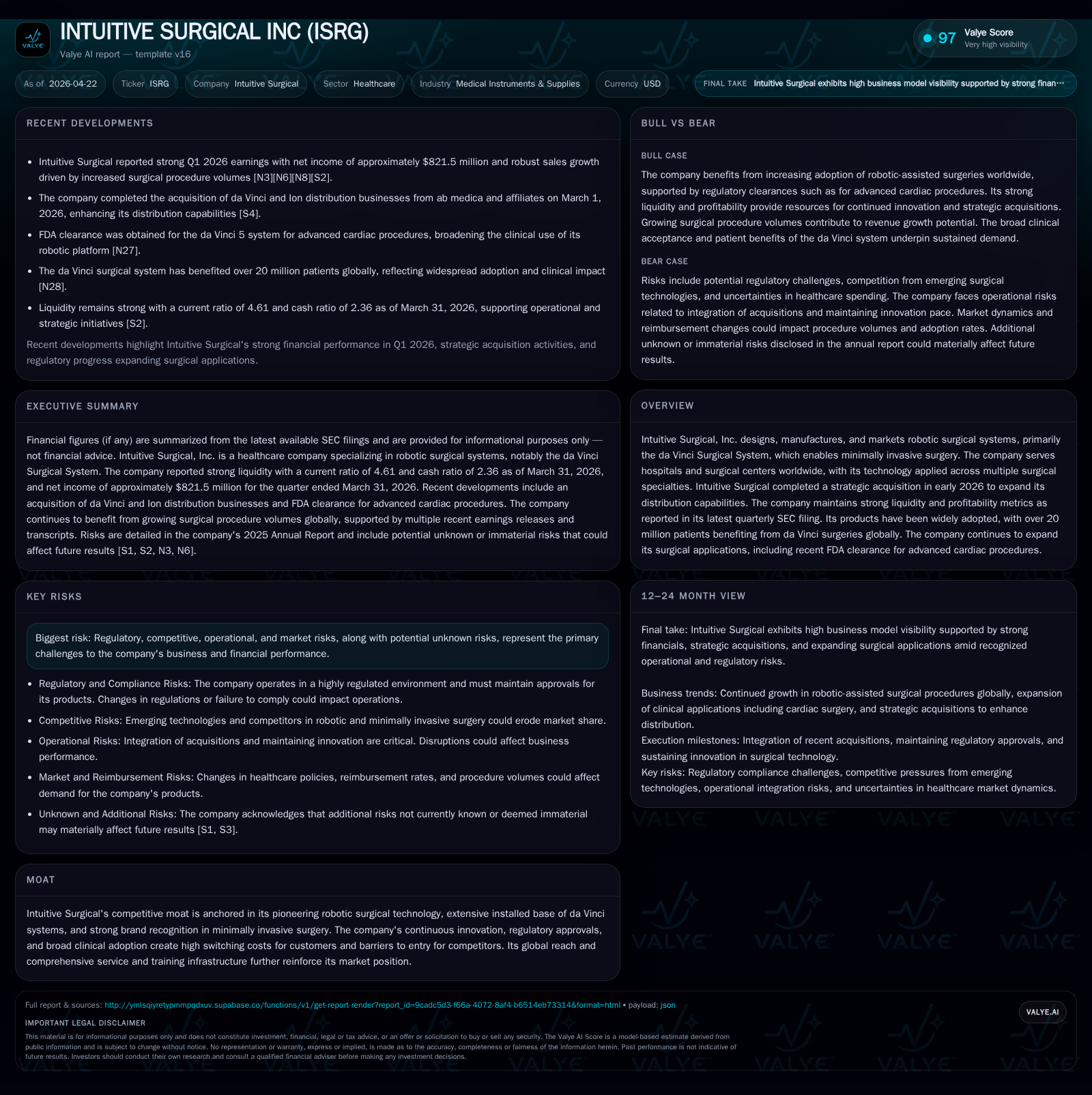

Intuitive Surgical reported Q1 2026 results that exceeded expectations, driven by continued growth in procedure volumes and improved operational leverage. Complementing this momentum, the company completed a strategic acquisition in early 2026 to internalize key distribution channels across Europe, Latin America, and Asia, reducing dependency on third-party operators and enhancing sales efficiency. The business model, anchored by recurring revenues from instruments and services tied to its installed base of da Vinci systems, remains robust amid expanding surgical indications such as advanced cardiac procedures. Regulatory approvals and entrenched switching costs solidify Intuitive’s competitive moat, though potential risks include regulatory delays and emerging rivals. Upcoming milestones center on integration progress and new procedure launches.

Q1 2026 Results Highlight Strong Procedure Momentum

Intuitive Surgical’s latest quarterly filing dated April 22, 2026 ([S2]) reveals that the company delivered revenue and unit sales above consensus estimates for Q1 2026. This performance was propelled by accelerating procedure volumes leveraging its da Vinci Surgical System platform — a leading robotic surgery technology widely adopted across multiple specialties. The firm's sales momentum is underpinned by higher shipments of surgical systems coupled with increased “attach rates,” referring to instrument and accessory usage per procedure. This dynamic renews Intuitive’s core recurring revenue streams tied directly to the installed base economics of its robotic platforms ([N2], [N5], [S3]). Operational leverage also improved due to scale efficiencies as procedural utilization rises.

The uptick reflects structural demand drivers in minimally invasive surgery (MIS), where clinical evidence supports superior patient outcomes relative to traditional open surgery. As surgeons accumulate experience with the platform and hospitals expand case loads, average instrument consumption grows in tandem — a critical factor sustaining durable top-line growth beyond initial capital equipment sales.

Strategic Acquisition Enhances Distribution Capabilities

In early March 2026, Intuitive Surgical announced completion of an acquisition absorbing the da Vinci and Ion system distribution lines from key regional operators including ab medica, Abex, Excelencia Robótica across Europe, Latin America, and Asia ([S7], [S3]). This shift from third-party distributor dependence toward direct control addresses historic challenges around reach and sales efficiency in fragmented international markets.

By integrating these distribution businesses into its own operations, Intuitive is expected to unlock margin enhancements through reduced intermediary markups while enabling more cohesive customer engagement strategies tailored locally. Moreover, direct oversight over training programs, service delivery timelines, and inventory management yields tighter operational coordination—a crucial advantage given the complex nature of robotic surgical hardware logistics in diverse healthcare systems ([N11]).

This move is transformative in scaling global penetration without diluting brand service quality or technical support standards. It also signals confidence in the underlying market opportunity for robotic-assisted surgeries beyond North America.

Business Model: Driving Recurring Revenue Through a Robust Installed Base

Intuitive Surgical’s business model centers on the sale of capital-intensive da Vinci Surgical Systems complemented by an expanding annuity-like stream generated from proprietary instruments, accessories suppliers consume per procedure, plus maintenance services ([S1], [S14]). The company benefits from entrenched high switching costs: hospitals make long-term commitments investing heavily in clinical training for surgeons and operating room staff—intangible assets costly to replicate or transition away from once established.

Revenues thus bifurcate into system sales accounting for initial large outlays balanced by steadily growing consumable instrument usage dependent on case volume. This model fosters predictable cash flows over extended periods while incentivizing product innovation to broaden surgical indications. FDA clearances recently expanded application of the da Vinci system into advanced cardiac surgeries—a challenging area representing incremental addressable market growth that drives up total procedure volume per unit deployed.

Competitive Advantages Rooted in Technology and Customer Ecosystem

Intuitive commands a substantial competitive moat founded on pioneering robotic technology widely perceived as superior in precision, dexterity, visualization quality, and ergonomics ([S14], [S1]). Extending beyond hardware superiority is the company’s comprehensive ecosystem: surgeon training programs tailored to accelerate adoption curves; dedicated service networks ensuring uptime; broad clinical trial data validating safety/efficacy; plus a strong brand synonymous with MIS innovation.

The extensive installed base propels network effects—the more units implanted globally elevates clinician peer familiarity biasing hospital purchasing decisions towards proven solutions. Regulatory achievements like FDA approvals for cutting-edge cardiac procedures further raise barriers for competitors lacking such clearances or exhaustive clinical evidence packages. Switching costs are further reinforced by software/platform integrations unique to Intuitive devices complicating migration.

Industry Dynamics: Pricing Power, Regulation, and Adoption Curves

Within the medical instruments industry spectrum focused on robotic surgical systems, Intuitive enjoys pricing leverage derived from differentiated product offerings protected by intellectual property and semi-monopolistic positioning ([S1]). The regulatory environment is notably stringent: every new indication demands protracted FDA review cycles entailing substantial data submission burdens—an effective moat restricting new entrants.

Manufacturing complexity limits rapid capacity expansions given the precision electronics/mechanical assembly required for da Vinci systems. Globally the adoption curve reflects steady structural growth fueled by reimbursement policies increasingly favoring minimally invasive approaches due to lower complications/hospital stays versus conventional surgeries. However, asymmetric competitive pressure arises from emerging rivals pursuing niche applications or lower-cost robotic approaches aiming at price-sensitive customer subsets.

Growth Catalysts: New Surgical Indications and Global Expansion

Looking ahead, principal growth levers reside in augmentation of approved surgical indications—such as the recent clearance for advanced cardiac surgeries—which deepen utilization rates per device beyond established urology/general surgery/tissue procedures ([S1]). Geographically expanding market presence further fuels upside particularly within underpenetrated international regions where healthcare infrastructure investments are accelerating.

The March 2026 acquisition acts synergistically here: enhanced distribution footprint supports broader channel coverage that dovetails with ongoing product portfolio enhancements facilitating entry into emerging procedural categories. Training pipelines remain a high-leverage asset—continuously growing numbers of certified surgeons contribute to rising case volumes globally underpinning consumable usage growth.

Potential Headwinds: Regulatory Risks and Emerging Competition

Risks surface primarily around regulatory uncertainties potentially delaying new approvals or imposing additional compliance costs ([S4], [S6], [S8]). Litigation exposure persists as manufacturers of complex medical devices frequently face legal disputes connected with device claims or patent infringements—possible earnings volatility factors.[S8]

Competition is intensifying albeit selectively; rivals focus on cost innovations or targeting less complex procedural niches intending to erode parts of Intuitive’s addressable market share. Unforeseen regulatory tightening or rapid technology shifts represent "unknown unknowns" necessitating cautious monitoring despite currently robust positioning.

Upcoming Milestones and Market Signals to Monitor

Investors should watch forthcoming quarterly reports for detailed adoption metrics post-distribution acquisition capturing usage progression across new geographies ([S2]). Progress updates regarding FDA submissions or approvals extending da Vinci’s application scope beyond established areas also represent critical signals. Execution success integrating acquired distributors will influence margin trajectories reflecting operational scalability.

Surgeon enrollment rates in training programs serve as leading indicators of future case volume accelerations while any announced partnerships expanding product functionalities merit close attention as well.

Supporting Financial Overview

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 2.9 | 3.0 | 2.9 | +23.0% |

| 2024 | 2.3 | 2.4 | 2.3 | +29.2% |

| 2023 | 1.8 | 1.8 | 1.8 | +36.0% |

| 2022 | 1.3 | 1.5 | 1.6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | ROE% |

|---|---|---|---|

| 2025 | 0 | 2.3 | 16.0 |

| 2024 | 8 | 0.0 | 14.1 |

| 2023 | 0.4 | 13.5 | |

| 2022 | 2.6 | 12.0 |

Source: SEC companyfacts cache [F1].

According to companyfacts data through FY2025/ Q1 2026 ([F1]), Intuitive Surgical demonstrates strong financial health:

- FY2025 revenue expanded nearly 18% year-over-year showing sustained top-line momentum,

- Operating income grew over 25%, reflecting effective cost management amidst scaling,

- Net income rose approximately 23%, reinforcing profitability,

- Cash & equivalents stood robustly at $2.0 billion at quarter-end March 2026,

- Current ratio approximated a healthy 4.6x indicating solid liquidity,

- Capital allocation includes $2.3 billion repurchased shares during FY2025 signaling confident deployment of excess capital.

These figures substantiate operational strengths highlighted earlier without dominating the analytical narrative but reinforce confidence in sustainable business model execution moving forward.

This analysis is based on publicly available SEC filings up through April 22, 2026 ([S1], [S2], [S3]) supplemented by aggregated financial data ([F1]) and market news sources ([N2], [N5], [N11]). It is intended solely for informational purposes without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments